Desperate To Get Crypto Out of FTX, Some Get Creative

With withdrawals from FTX limited to Bahamian customers, some have found a clever way of spiriting their money out of the bankrupt crypto exchange.

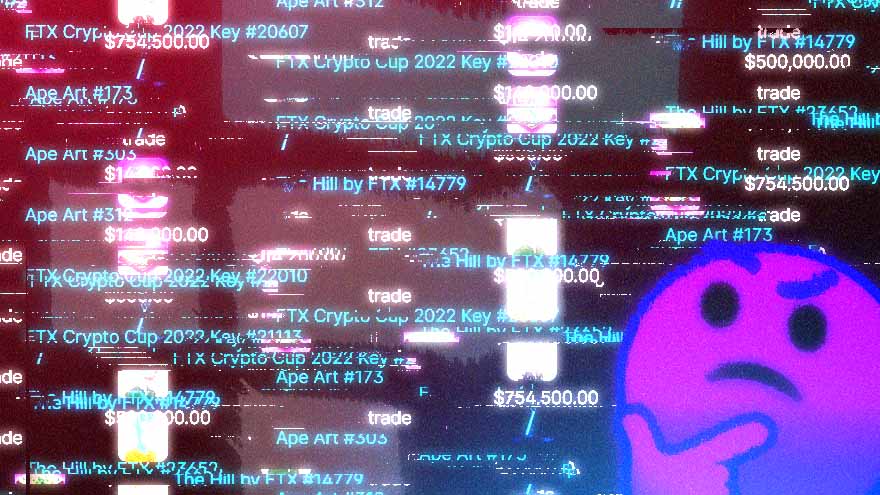

FTX’s Bahamian users are listing NFTs on the platform “at a wildly marked-up price,” according to Andrew Thurman, a researcher at Nansen. Foreign users with crypto trapped on FTX are buying the NFTs, with the crypto used for the purchase then sent to a wallet of the non-Bahamian users’ choice.

Ape Art #312 Sold For $10M

As of noon Friday, FTX’s NFT marketplace — which was “never terribly popular,” Thurman said — had processed about $20M in volume since FTX re-enabled withdrawals Thursday morning.

“This appears to be the first recorded case of NFT utility in existence,” crypto influence Cobie sarcastically tweeted early Friday.

When FTX re-enabled withdrawals Thursday morning, observers cheered. But their hope that customers might have a shot at retrieving the billions they’d stashed on the platform quickly turned to skepticism.

Preferential Treatment

On-chain sleuths noted most withdrawal requests were still failing, and that successfully withdrawn funds were often going to newly created crypto wallets, arousing suspicion that friends of FTX executives were receiving preferential treatment.

“Some people just assumed it was you know, garden variety rat f@#king and FTX was just letting friends and family withdraw,” Thurman said. “But nobody could quite figure out how to make it work. And a lot of users were reporting that even though there was this clear and unassailable on-chain evidence of withdrawals, that they still couldn’t [withdraw] themselves.”

Fresh Wallets

A “significant percentage” of withdrawals went to fresh wallets, he added, but there are “totally anodyne” reasons for withdrawing one’s funds to a wallet without any on-chain history. FTX employees paid in crypto may have had money deposited directly in their FTX account, for example; those employees wouldn’t have had to go on-chain before the exchange collapsed this week.

Others might simply want to preserve their privacy with the entire industry tracking the flow of money out of FTX.

FTX’s announcement that the funds were going to Bahamians per “our Bahamian HQ’s regulation and regulators” quelled some of the speculation. But it also led to a flurry of suspicious transactions like the NFT workaround described above, Thurman said.

One user was able to withdraw $9M in stablecoins, according to Nansen data.

“Is there a born and bred Bahamian who’s got 9 million in stablecoins to withdraw from FTX? I don’t know,” Thurman said with a laugh. “You can only speculate. It’s impossible to tell.”

Customers managed to withdraw about $50M in the 24 hours after withdrawals were re-enabled, according to Nansen data. Curiously, however, some users chose to deposit money in the bankrupt platform.

Risky Arbitrage Opportunity

“When you have an exchange that’s undergoing this kind of volatility, whose market maker is now bankrupt and isn’t active anymore, there are some incredible arbitrage opportunities,” Thurman said. At one point, ETH was trading $200 lower on FTX than other exchanges.

“If you have an absurd risk tolerance, and you are the most degenerate ape under the sun, depositing funds, making some money off of some clever arbitrage and then withdrawing through a Bahamian resident’s account, somebody’s going to be able to make money off of that,” he said.

Advertisement

Get an edge in Crypto with our free daily newsletter

Know what matters in Crypto and Web3 with The Defiant Daily newsletter, Mon to Fri

90k+ Defiers informed every day. Unsubscribe anytime.