MGUSD, Explained: How MoneyGram Built a Stablecoin Around Distribution

A customer sends $200 through a remittance app, then learns the recipient needs $250. They cancel to resend the right amount, and the refund takes up to 10 business days to land back on their card. For households that send money home from every paycheck, the funds are unusable in the meantime.

That delay is one of several frictions in cross-border money movement. Sending $200 internationally cost an average of 6.36% in the third quarter of 2025, per the World Bank. A recipient picking up cash has no way to keep part of the transfer in dollars.

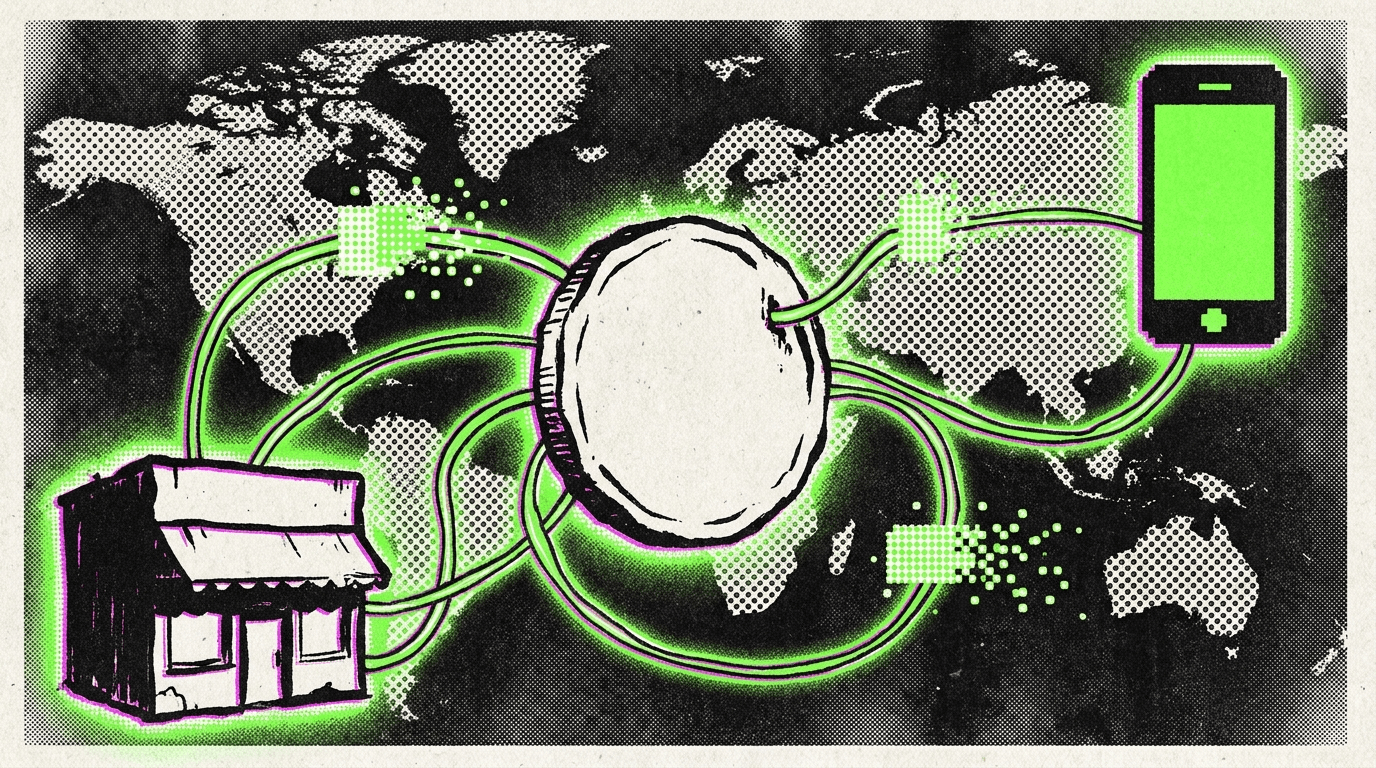

MoneyGram, one of the world's largest money-transfer networks with more than 60 million active customers and nearly 500,000 retail locations, is betting a stablecoin can remove some of those frictions. On June 2, the company announced MGUSD, a native U.S. dollar stablecoin issued on Stellar and embedded in the MoneyGram app as a self-custodial dollar balance. MGUSD launched in the U.S. market, with plans to scale globally.

A Stablecoin Built for Distribution

Stablecoins hold more than $310 billion in circulation, per DefiLlama, dominated by Tether's USDT at roughly $187 billion and Circle's USDC at $75 billion. Nearly all of that supply was built around the asset itself: tokens designed for exchanges, DeFi, and treasuries. MGUSD inverts the order. The token starts inside a consumer product that already moves money, for customers who may never interact with a blockchain directly.

"The stablecoin market has largely focused on the asset itself. MoneyGram is taking a fundamentally different approach. Starting with our distribution platform, we're using stablecoin as a foundation to build future applications on our global network," Anthony Soohoo, MoneyGram's chairman and CEO, said in the launch announcement.

The Four-Layer Stack Behind the Balance

Four companies each handle one layer, per the announcement. Bridge, the stablecoin platform Stripe acquired for $1.1 billion, is the regulated issuer. That puts MGUSD under the GENIUS Act, the federal law requiring 100% reserves and monthly reserve disclosures.

M0 provides the mint-and-burn smart contract infrastructure, and the token deploys on Stellar. MoneyGram distributes from Fireblocks wallets to customer wallets embedded in the app. Those wallets are self-custodial: the customer holds the keys, rather than an IOU on MoneyGram's books.

"Over the past year, we rebuilt the core of MoneyGram so that a digital dollar could move through it as naturally as cash moves through our agent network," Luke Tuttle, MoneyGram's chief product and technology officer, said in the announcement. "Everything else is invisible by design."

What a Dollar Balance Changes for Remittance Users

Josh Gordon-Blake, executive vice president and general manager of MoneyGram Online, described the use cases in a June 4 interview. The conversation was conducted by the Stellar Development Foundation and shared with The Defiant.

The first is refunds. "Now with a stablecoin balance, we can return that money instantly so they can repair that transaction and resend it right away," he said.

The second is a balance on the receiving side, something cash recipients have never had. "Now, for the first time, the receiving customer that's receiving in cash can say, 'I want to keep half of my remittance in USD,' and only take out a portion of their transaction."

The third is the cash network itself. "500,000 locations is more than Walmart, 7-Eleven, Subway, McDonald's combined," Gordon-Blake said, "everything from Walmart in the US, to the bodega in Mexico City, to the smallest of partners in Nigeria." That footprint already serves crypto wallets and exchanges whose users top up with cash: "We work with a number of wallets that are using us essentially like a global ATM."

Gordon-Blake placed the project inside MoneyGram's regulatory posture rather than its crypto ambitions. "We're a regulated financial institution. We have over 75 different licenses. We have 200 regulatory bodies that we work with. We've been working with them and talking to them about the pros and cons of stablecoins for over five years now," he said. The design question, as he framed it: "We're not trying to catch up. We're trying to build a remittance platform. If a remittance platform were being built today, what would it look like? You would build on a global ledger that allows you total interoperability to every country in the world."

The bet is operational rather than speculative. "If Bitcoin goes to zero tomorrow, it doesn't matter to us at all, because we're looking at the ability to efficiently move money globally, and that's what stablecoins unlock for us," he said.

Stellar's Path From Cash Ramps to Native Issuance

MGUSD extends a partnership that began in October 2021, when MoneyGram connected its agent network to Stellar so consumers could convert Circle's USDC to cash and back. The service went global in 2022 and now operates as MoneyGram Ramps. "Our five-year partnership with MoneyGram is proof that stablecoins have moved well beyond pilots," Denelle Dixon, CEO and executive director of the Stellar Development Foundation, said in the announcement.

The launch came a week after DTCC, the clearinghouse that settles most U.S. securities trades, said it plans to connect its tokenization service to Stellar in the first half of 2027. The two deals put institutional issuance and consumer distribution on the same chain.

The network has drawn other regulated issuance this year, including the first regulated yield-bearing stablecoin and Amundi's tokenized swap fund.

Freeze Powers, Issuer Dependence, and an Unproven Market

The architecture carries tradeoffs. The GENIUS Act requires issuers to retain the capability to seize, freeze, or burn payment stablecoins when legally ordered. A customer who controls their keys still holds a token Bridge can freeze at the contract level.

The system also depends on a single issuer for minting and redemption, the same dependence USDC and USDT holders carry with Circle and Tether.

And the demand is unproven. MGUSD launched in the U.S. only, while the strongest use cases sit in the $685 billion remittance corridors outside it. MoneyGram has not published a rollout timeline.

MGUSD puts a federally regulated, self-custodial dollar balance in front of 60 million customers. Behind it sits a cash network that can move value between paper and chain in either direction. The number to watch is MGUSD's circulating supply once the rollout leaves the U.S.

Advertisement

Get an edge in Crypto with our free daily newsletter

Know what matters in Crypto and Web3 with The Defiant Daily newsletter, Mon to Fri

90k+ Defiers informed every day. Unsubscribe anytime.