"When Incentives Are Gone, What's Left? DeFi Gets Mixed Marks:" Sam Bankman-Fried

FTX co-founder Bankman-Fried and Solana co-founder Anatoly Yakovenko talk about the future of decentralized finance on The Defiant podcast.

In this week’s interview, I speak with Sam Bankman-Fried, co-founder and CEO of crypto liquidity provider Alameda Research and derivatives exchange FTX, and with Anatoly Yakovenko, the creator of the Solana blockchain.

Bankman-Fried, also known as SBF, recently announced the launch of Serum, a DEX built on the Solana blockchain. In this episode, we talk about why he chose Solana and Anatoly explains how Solana works and how it’s able to process tens of thousands of transactions per second. Anatoly hopes that a higher throughput blockchain like Solana means that people can start dreaming big about what they can build.

SBF has become known to be a ruthless trader, but he argues he’s simply using DeFi protocols for what they were made. He says his firms’ involvement in DeFi will be motivated by short-term profits and is not seeking to have a long-term impact in protocols via governance.

For Anatoly, the end goal of Solana is to find the fastest and cheapest way to scale cryptography so that people are able to have ownership and participation in the applications they use, and so that the financial system can become more open efficient.

🎙Listen to the interview in this week’s podcast episode here:

You’re a paid subscriber, which means you get the full transcript below. Subscribers also get exclusive access to The Defiant’s Discord chat for the community, here’s a new link to join.

🙌 Together with Zerion, a simple interface to access and use decentralized finance, Sorare, a fantasy football game with officially licensed cards on Ethereum, and Near, a high-performance proof-of-stake blockchain that interoperates with Ethereum.

Sponsored Post

3, 2, 1...Liftoff: One week to go till applications close for Filecoin Frontier Accelerator!

We enter the countdown for Filecoin Frontier Accelerator, with only one week away till applications close on 15 November! If you’re new to us, our 12 week-accelerator program offers a $20K grant, follow-on investment of up to $1 million, and a global network of mentors from blockchain-native and institutional companies including UNICEF Ventures, Winklevoss Capital and Fenbushi Capital.

More questions? We’ve rounded up an expert panel from Filecoin and LongHash Ventures in an upcoming Ask Me Anything happening on 11 November 7 PM PST/12 November 11 AM SGT. The session will be conducted in both English and Mandarin - come join us to make the most out of it.

If you’re part of the vanguard bringing Web 3.0 to reality, join us:

1) Core infrastructure driving the transition towards a more decentralized, efficient and resilient Web, supporting essential functions such as networking, computation and storage.

2) Middleware solutions that extend the utility of Filecoin beyond the blockchain protocol. Some examples include data oracles, plug-and-play blockchain toolkits, developer APIs, block explorers or search engines.

3) Applications that provide and enable end user interaction, running the gamut from gaming to social media to content marketplaces.

Apply by 15 November.

Sam Bankman-Fried: I was an ETF trader at Jane Street Capital before I got into crypto, on Wall Street and left in 2017, and sort of checked out a number of things, including briefly looking at CoinMarketCap and seeing some pretty big arbitrages and ended up basically diving into crypto trading.

Camila Russo: Driven by arbitrage opportunities?

SB: Yeah.

CR: So you left Jane Street to start a crypto derivatives trading desk. How was that transition?

SB: I didn’t know exactly what I was going to do when I left, but I checked out a number of things. When I checked out crypto, it was sort of with an eye towards, like are there good trades to do here? Are there good arbitrages, quantitative modeling type things that would be worth doing? Basically seemed after looking into it a bit, like there are some pretty gigantic opportunities there, if any of this sort of data was real, and so you end up basically diving in.

Really quickly realized there were, in fact, gigantic opportunities here. But it was not easy to do them. There's a lot of operational work that went into getting set up to do one of these trades, because you had to get together your bank accounts with exchange accounts and withdrawal limits and blockchain infrastructure, and you had to understand the trading and the flow, and sort of a bunch of these things together in order to actually complete even just a single simple arbitrage. So I spent the next month building out a team and building up the infrastructure to do that.

“Really quickly realized there were, in fact, gigantic opportunities here [in crypto]. But it was not easy to do them. (…) So I spent the next month building out a team and building up the infrastructure to do that.”

CR: That was kind of how Alameda came about?

SB: Yeah, that was Alameda starting up late 2017.

CR: Anatoly, do you want to give us your background and what got you into crypto?

Eureka Moment

AY: So I spend most of my career at Qualcomm, study computer science. When I ended up at Qualcomm, I kind of jumped into optimizations, really working on protocol stuff, embedded systems, operating systems. If you ever remember those old school flip phones, I was on the team that built the first developer platform for mobile. They were like half a billion of these devices out there, about 2 billion app downloads, stuff like that.

2017, I was at Dropbox working on compression. With Stephen, who is a cofounder at Solana, we had this silly startup to use crypto mining to offset the cost of deep learning hardware. We're more interested in deep learning, but we wanted to buy a bunch of hardware to build something interesting. The way to offset the capital cost is you might add in the background.

CR: Did it work out?

AY: No. Before we put in enough interesting amount of capital there, I had the idea to start Solana, which was we were getting into the weeds of proof of work, why it's slow, why is it necessary for consensus and I had too much coffee and beer, and I was like up till four in the morning and this kind of like eureka moment for using the same technique that you use in proof of work, but to track the passage of time.

Because I spend most of my career at Qualcomm, time is a fundamental optimization technique for wireless protocols, like time division, multiple access. The most boring radio protocol ever, 2G foundation for cellular networks, that can handle thousands of block producers. So that was it, right? That's what started it for me.

CR: Using time as a core element inside a blockchain was kind of the Eureka moment?

AY: So if you look at like a bunch of consensus protocols, like a ton of academic work, almost in the first paragraph, all of them say, we make weak assumptions about time and this thing, this protocol is still valid, still has strong conditions, strong results for safety and availability. So those weak assumptions about time make it really, really hard to work from an engineering level, like it becomes a kind of an impossible thing.

CR: So the reason why you're both on this podcast is because FTX announced it would be building a decentralized exchange called Serum on top of Solana back in July. So, Sam, why did you choose Solana as your base layer?

A Billion Users

SB: We were sort of looking at what to do, and talking to a number of projects. Once we decided that we want to do something in DeFi, there are sort of two options. One was, do what it will work, and the other was, do what we're most excited about. And do what will work, what I mean is like, do the thing that definitely will at least be fine.

From that perspective, it's like, what's the thing that we're really confident about the path forward for? For a lending protocol on Ethereum or something like that, this sort of thing that people are doing, it's obvious how it plugs into the current infrastructure. It's obvious what role it is. It would just be a marginal improvement on what the current Ethereum DeFi ecosystem at the time was, but is definitely not going to be super ambitious.

The reason for that was, any time we tried to build anything we're excited about, we just immediately exceeded the throughput of Ethereum blockchain by orders of magnitude. At some point, it’s just clear that we weren’t getting around that. Either, we're going to build it on Ethereum, or we are going to build something that we thought was going to be really exciting, but not both.

Then when we sort of started thinking more about it, there's the sense of why half-ass it. If it's worth doing, it was going to be enough of a production no matter what. It wasn't going to be like a one-week side project thing. It's really sad to have a three-month project and release it, and you just know from the beginning, the project's not going to scale and it's not going to be that cool.

But we were excited, and the reason we were excited was that we're excited about DeFi, and the world was excited about DeFi and there's a lot of potential there. So if we really want to tap into that, the thing that really had upside was going to be the thing that had a chance to become huge. What does that mean? It means that you could imagine a world in which a billion people use it.

“…the thing that really had upside was going to be the thing that had a chance to become huge. What does that mean? It means that you could imagine a world in which a billion people use it.”

It's true of crypto and I think it's true of FTX. What's an enormous upside case for FTX, it's the world in which they are a billion traders with accounts on FTX. What's an upside for Serum was going to be a world where a billion people use it. As soon as we got there, we were like, alright, well, we have some instincts about what the fundamental building blocks of a decentralized financial ecosystem would be.

But if we're looking to scale to that number of people, it's not just Ethereum and it's also not just 100 times faster than Ethereum, we need like a million times faster than Ethereum. And that prices out basically every blockchain, and you need not just one of the fastest blockchains, but a blockchain that is built to scale, one where it's going to keep getting better over time.

“…it’s not just Ethereum and it's also not just 100 times faster than Ethereum, we need like a million times faster than Ethereum.”

When we talked to a bunch of different ones, it kind of quickly became clear, alright, one of the core principles for it was if you want to care about throughput and speed and efficiency when building a blockchain, how would you do it from first principles? How would you make it scale natively? For all the others, it was sort of not quite an afterthought but “and also we made it fast.” That's one of our 12 pillars and one of the 12 pillars is not enough to scale. That's enough to get 10 times the current DeFi ecosystem using it efficiently which is cool, but it's not huge. So that was the thing that was really exciting.

CR: Basically, you looked at this space and said, which is the blockchain that is the most scalable, that is capable of really supporting the throughput that we need for getting a billion users on this DEX?

SB: Yes. We could get there theoretically.

Censorship Resistance

AY: So fundamentally, to me, what we're scaling isn't blockchain, it's kind of a core thing of it, which is the censorship-resistant part. You can scale a database, right, but I think, when you look at a lot of blockchains, and they give you a TPS number, it's kind of like a bolt on top of the rest of the system. The way we've designed this thing, kind of from first principles is that what is the point of this thing to begin with, and then how do we maximize that to the physical limit bounded by silicon?

“What we're scaling isn't blockchain, it's kind of a core thing of it, which is the censorship-resistant part.”

The key part there is this idea that censorship-resistant, this is a fundamental aspect of decentralization that differentiates the systems from databases. Like why can't FTX just go use PostgreSQL and be done with it, right? It's because they want something that is censorship-resistant. That is what we're scaling. It's not so much that we're scaling TPS, it just also happens that when we increase the capacity for this thing, for this key differentiator of this technology from everything else, it also makes it possible to do trading price discovery, like all this other stuff, all the cool use cases, and get to this billion person level.

CR: So what you're scaling is actually censorship resistance, and then increased TPS comes as a result of that?

Betting on Moore’s Law

AY: Yep. So our approach is not like the other folks are wrong. They've picked a different point than this Pareto efficient curve. We're going to do this with sharding; we're going to do this with zero-knowledge proofs. Those systems kind of create different tradeoffs. The way we're doing it, and betting everything on is Moore's Law. So to give you an example, to tie it all together, our consensus runs as a smart contract. So votes are transactions, and those transactions are processed on a multi-core, multi-threaded GPU accelerated system. When Intel and Nvidia double the number of cores every two years, our TPS goes up, and that means we can scale the network to double the size, therefore be twice as decentralized and twice as censorship-resistant.

So what we're betting on is this idea that hardware as it's been scaling for the last 50-60 years, it's going to continue to do so, because there are probably 3 million engineers working on that problem. There's already TSMC building a three-nanometer fab, right? So that kind of fab bet is what allows us to kind of stand on the shoulders of that industry and build something that just gets better with time. No matter what, the system is going to get faster and faster.

CR: So I read that Solana can process theoretically up to 700,000 transactions per second and right now it's at 50,000 TPS. So does that depend on the hardware improving, getting to that 700,000 number?

AY: Yes. So the trilemma, that number comes from the bandwidth that is available to the network. If we were to test this in a one-gigabit network with a bunch of hardware, and each node, we could process probably close to 700,000 with a bunch of work, because memory, throughput, and all these other things still need some engineering work. But that's limited by the bandwidth of the network. So today, we're seeing 5G networks deployed with one gigabit. 20 years ago, if I would have told you that, I would have sounded as crazy as I would be today saying that we're going to see one terabit internet 20 years from now.

CR: So it’s like bandwidth plus hardware?

Marketing Trick

AY: Yeah. So these limiting factors that are limits on the physical processing power, all of these things are growing at an exponential rate. This is why we just threw that number out there just as a marketing trick for you.

CR: Good of you to admit it.

AY: The reality is that those are marketing tricks. I think one of the conversations Sam and I had, like, we were already live, so that was an advantage of versus our competitors. We’re already live and it was already fast. So we kind of showed them our demo, you can smash your keys. I don't know if folks are listening, but can go to break.solana.com. Literally, it's a very dumb app that we use as a sales demo, and you smash your keyboard and as fast as you smash them, transactions are sent to the global network and confirmed.

CR: I’ve done it. It’s pretty cool.

AY: Those are smart contract transactions, there's no faking it. It's going through the full path of the whole system, and that's as fast as Serum runs right now. Humans, I think, probably can't tell the difference between the Serum UI and its speed than the Binance one. Bots definitely can, but I think it's good enough that we can fool most humans at this point.

CR: That's a good start. One more thing on the nuts and bolts on of Solana, is what happens to the nodes needing this highly sophisticated hardware? Does it limit access? Does it reduce the ability for people to participate in the network?

Like a Playstation

AY: Yes and no. Right? So we live in a world with 7.5 billion people. How big is the Ethereum and Bitcoin network? It’s about like 10,000 machines. Nvidia ships 10 million GPU cards a year. There's 100 million PlayStations out there. A PlayStation 5 already has faster specs than what we'd recommend for people to run a validator. So effectively, we live in a world where finding 10,000 people that are into building fast systems and like tweaking them and configuring them, it's not a hard problem. That'll just happen from adoption.

“A PlayStation 5 already has faster specs than what we'd recommend for people to run a validator (…) The problem that we need to focus on is getting more awesome applications.”

The problem that we need to focus on is getting more awesome applications, Serum or things that will plugin with Serum, like the swap implementation that they launched. If we succeed there, the ecosystem grows, there are 10,000 people out there that are into building high-performance computers that will go do it. These are super-specialized systems. These are like gamer boxes. This is off the shelf hardware you can buy it on BestBuy or Amazon, and they'll be at your house in two days and you can put it together and take pictures of it.

Folks, myself and a bunch of the cofounders were cyclists and we have this thing called Tour de Sol, which is our testnet where people stress test networks, and we do time trials. There are already people that have built systems that can do 300,000 TPS from just off the shelf hardware. So that part is, I think, is the easy part because it's not like product-market fit. It’s just getting people to go and do it.

SB: One thing I'd add to that is as Anatoly said like, there's a curve here, there's a tradeoff. There's a tradeoff between decentralization and performance here. You can think of it as all one Pareto curve in that, the higher the hardware requirements, the less decentralization but the more throughput. But that doesn't mean that you think all points on the curve are equally good. At some point, when you're like, you can do one TPS per month because it’s people using an abacus, to compute the blockchain. That's taking it further than the need to go.

“The higher the hardware requirements, the less decentralization but the more throughput. But that doesn't mean that you think all points on the curve are equally good.”

But getting back into more reasonable territory, there's sort of this thing of what is the right point there? How much did you dial up the tech requirements, and Ethereum is at a very, very low point on this curve right now. Ethereum is at the point where any device like a chip and an internet connection can do it.

AY: It is actually like Ethereum is so poorly designed that it doesn't need hardware that is that much lower than Solana. So that is kind of part of the problem.

SB: Let's get rid of Ethereum, and let’s say, proof of stake variant, like, a proof of stake network, but dial down to Ethereum TPS. I'm guessing that's kind of hard to even think about devices that.

AY: So where this question of like, I think the Pareto curve is more focused not on hardware, but on high available bandwidth. Ethereum doesn't need a lot of bandwidth because the number of transactions per second is so small that it can run on a one megabit connection, or not a 56KB modem, but like a pretty low connection. Because Solana is processing more transactions per second, it's handling like 500-600 right now, per second, it needs more bandwidth, and that bandwidth is expensive, right?

But if you do some back of the envelope analysis, $115 million was worth the number of fees that the Ethereum network collected during the month of August. That should pay for 20,000 systems that can do 300,000 TPS that our friends have demonstrated plus the bandwidth to do that for the entire year.

CR: So the incentives are there. Now going to Serum, Sam, I want to learn more about, well, I've seen the interface and it's very different from the most popular Ethereum DEXs, it does have this order book system different from AMMs. I want to hear more about your thinking between the user experience and how this DEX works and why you decided to design it this way versus the leading AMMs or DEXs that we're used to?

AMMs Vs. Order Books

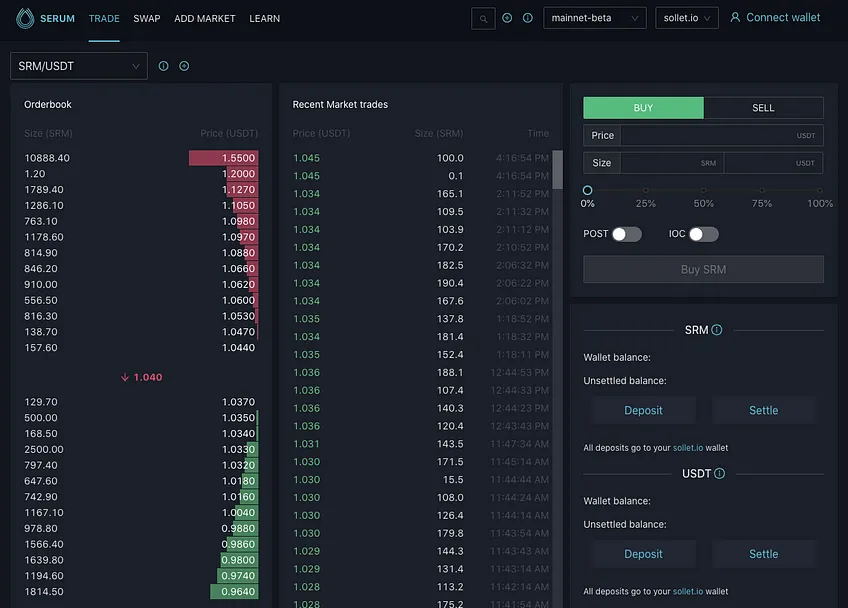

SB: The first thing I'll say is that Serums is more than just one DEX, and there's, a bunch of things being built on it, including there's now an AMM live on it. But so the first DEX that came out there, which is the order-book based one, why is it designed that way? I think the answer is like, almost anywhere you look, when you look at scaling financial systems, almost all of them end with an order book. That's sort of where everything bottoms out.

Image source: dex.projectserum.com

There's a reason for that, which is that that's sort of the most general way of letting people express what they're willing to buy and sell at different prices and it's sort of the most powerful version of that. It's sort of the market has spoken here, like anywhere that people have full control over what type of system they use, all the volume is flowing through order books in every sector of finance in crypto, outside of crypto. What that means is it's sort of the best in a generic sense.

Why isn't that the way that we're used to DEX is working? It's because they can't because there isn't enough throughput. A single order book on the Serum DEX right now is using and some single order books are using more transactions per second than the entire Ethereum network combined is. It's just like, if you think about, you have to place an order, that's going to be at least one transaction, then markets move, and you have to cancel your orders and place them at a different price. There's a few transactions, that's just constant background noise and you just can't do that on Ethereum.

Because of that, AMMs have become popular because they’re a really simplified model of an exchange that doesn't require order matching, and doesn't require canceling orders, doesn't require a liquidity provider in the same way. Thus, you can fit it better to a place where it's costing $1 per order. But I mean, mostly, I think that order books are, for most purposes, just better. One of the really exciting things about building on Solana is that it means that Serum, it has the support, the throughput to be able to handle an order, and in fact to be able to handle many of them.

“AMMs have become popular because they’re a really simplified model of an exchange that doesn't require order matching, and doesn't require canceling orders, doesn't require a liquidity provider in the same way.”

CR: I looked on CoinMarketCap today for Serum’s volume and saw that it was a little under $2 million. I don't know if that's accurate.

SB: It’s undercounting a bit, but it's the right order of magnitude. I think it's probably more like 3 million for the DEX because some markets aren't being counted, and then the AMM has another few million dollars. But yeah, that's like 5 million total between them or so.

CR: So that compares with like, $200 million for Uniswap. Why do you think this gap is coming from given, but you think order books are better and faster? Also, I wanted to get your thoughts on, DEXs: there’re still at a tiny percentage of total crypto volume, but they have been increasing and, we saw recently Uniswap overtake Coinbase Pro and so they have been kind of making a lot of headway. So I wanted to get your thoughts on both the difference with the volume on Serum, and whether, you think there’s space for AMMs to keep gaining market share.

Decaying Incentives

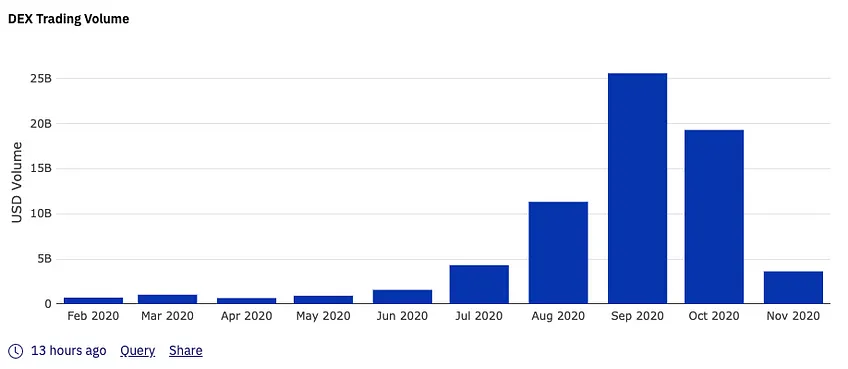

SB: So, basically, I think that there's like two pieces to this. The first is just time. Uniswap, the DEX with the most volume was launched two years ago and Serum was launched two months ago. That's an enormous difference. I feel like in centralized exchanges, no exchange launched in the last year has any volume.Any exchange launch two years ago has massive volume and there’s this really big divide. That's just like a super powerful effect. So that's one piece of this. You’d see something very different if Serum were started two years ago.

Then the second thing on is that the entire DeFi ecosystem, it's very heavily incentivized. Now, while those incentives are going down, they're still high. What's that mean? It means that people have collectively given out something $5 billion worth of tokens over the last four months to pay people to use the products. A lot of that's happened on Uniswap, a lot has happened on the other DEXs. You can get volume if you're willing to pay for it.

Note that Uniswap collects zero fees right now, and in fact really has negative fees because it's paying for the volume, whereas the Serum DEX is charging fees on the volume. It's sort of like a pretty big difference between those two paradigms. We saw this in centralized exchanges too where a bunch of new exchanges did trans-mining, which is like paying people to trade. There are like $3 billion a day volume, and everyone was very excited for a few months, then everyone realized there's nothing there. It's all paid-for volume. As soon as incentives stop, the volume stops.

You're seeing that with DeFi too. I mean, it's way up from a year ago, but it's way down from a few months ago. DeFi volume numbers were growing exponentially through about a month and a half ago, and now they're kind of like decaying away exponentially as the incentives decay away. It's sort of roughly what you'd expect.

Monthly DEX volume. Image source: Dune Analytics.

In the end, what matters is when incentives are gone, what's left? Did you successfully build a really great product and user base and ecosystem while they were there? I think it deserves mixed marks for a lot of DeFi right now. I think they successfully built a loyal, but small user base and a kind of heavily constrained product.

“In the end, what matters is when incentives are gone, what's left? Did you successfully build a really great product and user base and ecosystem while they were there? I think it deserves mixed marks for a lot of DeFi right now.”

In the last 24 hours, I see $600 million total volume on DEXs is my guess, if you got rid of incentives that goes down by a factor of two or so. It’s like 300 million or so. In contrast, if you look at like centralized exchanges, I mean, there's 12 centralized exchanges, each one of which have traded more volume than all that put together in the last day on and the top centralized exchanges have traded more than 10 times that volume in last day alone. So it's still a pretty small drop in the bucket, all things considered. Again, that's DEXs paying for volume and centralized exchanges charging for it.

CR: You said in a thread back in July, a really good thread on DeFi that true yield can be a business model, but inflation can't and it's what you're mentioning here. But with this thought that yield can maybe become a sustainable long term business model, how do you see that working, and which DeFi protocols do you think are doing a good job at it?

No Revenue in DeFi

SB: So I think that most are not, and I think long term, the model of like whenever you have yield, if it's coming from fees that the protocol is collecting, then that's totally fine as long as the protocol is still net, collecting fees. If it's something else, you're sort of just like unsustainably paying for it. Can be a good short-term marketing strategy, which is great if you do something great with that time. But you don't have infinite dollars to do it with. It's another thing to be, again, continuously giving less yield than the platform is collecting fees.

Note that almost every single platform in DeFi right now is not collecting fees. There's this myth that DeFi has revenue, it doesn’t, it's just people lying to themselves maybe, even as much as they're trying to lie to other people, talking themselves into thinking that they're making money. But liquidity provider rebates are not fees, that's not revenue. Looking at this, I mean, real fees collected by DeFi protocols per day, it's like $1,000 or something. It’s really tiny, because none of the big ones have fees.

“Note that almost every single platform in DeFi right now is not collecting fees. There's this myth that DeFi has revenue, it doesn’t, it's just people lying to themselves maybe.”

CR: But do you mean traders are paying fees to go on these DEXs, and those fees are going to liquidity providers, so what do you mean that they're not getting fees?

SB: So the protocol isn't getting fees.

CR: Liquidity providers are but the protocol isn't?

SB: That's right. So there are two ways to think about this. One, is the exchange net making money? The answer is no, it's making zero dollars, because the liquidity provider rebates are equal to the taker fees. Another way to think of it though, is like if you have a 30 bip taker fee and a 30 bip maker rebate, that's just relabeling the number line: it just sort of like saying, oh, like instead of trades happening at this phase, you shift everything over by 30 bits. So there's this price that it happens at and then this fee, but the fee is asymmetric and seeing just like shift the price 30 bips and then have zero-fee trades. It's sort of like equivalent, all it's doing is widening out the prices that the trades happen in.

It's a little bit of a subtle thing, but it usually does have an impact. It does for DEXs because it's meant to counteract the fact that you can't show bids or offers on DEXs to gain throughput. So normally, liquidity is just show a market with some width that represents their cost of execution or hedging or adverse selection or something. In DEXs you don’t have the throughput to let people customize anything. So instead, they put on this fee, which is really just saying, alright, 30 bips per side, 60 bips wide, that's how. Anyone who market makes on Uniswap is just showing you 60 bip wide market to the taker, is what it's like really equivalent to.

CR: I mean, this is just also a way to incentivize liquidity coming to DEX?

SB: Yeah, you could put it that way, it's incentivizing with all the fees paid. Because making a zero bips wide market with no incentives, and no ability to control the pricing with or anything, it generally does not tend to be a good trade.

Long Tail of Tokens

CR: So the reason why AMMs emerged in the first place was to provide liquidity for this long tail of tokens. Would you say that’s a valuable use case for AMMs and how does Serum and order books work for that?

SB: It's a good question. That is real. Even before DeFi summer, you saw AMMs did have a decent amount of liquidity for the long tail coins, right? They're trading $5 million total a day globally, but that $5 million, about half of it was coins that were basically not trading anywhere else. You can do that on an order book DEXs as well, like you can simulate AMM.

The thing is, basically, you need a market maker. You need someone to have bots that are running 24/7 updating orders, whereas in AMMs, you can just plop funds there and walk away. So the real great use case for an AMM, or one of them is you're a project and you don’t have a market maker, you’re small, you're just starting out, it's not worth finding a market maker. You just want to have some liquidity, you're willing to do bad trades for it, you just want to have something out there, AMMs are pretty good for that and I think they’re probably better than order books are for that.

“In AMMs, you can just plop funds there and walk away. So the real great use case for an AMM, or one of them is you're a project and you don’t have a market maker.”

So either you want AMM or you want some like open source bot that you just put some capital in and run and just provide liquidity on order books and you can walk away. That would be totally fine, too. It's just like a little bit more finicky than AMMs. But yeah, I think they make sense for that purpose and I think that does make sense to have automated market making to some extent. I think that it's real, and I think it represents something like a half percent of all volume in the world, but that it does make sense for that.

CR: Anatoly, I’d love to hear more about DeFi on Solana. Obviously, Serum is a big part of it. But what are the other pieces of the ecosystem, what does it look like today?

DeFi on Solana

AY: From our perspective, Serum is just a protocol and anyone can fork it. There are half a dozen teams that have used different UIs and wrapped their interfaces on top of it. We're primarily focusing on building out the tooling for people to take and run, just something as simple as the token standard. Serum and the swap implementation, those are all available, OpenZeppelin, libraries that anyone can use and use the same token interface, that makes it composable DeFi. Stuff that folks are working on in the background are lending protocols, more interfaces to wallets and things like that.

In terms of teams, we have like, I don't have that list with me, but there's a list of folks between us, Solana and folks that are participating in Serum ecosystem that are building what you see on Ethereum right now which are AMMs. AMMs have kind of split into like different kinds like Balancer Curve, trying to target different parts of what you could trade, so folks working on that as well as like the variants of lending protocols and things like that.

The Serum order book is a new primitive that's not available in Ethereum, and that's what makes it more exciting to me than just thinking of how do we replicate what's in Ethereum and Solana. For example, that spread that's calculated by market makers, like Alameda and Jump, that's basically the best Oracle money can buy. They're actually putting their skin in the game to risk an offer at a particular price that's got like a weight to it. That spread is information that's not part of the state machine. That you can then if you wanted to build an AMM that's trying to reduce the permanent loss, you can actually use that information to construct the curve that is used to trade on. That kind of like feedback loop between doing that and using the order book, I think is the exciting possibilities. But you're not going to find it Ethereum because of the lack of throughput, latency and capacity.

“The Serum order book is a new primitive that's not available in Ethereum, and that's what makes it more exciting to me than just thinking of how do we replicate what's in Ethereum and Solana.”

CR: I mean, isn't it risky to be using one pricing source for oracles for other protocols, say, lending protocols?

AY: It's not an oracle, because that's an actual offer. That’s the difference. When you get an oracle from Chainlink, and I don't know, if you saw the Chainlink announcement, we’re working with them too, there's an awesome use for that too. But what's even better is like an actual offer to buy at a particular price for a certain amount that you can take that at any given moment, and that information has a lot more weight to it. I think you can construct much more robust systems that adjust with the market conditions.

SB: So one thing I'd say is, you can put whatever additions on that you want so that one random tick won't do anything crazy on. But in the end all oracles sort of have this problem of what if the oracle price is wrong? What is wrong even mean? No one knows what the right price is.

But the best thing you can come up with for the right price is a price you can buy and sell at? Is a price where if you disagree with the oracle, you can just trade against it, until it's either you've gotten off as much size as you want, or it's the price or it’s the right price. The price you think is right. That's like true of using on-chain feed from the DEX, because if you think it's wrong, you can just go trade against it. It's way more true than an off-chain Oracle, where you sort of don't have that much recourse if you disagree with whatever calculation they're doing.

CR: It's true. It's like, more concrete rather than getting an average of multiple sources that may be outdated and you can really trade on, but now, you're getting an actual price that's on an exchange and you can trade with.

I'm interested in what you said Anatoly about Solana being able to enable different DeFi use cases and applications that just can't be done on Ethereum. What are some of the most out there, crazy ideas that you've seen?

Money Legos and Everything Legos

AY: Audius announced that they're going to build a big part of their application on Solana. To me, that is one of those out there ideas, because music is so integral to our lives, and it’s scale. Tens of millions of people, I think have the potential to go use Audius versus right now, what is the size of traders in the world. That market is just more accessible and they can do much more music stuff than trading.

Those kinds of applications, I think are farther out there because people don't typically —the kind of 2017 era, “we're going to put everything in the blockchain” thinking kind of came and went, because there wasn't any scalability there. People are talking crazy big dreams, that we're going to build this to scale, build this censorship-resistant application for the entire globe. Well, you can actually start doing that stuff now. You can build a consumer-facing applications that look and feel like Spotify that streams music that artists and everyone else can interact with and get the benefits of decentralization by cutting out all these middlemen in the music industry. That kind of stuff, to me is pretty revolutionary.

“The kind of 2017 era, ‘we're going to put everything in the blockchain’ thinking kind of came and went, because there wasn't any scalability there (…) Well, you can actually start doing that stuff now.”

But I think a really, really cool thing about it is, you look at the real world, you look at how music and movies and everything else is done. Behind the scenes is a big pile of finance that is inscrutable and really hard for folks to understand. Stuff that project Serum, and everything around that ecosystem, they're actually implementing all of that software now.

Now, you take Audius and combine that with a sophisticated audio publishing network that can borrow and lending against your revenue stream. How cool is that. You can build that. Somebody can do this in a weekend. You can take the protocol, like Audius protocol, plug it into Serum, and create a market for a token that represents royalties on the song in Audius.

Stuff like that, I think is the out there of composability. Everything we bring into the ecosystem works for the rest of it.This is like, I think, the awesome thing about the space. You're not like building this thing on your own. No matter what you're doing, even if you're working on something not related to trading, all these tools can be leveraged to really exponentially outpace, what you could do in Web 2.0. I think this is what some engineers are realizing this, some entrepreneurs are realizing this, and I think this will be what puts them ahead against everyone else outside of the space.

“No matter what you're doing, even if you're working on something not related to trading, all these tools can be leveraged to really exponentially outpace, what you could do in Web 2.0.”

CR: We're used to talking about Money Legos, but maybe now we can talk about Everything Legos.

AY: I mean, money is such a core part of everything, right? FTX run some servers on AWS, I don't know if they do, but they might and like, some other company run servers on AWS, they’re probably the same data center. They can't transfer funds between those two databases without a big pile of contracts and like humans in the middle. It's absurd, right? They wouldn't even go between those two databases, they would go outside to a bank, then like through like a three-day thing, and then back into that state. Even though the origins of the two things are really right next to each other. That's like, that massive inefficiency is going away with crypto.

CR: It's so exciting to be changing the very rails of how things work. It's pretty cool. Sam, I want to talk about your own DeFi trading activity and exploits. Because in the DeFi summer, Alameda, FTX and I don't know if you personally, but you amassed large amounts of different governance tokens, in some cases, big enough to actually have a big influence on these protocols. I was wondering about your strategy with this. Was it to participate in governance in the long term or was it more short-term trading driven?

Short-Term Profit

SB: I mean, there's a lot going on there and I'm sort of not in charge of all those decisions. But I think what I would say is, by default, and this doesn't apply everywhere, and there's always sort of special cases. But as a default, Alameda is in the business of liquidity providing and arbitrage and what it does are positive expected-value trades rather than things like governance plays.

“Alameda is in the business of liquidity providing and arbitrage and what it does are positive expected-value trades rather than things like governance plays.”

That's not to say that it will never participate in governance. But a pretty good default, yes, is that the goal is just doing positive EV trades on sort of shorter timescales as a default. I think that was the majority of it, not looking to have particular influence on protocols or anything like that. Now, separately, sometimes protocols will come to us for advice, sometimes there are other relationships that we have, but doesn't tend to be expressed through the trading.

CR: It's interesting, because these are namely governance tokens, they're kind of meant, supposedly to give users ownership and the ability to participate in decisions. But in your case, we saw pretty clearly that often that's not really what they're used for.

SB: I think governance token is to some extent a catch-all, and doesn't literally just mean can cast votes, but also can do whatever else governance votes for them to be able to do. That gives them a life of their own, and makes them often interesting products to trade as well.

“I think governance token is to some extent a catch all, and doesn't literally just mean can cast votes, but also can do whatever else governance votes for them to be able to do.”

CR:. Then I want to dig a little bit deeper into the couple of incidents you had with these tokens. There was what some may call the gaming of the Balancer liquidity mining program, and getting large amounts of collateral in Cream to short UNI and YFI. So it's earning you this reputation of like a DeFi villain for some people. So I’m wondering, first of all, what are your thoughts on that? Then is there any ethical barrier for you when making trading decisions?

No Sympathy

SB: So I think on the Cream one, it's worth splitting in two things. The first is should there be a different collateral ratio or limit on collateral or something like that? For individual tokens in the protocol, I think it would be totally reasonable to change some of those parameters. I would be in favor of some changes, including some changes that might decrease the amount of collateral that Alameda has. You could make decent arguments that there are tweaks that are good for the protocol.

But I kind of think it's f*cking ridiculous the central claim, that it's bad or evil or manipulative to use a borrow/lending protocol to lend one asset in order to borrow another. That’s the whole f*cking point of it. If people aren't lending out one type of digital asset or to borrow another, that's the entire reason it exists, is the only reason it has value, and it’s the only reason anyone uses it.

It's just like, and honestly, what triggered this? There's a lot of really b*tthurt a**holes who are long YFI and are sad that someone else was borrowing it. I don't know, I just have no sympathy for that position there. It's pretty ridiculous.

“… it's f*cking ridiculous the central claim, that it's bad or evil or manipulative to use a borrow/lending protocol to lend one out asset in order to borrow another.”

First of all, I think people have no sense for what the scope of what would have massive impact on something like that, is a lot bigger than through YFI or something. Second of all, it's really hard to figure out what a trading position is, people are wrong half the time. Because all they see is one single lending protocol, they don’t see all the centralized exchange trading. They don't see the staking. They don't see everything else. Was it to steak, to provide liquidity, to sell, to hedge? Who knows? I don't know, you're seeing like 5% of the total activity. So it's really hard to fit that into a bigger picture of the whole.

So separately from like, it being the entire point of a borrow/lending protocol. Also, it's very hard to extrapolate just from that, what an overall book necessarily would look like, which again, I think all these are separate things from like, should there be a change to the collateral ratio for some of these things? I think you could make a decent argument for yes there.

CR: That's pretty clear. So you gained this reputation, but on the other hand, I think it's so interesting that you've stated that a lot of the profit that you make from these apparently selfish trading strategies, that you end up donating to charity. I would love to hear more about this concept of, what was it, efficient altruism? How does it reconcile with your trading?

Effective Altruism

SB: Yeah, effective altruism. I think that in the end, my goal is to be able to have whatever the most positive impact I can on the world is, and I think that there are a lot of ways that you can do that. But one way is through figuring out what the most effective places you can donate to are, and how you can donate as much as possible to them.

“My goal is to be able to have whatever the most positive impact I can on the world… one way is through figuring out what the most effective places you can donate to are.”

I think that's what I've been doing really for the last seven or so years. I mean, I've been donating, reasonable amounts each year, Alameda has, and that's ultimately the goal. Where that is can depend and I don't think it's obvious what the right answer is. I think there are good arguments for a lot of things, whether it's sort of like, global poverty charities, animal welfare charities, future-oriented charities, I think that there's a lot of good work being done on that, and it serves a pretty cool field.

But I think that's been pretty exciting, and together it’s given, I think upwards of $20 million or so over the course of the last whatever seven years or so. I mean, I'm sort of really grateful that there are a bunch of other people who've worked for Alameda or FTX and who have also given a lot. So, that's ultimately what I care about.

One thing, also that, I would say is that there's this interesting thing, when it comes to trading, like, what does it mean to provide liquidity? It means to find a place where there are too many buyers relative to sellers, or too many sellers relative to buyers. A place where there's a mismatch in supply and demand, and markets are sort of blowing out and getting inefficient because of that and to find a way to provide liquidity there, to find a way to take whichever side there isn't enough.

In doing so, you make markets more efficient. So you can imagine Bitcoin trading at $10,000 on Coinbase and $11,000 on Bitstamp, and there's an arbitrage there, obviously, where you buy on Coinbase and sell on Bitstamp. So you're making money doing it, but what else are you doing well, there's a guy trying to buy Bitstamp and probably tricked by a lot, way more than there is liquidity, he was getting sort of worse and worse price. Someone had to go in there and be there for them to allow them to get their execution off. By doing that arbitrage, you actually make their execution better, and you make the markets more efficient, because you sort of make prices more in line between the venues.

So there's this interesting duality between arbitrage and market efficiency where when you provide liquidity, you sort of simultaneously on at least in many cases, do both. That can be thought of really kind of directly as like Bitcoin trading at different prices on different platforms, or it could be sort of like a more generalized version of that. Whether it's like huge staking rewards, not enough stake, huge amount of stake, not enough staking rewards. Whether it's some asset that's being over or under bought, like there's a lot of variants on this, and it sort of becomes more of this generalized sense of, is there something lopsided going on here?

CR: Does that connect to your charitable work because you see, maybe causes or institutions in the world that are missing liquidity in a sense that there's this misbalance on maybe giving to charity is kind of like providing liquidity or doing arbitrage, but instead of making a profit off that arbitrage, you're making maybe just some other kind of profit, just like you're good with yourself or something?

SB: Yeah, I think so, but I don't see that as a primary thing. I mean, I think that there is good in making markets more efficient. I don't think that taking two Bitcoin USD order books, and making their prices more in line with each other is like the greatest good you can do in the world. I don't think that inefficiency was the world's most glaring problem. I see this more as an argument that liquidity providing is net positive rather than net negative for the world, rather than trying to argue that it's value is on the same level as preventing people from getting malaria, because I don't think it is.

CR: So for you, it's like a tool to make a profit, and then give that money for people getting malaria?

SB: Yeah, with the caveat that I also think that it is itself helping the world become more productive and efficient. I think that it is important to me that I do see it as sort of like net good instead of like net bad.

CR: So interesting. We haven't really talked about another core thing on Solana, which is like its interoperability. So Anatoly, just wanted to touch on that, like, how is Solana right now integrating with Ethereum, and where is that kind of working right now, and how has it helped drive activity if at all?

Cryptography for All

AY: When you have two programmable ecosystems, somebody will go and build a bridge between them. It just kind of happens. There's arbitrage between the cost of doing business in Ethereum and doing the equivalent thing on Solana, which is much, much cheaper. So somebody will figure out how to make that happen.

“…when you have two programmable ecosystems, somebody will go and build a bridge between them. It just kind of happens.”

So far, there are two projects that have done a great job. The wallet that Serum uses, Sollet has a built-in bridge for BTC and Ethereum. So you can move funds into the ecosystem in under a minute, and much longer with BTC, right, so but I think with Ethereum, it's under a minute. One of our validators Service One, awesome kind of security folks, they're building a bridge called Wormhole, that's up and running and out whole hackathon was going to focus on that. So that's another solution.

Bridges are part of efficient tradeoffs. The goal is to make them as collusion and intrusion resistant as possible, and then you can pick your poison there which techniques you use. In a big picture way, I think that Layer 1, Layer 2 consensus stuff is an implementation detail; the key part we're solving for people is enabling 10 billion people to use cryptography. There's very small number of people who have access to wallets and keys that they can sign with. There's no way you're going to get all 7 billion people on the planet to do that on Ethereum.

All these applications that are using cryptography to do these very powerful things, I'm guessing they're going to use Solana because we're the fastest cheapest way to scale cryptography, but we're an implementation detail to that ultimate goal, right, to really empower people with those tools. How you get funds between Ethereum and Solana? There are tons of different ways to do that. I think the more exciting thing is actually getting the end-user to go use this stuff.

CR: I love that core big vision for you. Why is it important to you that people are using these cryptography tools?

AY: It is, I think, transformative in like a real-world sense for people to have access to cryptography. Because the things that you see in the world right now that are like poison, like, I don't know, the Twitter newsfeed, fake news, that kind of stuff, I think there are really powerful ways to deal with those things if everybody had cryptography. A governance token is a much more powerful social network than Facebook, because it costs money to participate in this network. You have to go buy this token. So it is naturally resistant and the folks that are participating in these networks are much more aware of what's going on there.

They yell at Sam when they don't like something. But that's awesome. That's part of a very healthy, self-sufficient ecosystem. Those people that are part of this feel ownership of it and that's all done with cryptography. You can't replicate this on Facebook. There are pockets of this in Reddit, but I think these systems, if they scale up to the entire world, I think we'll make it a much safer, fair place. People all over the world can now lend to each other, bypassing all the middlemen and all the bullshit with no fees. How awesome is that?

“They yell at Sam when they don't like something. But that's awesome. That's part of like a very healthy, self-sufficient ecosystem.”

Very dumb kind of back in the envelope reductionist view is. You look at McKinsey, they say like $20 trillion is spent on moving finance stuff. These companies in the world of finance make $20 trillion a year. That's 20% of the world's GDP. Take all of that and replace it with software, and let's say that software stack, Solana, is making a trillion a year, still absurdly, ridiculously successful. Biggest thing in the world and you’ve effectively removed 95% of the cost. People can work four days a week, have the same standard of living, as they did before. That is like, I don't know what else I could be working on, like that’s awesome.

“ Biggest thing in the world and you’ve effectively removed 95% of the cost. People can work four days a week, have the same standard of living, as they did before. That is like, I don't know what else I could be working on, that’s awesome.”

CR: Oh, that’s so inspiring. I'm going to leave this call and be like, yes, Blockchain!

AY: These are like, ridiculous transformative tools.

CR: I agree. Love the big vision. Then to end this call, Sam, I was just very curious to ask this question. Do you think Serum will someday beat FTX in volume? Just as an example of the bigger question, will DeFi beat centralized finance?

Will DeFi beat CeFi?

SB: That's a really good question. I don't know. I could honestly see that going either way. I could see a world in which DeFi really takes off. I could see a world in which it never quite does. What's the difference between those worlds? There's a lot of things you could imagine. But my guess is that one of the big things there is going to be to build the products that people want to use well enough for people to use them. Is everyone's takeaway in the end, this is a place full of useless scams, or this is a place with endless possibilities that has all these advantages and yet is also replicating the products that we've come to know. They're both within the world's power, and I think I don't know exactly which way it's going to end up and I don't know if we're going to end up in some mixed world, some uncertain world or if one of them is going to end up really becoming quite a bit bigger than the other.

The Defiant is a daily newsletter focusing on decentralized finance, a new financial system that’s being built on top of open blockchains. The space is evolving at breakneck speed and revolutionizing tech and money.

About the founder and editor: Camila Russo is the author of The Infinite Machine, the first book on the history of Ethereum, and was previously a Bloomberg News markets reporter based in New York, Madrid and Buenos Aires. She has extensively covered crypto and finance, and now is diving into DeFi, the intersection of the two.

Get an edge in Crypto with our free daily newsletter

Know what matters in Crypto and Web3 with The Defiant Daily newsletter, Mon to Fri

90k+ Defiers informed every day. Unsubscribe anytime.