Christensen Under Fire After MakerDAO Members Vote for His Reorganization Plan

Rune Christensen has won. But now the real contest begins.

That’s the upshot of a just-closed vote taken by MakerDAO members and the backlash to its implications in the DeFi community.

The members of DeFi No. 1 protocol voted overwhelmingly in favor of making big changes to the project’s structure in line with the Endgame roadmap laid out by Christensen, MakerDAO’s founder, in May.

Bad Proposal

But the vote, poll #882, has come under fire from prominent voices in the web3 industry, who say only 15% of circulating MKR, Maker’s governance token, was mobilized to vote. Moreover, votes delegated by Christensen represented nearly three quarters of those cast.

“The Endgame Plan is an exceptionally bad proposal, and it’s really sad for Maker that it passed the signal (shoved through by [Rune Christensen] single handedly in face of strong and justified criticism),” said Hasu, a MakerDAO governance delegate and strategy lead at Flashbots.

MakerDAO Poised to Break Up Into 'MetaDAOs' in Historic Shakeup

Maker Members Voting on New Reorganization This Week in Series of Votes

Yet Christensen said voter participation is one of the problems he flagged months ago and is at the heart of the raft of changes he’s proposing. “It has been clear since the dissolution of the Maker Foundation that a lack of voter participation and open-ended governance complexity are existential risks to Maker and DAOs in general,” Christensen told The Defiant.

“Overcoming this fundamental challenge is what the Endgame Plan is designed to solve, using decentralized mechanisms such as voter incentives, limited and immutable scope of governance complexity, and replacing unaccountable black box budgets with performance based incentives such as a revenue share, as well as other checks and balances.”

Delegates

Sebastien Derivaux, an asset-liability manager at MakerDAO, shared data showing that three quarters of the votes were cast by delegates backed by Christensen.

“While 122 persons have voted, only one matters as he represents 63% of the turnover and 74% if we use influence,” tweeted Derivaux. “It doesn’t have to be this way as MKR is quite decentralized in holdings, just people don’t vote nor delegate.”

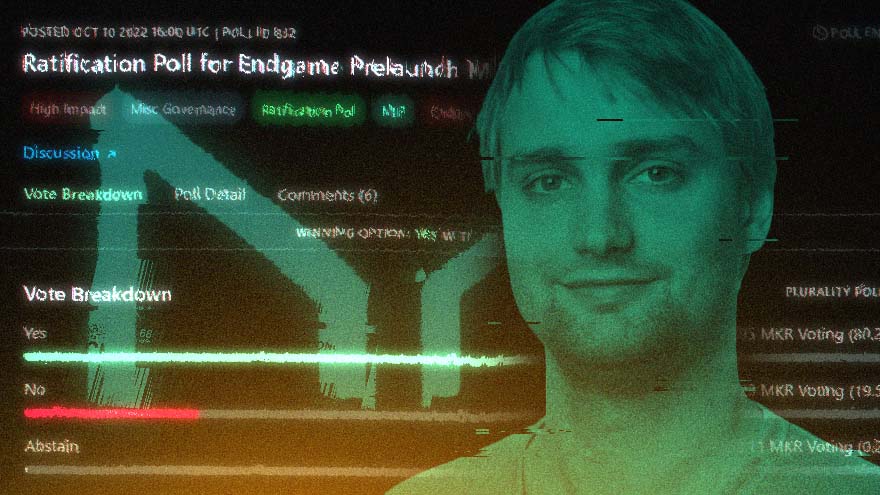

Vote breakdown for MakerDAO governance poll #882. Source: Sebastien Derivaux

This episode is just the latest flashpoint in Maker’s effort to balance its cooperative governance model with the imperative to generate revenue growth. At the same time, Maker and Christensen are wrestling with the best way to address regulatory risk in the wake of the Tornado Cash sanctions and the exposure of stablecoins to Washington’s enforcement actions.

MakerDAO is a collateralized debt protocol allowing users to mint its DAI stablecoin against collateral assets. It is the largest DeFi protocol with a total value locked of $7.5B, according to The Defiant Terminal.

Suite of Proposals

On Oct. 25, the Endgame Prelaunch Maker Improvement Proposal Set passed with 80% support. The poll represented a suite of proposals to radically overhaul MakerDAO’s structure per Christensen’s Endgame thesis.

In Endgame, Christensen lamented that Maker’s decentralized governance was failing due to voter apathy, competing factional interests, and the increasing complexity of MakerDAO’s operations. He called for reorganizing Maker into a series of self-sustaining MetaDAOs that will autonomously develop their own business models and growth strategies and operate in parallel.

Winklevoss Offers MakerDAO Deal But Christensen May Be Underwhelmed

Gemini's Offer to Deposit Stablecoin with Maker is Latest Tempting CeFi

Each MetaDAO will have its own token and voting committees, with tokens issued through yield farming to incentivise governance participation. The structure will also allow Maker to compartmentalize and manage risky activities such as real-world asset lending by designating the specific MetaDAOs.

MakerDAO will now launch six MetaDAO “clusters” tasked with developing the governance process for MetaDAOs. Maker will also create a “Protocol-Owned Vault” tasked with accumulating stETH, and expand the scope of the project’s DAO-based governance to include issues relating to MetaDAOs.

The proposals also transfer governance over onboarding and offboarding collateral assets from Maker’s existing governance structure to its Strategic Finance, Risk, and CES Core Units.

Real World Assets

However, the vote was largely panned on social media for its low vote-count and the influence of Christensen over the delegates that participated.

“It is really sick that a proposal that so dramatically changes… every part of the protocol, can pass with less than 15% vote participation,” Hasu said on Twitter. “If there had been a 50% quorum, at least [Christensen] needs to lobby and convince other holders to get his proposal passed… I hope that other projects take what happened at MakerDAO as a lesson and develop a staggered governance system.”

Nick Garcia, the CEO of Fortunafi, agreed. “Prime example of the current dismal state [of] protocol governance,” he tweeted. “You cannot fix a governance layer like this. It simply must be rebuilt from the ground up.”

‘Prime example of the current dismal state [of] protocol governance. You cannot fix a governance layer like this. It simply must be rebuilt from the ground up.’

Nick Garcia

The London Business School Blockchain Society was among the delegates that voted against the proposal set.

“The most important problem that we see with Maker right now is the lack of consensus over its overriding object/strategic purpose,” tweeted Park Y, a representative of the society. “Unfortunately, Endgame introduces new and complex governance features that don’t necessarily solve for this core problem.”

The Endgame plan also seeks to establish a roadmap for Maker’s real-world asset adoption moving forward.

Regulatory Risk

Christensen’s original Endgame plan spoke favorably of RWAs, arguing that MetaDAOs offer a more efficient structure for Maker to increase its exposure to real-world institutions and diversify its sources of revenue.

However, after the U.S. Treasury Department sanctions on Tornado Cash prompted Centre to blacklist 38 wallets holding USDC, Christensen changed his mind and asserted that RWAs including centralized stablecoins could comprise a dangerous source of regulatory risk.

An updated version of the Endgame plan argued that MakerDAO should restrict its RWA exposure to no more than 25%. Christensen also said Maker freely float DAI against the dollar within three years, attracting pushback from many in the web3 community community.

“Giving up price stability to pursue RWA appears a terrible tradeoff in our view,” Park Y argued. The core product of Maker is DAI, meaning price stability should be its #1 objective. A float would cause a loss of confidence that is far more detrimental.”

“We think there can be a viable middle ground in navigating this tradeoff — perhaps one that sees MakerDAO building up a diversified collateral portfolio of ETH, stables, other on-chain assets, RWA, rather than extremities of either,” Park Y continued.

“Endgame is only bad if it unpegs the actual DAI,” said Curve Finance, the top DEX by TVL.

Now comes the crucial next stage in MakerDAO’s reorganization.

Negative Target Rate

With the passing of poll#882, MakerDAO is expected to vote between three different strategies for managing its RWA exposure and DAI’s peg: “Pigeon Stance”, “Eagle Stance”, and “Phoenix Stance.”

Under Pigeon Stance, which assumes the threat of regulation is low, no limit would be placed on Maker’s RWA exposure and DAI’s peg to the dollar would be maintained for at least two-and-a-half years.

Eagle Stance would result in DAI become free floating after the same period, possibly alongside a “negative target rate” intended to reduce demand for the token. Phoenix Stance would prohibit any RWA exposure “to ensure maximal protection against regulatory crackdown.”

Advertisement

Get an edge in Crypto with our free daily newsletter

Know what matters in Crypto and Web3 with The Defiant Daily newsletter, Mon to Fri

90k+ Defiers informed every day. Unsubscribe anytime.