It Isn't Just the SEC — Feds' Dragnet Targets Crypto Banking, Too

The Securities and Exchange Commission. The Office of the Comptroller of the Currency. The Federal Deposit Insurance Corporation. The National Council of Economic Advisors. The U.S. Justice Department.

This year, an alphabet soup of U.S. agencies have scrutinized the crypto industry like never before. They are wielding indictments, lawsuits, investigations, and penalties to rein in the largely unregulated market. No surprise, crypto folk are none too pleased with the development.

Shut Off

The Feds’ actions have been called a war, an attack, and a bid to kill blockchain technology in its adolescence.

“The breadth of this plan — spanning virtually every financial regulator — as well as its highly coordinated nature, has even the most steely-eyed crypto veterans nervous that crypto businesses might end up completely unbanked, stablecoins may be stranded and unable to manage flows in and out of crypto, and exchanges might be shut off from the banking system entirely,” wrote investor and influencer Nic Carter n a widely-read essay this month.

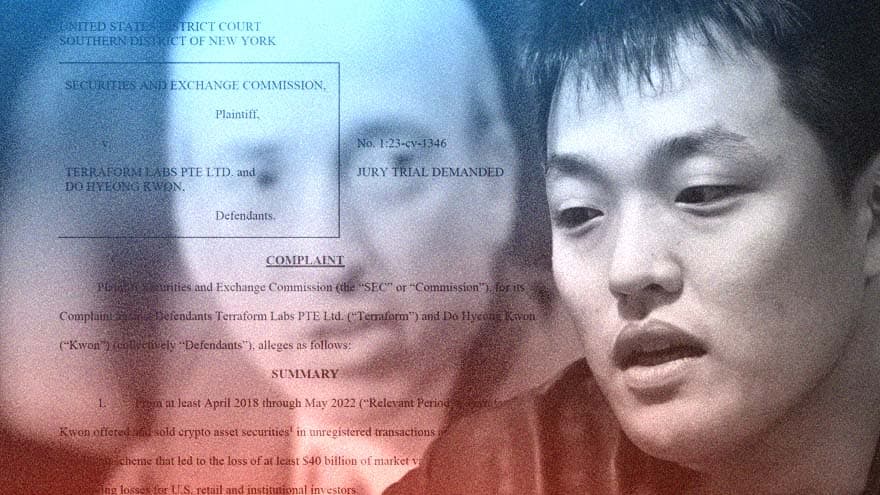

SEC Defines 'Interrelated' Terra Tokens as Securities

Feds Charge Do Kwon and Terra With Fraud in Case With Deep Implications For Crypto

While the SEC has made the biggest headlines with its spate of recent cases, bank regulators are driving equally profound action. For all the hew and cry over FTX’s failure, it was the crisis at Silvergate Capital Corp., a commercial bank that served crypto firms, that truly spooked officials, according to a source who spoke to The Defiant.

“I think people under-appreciate how terrified the Silvergate developments have made the federal government,” said a source at a D.C.-based crypto advocacy group who requested anonymity to talk about a sensitive subject.

Legal and policy experts who spoke to The Defiant said it’s too early to conclude that U.S. regulators are indeed trying to “de-bank” crypto, or thrust it outside the traditional financial system altogether.

And Gary Gensler, the chair of the SEC, argues regulators want the opposite — to bring crypto inside “the perimeter” as just another asset class governed by the same laws as other securities.

Marginalize the Industry

Yet crypto leaders feel under siege and frustrated that the SEC and its sister agencies are not recognizing blockchain-based digital assets as a new breed that warrants bespoke legislation and regulations. By applying traditional securities laws to the space, the belief is that Washington is out to marginalize the industry.

Cody Carbone, vice president of policy at the Chamber of Digital Commerce, told The Defiant, it may be too early to draw that conclusion. “But I think you can make the argument either way. … If [regulators’] end goal is to de-bank crypto and completely eradicate the use of cryptocurrencies in the U.S., I think the path that they’re taking is probably a good start.”

‘I think people under-appreciate how terrified the Silvergate developments have made the federal government.’

The scrutiny of crypto began during the Obama Administration in a coordinated program dubbed Operation Choke Point. At the time, the Justice Department and banking regulators discouraged banks from servicing certain “high risk” industries, such as payday lenders and gun vendors. The program ended after Donald Trump was elected president.

Operation Choke Point

“We share your view that law abiding businesses should not be targeted simply for operating in an industry that a particular administration might disfavor,” Stephen Boyd, Trump’s assistant attorney general, said in letters to a trio of congressional Republicans.

If the current wave of crypto regulation is a reprise of Operation Choke Point, the playbook has changed, according to Julie Hill, a professor at the University of Alabama School of Law.

“Operation Choke Point was all behind closed doors until members of Congress found out about it and turned it into a huge investigation,” she said in an interview Thursday. “This is a little different, in that we’ve got some public statements at least, where they’re being a little more forthcoming about what they want. Now, that doesn’t necessarily mean that there aren’t things going on behind closed doors that we don’t know about.”

Hayes Shares Why He Loves GMX and Is Bullish on DeFi

Crypto Investor is No. 1 Individual Investor in Yield-generating Token

One of the first signs a new, coordinated effort was underway came in January. In a little noticed move, the Federal Reserve, the Federal Deposit Insurance Corporation, and the Office of the Comptroller of the Currency released a joint statement concerning “crypto-asset risks to banking organizations.”

“It is important that risks related to the crypto-asset sector that cannot be mitigated or controlled do not migrate to the banking system,” the joint statement reads.

The statement goes on to say that banks are “neither prohibited nor discouraged from providing banking services to customers of any specific class or type.” Yet Carter argues it is “a strong deterrent to any bank considering aligning itself with crypto.”

Senior advisors to President Biden expressed their fear of contagion from the crypto sector in a blog post published Jan. 27.

“In the past year, traditional financial institutions’ limited exposure to cryptocurrencies has prevented turmoil in cryptocurrencies from infecting the broader financial system,” members of the National Economic Council wrote. “It would be a grave mistake to enact legislation that reverses course and deepens the ties between cryptocurrencies and the broader financial system.”

Run on Deposits

The Silvergate episode crystallized regulators’ fears that crypto might jump its banks and flood the financial mainstream with problems. The San Diego-based bank jumped headlong into crypto years ago and serviced a number of firms and protocols. In January, it shocked watchdogs when it had to borrow $3.6M from Federal Home Loan Banks to stem a run on its deposits. A competitor, Signature Bank, did the same, borrowing $10M, according to The Wall Street Journal.

“Their need to tap the federal home loan [banks] made people afraid that counterparty risk in crypto would spill over into the traditional financial system,” said the Washington source.

Even before the collapse of FTX, regulators were wary of banks like Silvergate and Signature. Those banks were required to maintain more liquid balance sheets than their more traditional counterparts, according to Professor Hill.

“In some ways, Silvergate is a positive story, because if a normal bank had had that big of a percentage of its deposits run off, they would have failed,” she said.

Nevertheless, it seems banking regulators don’t want to take more chances.

On Jan. 27, the Fed denied an application for membership in its system from crypto bank Custodia. That same day, the Fed’s Kansas City branch denied Custodia’s application for a so-called “master account.”

“Check processing, wire transfers, [the Fed] provides all that technology to banks,” Hill said.

Closed Accounts

Custodia could instead access that technology through a partner bank — like Silvergate — but it would be costly. A master account would have been a boon to Custodia’s business. And membership in the Federal Reserve system would have paved the way for a master account.

Kraken also has a master account application pending. Custodia’s denial doesn’t bode well, according to Hill.

“They had had a bunch of their bank accounts being closed,” she said. “And they thought it was a big operational risk … to always have to rely on some other bank to provide them payments processing.”

‘The SEC took awhile, but I think at some point learned the lesson that if they had a light touch, they would get blamed when things went wrong.’

Marc Fagel

Meanwhile, the SEC’s clampdown has drawn the most ire from the crypto community. That’s primarily because the agency is broadly defining virtually all cryptocurrencies and yield-bearing crypto products as securities or investment contracts.

On Feb. 9, crypto exchange Kraken settled a lawsuit filed by the SEC and agreed to pay a $30M fine and end its staking-as-a-service program in the U.S. A few days later, Paxos bowed to an order from the New York state’s Department of Financial Services, and said it would cease issuing new Binance-branded stablecoins.

Registering an Asset

And on Thursday, the SEC essentially branded all cryptocurrencies securities in a lawsuit accusing Do Kwon and Terraform Labs of defrauding U.S. investors of billions of dollars. That’s huge. For years, the crypto industry has resisted the idea that tokens can be swept up in the same regime that governs stocks, bonds, and other TradFi products. The SEC just said no dice.

Registering an asset with the SEC can be time-consuming and costly. One crypto firm spent $2M on legal fees alone, according to a report from DL News.

Marc Fagel, a former SEC attorney who spent more than a decade at the agency, said the SEC’s aggressive posture this year was to be expected given the spectacular collapse of FTX, which went from being worth $32B to bankruptcy in the space of a few weeks.

Least Resistance

“The SEC took awhile, but I think at some point learned the lesson that if they had a light touch, they would get blamed when things went wrong,” Fagel said. “So the path of least resistance is look for the clear violations of existing law, try to clamp down where you can and you’ll let other people yell at you for being heavy handed. But at least you’re not having another FTX on your hands.”

Even as the regulatory dragnet tightens, the crypto industry is hoping lawmakers may ride to the rescue with legislation that would set bespoke boundaries, rules, and most importantly, recognize blockchain-based tokens as a distinct asset class with its own legal regime.

The odds are slim, however.

“Yeah, some of that is congressional dysfunction,” Fagel said, “but some is: who wants to be responsible for saying, ‘We’re going to make it easier for crypto,’ when depending where you stand on the issue, some or all of it is a scam.”

Tough Place

Carbone agrees.

“You have to try to put yourself in [regulators’] mindset, and they were in a tough place” post-FTX, he said. Regulators’ wondered “What can we do quickly to kind of stem the tide of some of these companies going under, that will also give us goodwill with the administration [and] look like we’re protecting consumers?”

Balancer Shakes Off Rivals' Shadow With Novel Strategy

Aura Finance Casts Spotlight on Exchange Amid LSD Rally

Gensler’s critics argue that, despite the chairman’s commitment to “protecting” retail investors from bad actors, he has done a poor job getting in front of the industry’s biggest train wrecks. Fagel says those critics are missing the point.

“The SEC can say, ‘We got FTX right. We didn’t make it easy for [FTX] to do their business in the U.S. As a result, they were in the Bahamas,’” he said. “So yeah, it was a big explosion, but people who were putting their money in FTX were non-U.S. investors trading unregistered assets on an overseas exchange. Isn’t that better for American investors than if we gave [FTX] a green light to operate here, and you had a real blow up, not just with FTX, but in the American financial system?”

End Goal

Through blog posts and statements, the Biden Administration has stressed it wants to limit crypto’s influence on traditional financial markets. But observers aren’t sure where that leaves the industry, or when the regulatory deluge may recede.

“I think that if you were to ask the regulators, you know, what was their end goal? I’m not sure they have an answer,” Carbone said.

But their approach is likely to push companies, investment and talent overseas, he added. Even jurisdictions known for their heavy-handed approach to regulating business, like the European Union, have done a better job giving crypto companies clear guidelines they can follow without fear of running afoul of the law.

Financial Hub

“The incentive for innovators and businesses is to go abroad,” Hayden Adams, CEO of Uniswap Labs, wrote on Twitter. Two days later, Coinbase CEO Brian Armstrong said the U.S. “risks losing its status as a financial hub long term.”

Carbone warns lawmakers that jobs, tax revenue and the U.S.’s status as the world’s leader in tech and finance may be on the line.

“I’ve gotten pushback from a lot of members of Congress who said, ‘Nah we won’t lose, we’re the United States! Come on, the internet started here! Companies really aren’t going to leave California or New York to go to, like, England or Portugal,’” he said. “And I’m like, ‘Yeah, they are.’ … They’re not seeing how imminent the threat is.”

Advertisement

Get an edge in Crypto with our free daily newsletter

Know what matters in Crypto and Web3 with The Defiant Daily newsletter, Mon to Fri

90k+ Defiers informed every day. Unsubscribe anytime.