Contrasting The 2022 Market Crash To 2018’s Crypto Winter

The crypto industry faces one of the most critical periods in its young history.

Bitcoin has lost 55% since reaching an all-time high of $69,000 in November 2021. Just a few weeks ago, the collapse of Terra, the second-largest DeFi ecosystem, left behind the most significant loss of wealth in modern history. Retail, institutional, and even corporate investors lost over $60 billion in LUNA and UST as the 7th and 10th largest tokens by market cap evaporated in a matter of days.

To make matters more complex, the correlation between crypto and stock markets reached an all-time high in 2022, the worst year for capital markets since WWII. The war in Ukraine, the highest inflation in 40 years, and current monetary policies are just a few of the headwinds favoring a bearish trend for the last six months.

The uneasiness of looking directly at another crypto winter is palpable. However, the industry has undergone an accelerated evolution since 2018, when the last winter lasted around 18 months, leaving hundreds of projects born during the ICO era frozen in our memories.

This report compares the 2018 crypto winter with the current six-month bear trend in an attempt to assess whether a crypto winter is ahead, and what the crypto industry can expect in the upcoming months.

The ICO era and First Crypto Winter

In 2017, the crypto space was undergoing its first notable expansion phase fueled by the ICO boom that culminated with the first major bull run in December of that year. Numerous existing startups and new projects took advantage of the novel concept of leveraging cryptocurrencies as a funding mechanism.

There was optimism around a continued economic recovery from the macro perspective, with some scars still visible from the Great Recession of 2008. Epic’s Fortnite generated $8.5 billion in yearly revenue, while Apple became the most valuable brand. Tech and digital stocks were thriving.

The euphoria around crypto startups attracted a record amount of capital into the space, most of it coming from unleveraged retail investors. Multiple companies changed their names to include the word blockchain or crypto, while some businesses even decided to pivot their entire operation to catch the trend—something eerily reminiscent of the dot-com bubble.

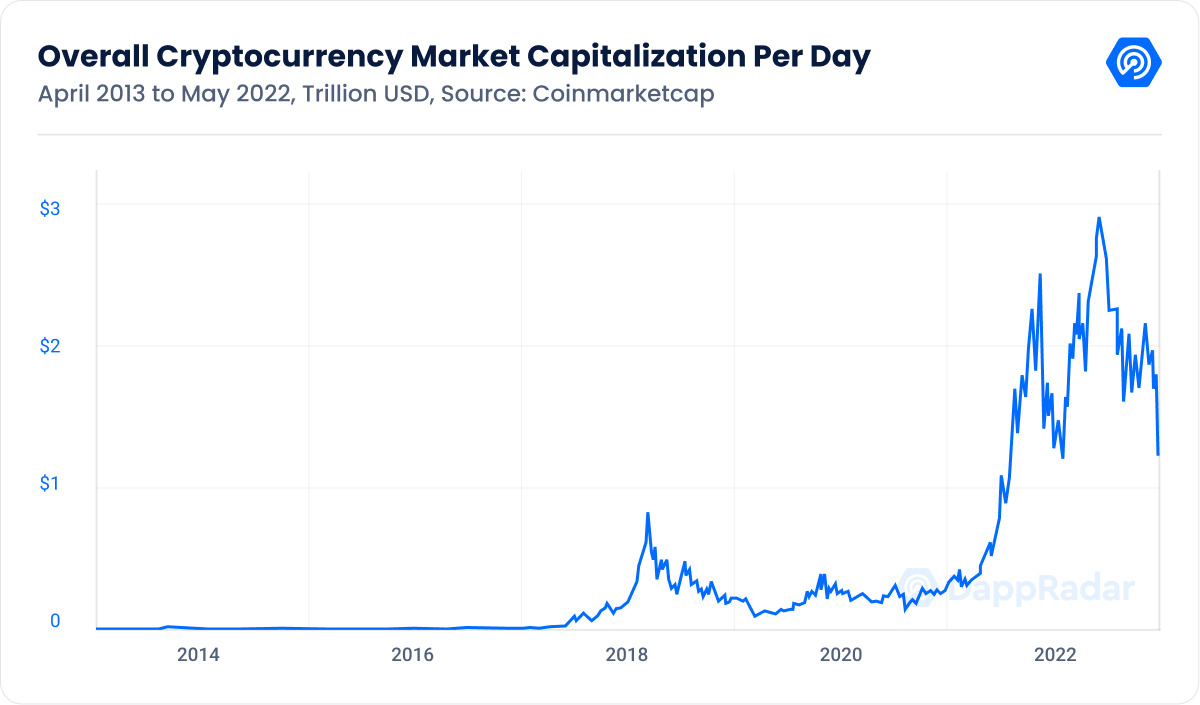

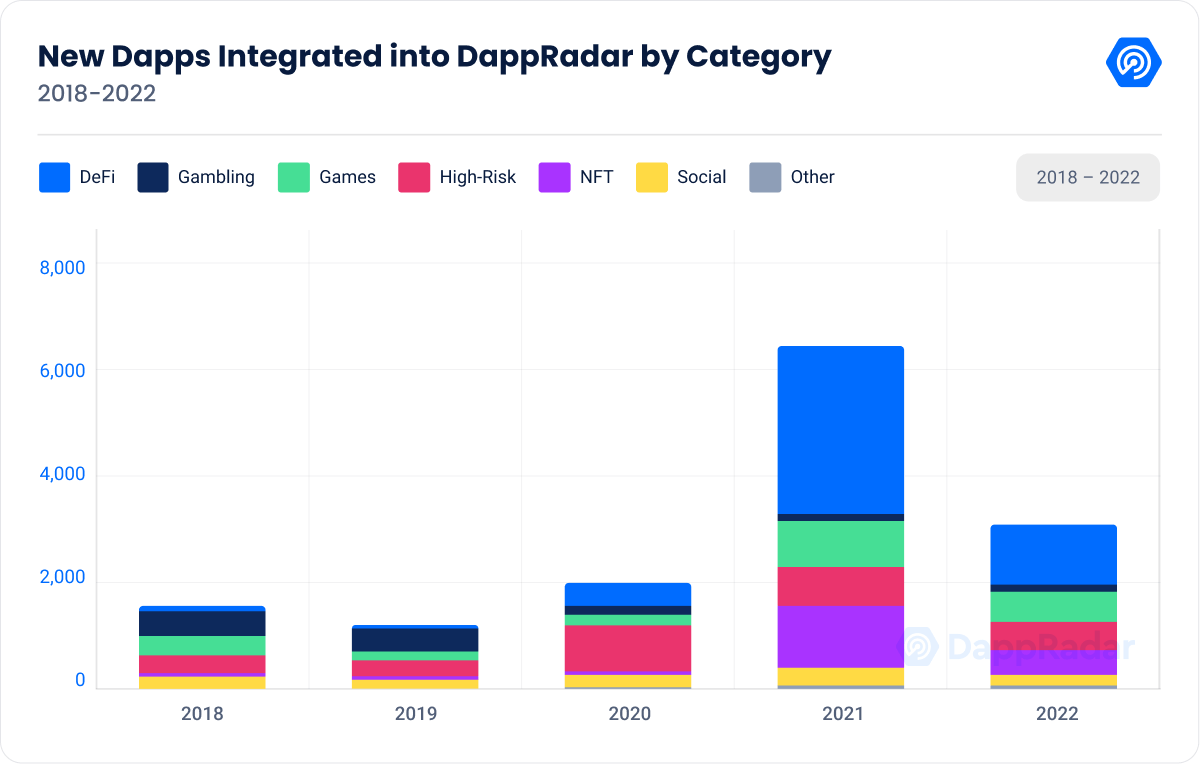

However, the blockchain industry was less adopted and even more unregulated than it is today. Only 104 dapps were live and running by the end of 2017, when total cryptocurrency market cap surpassed $800 billion for the first time in history at the peak of the bull run. Cryptocurrencies like BCH, MIOTA, DASH, and XMR accompanied BTC, ETH, LTC, and XRP in the top 10 tokens by market cap.

The lack of regulations and the excessive capital thrown at underachieving projects quickly turned the nascent industry unsustainable. It is estimated that 90% of the projects conceived during the ICO era failed less than six months after launch. Still, projects that became mainstays of today’s industry, such as Decentraland, and Enjin, were born thanks to ICOs.

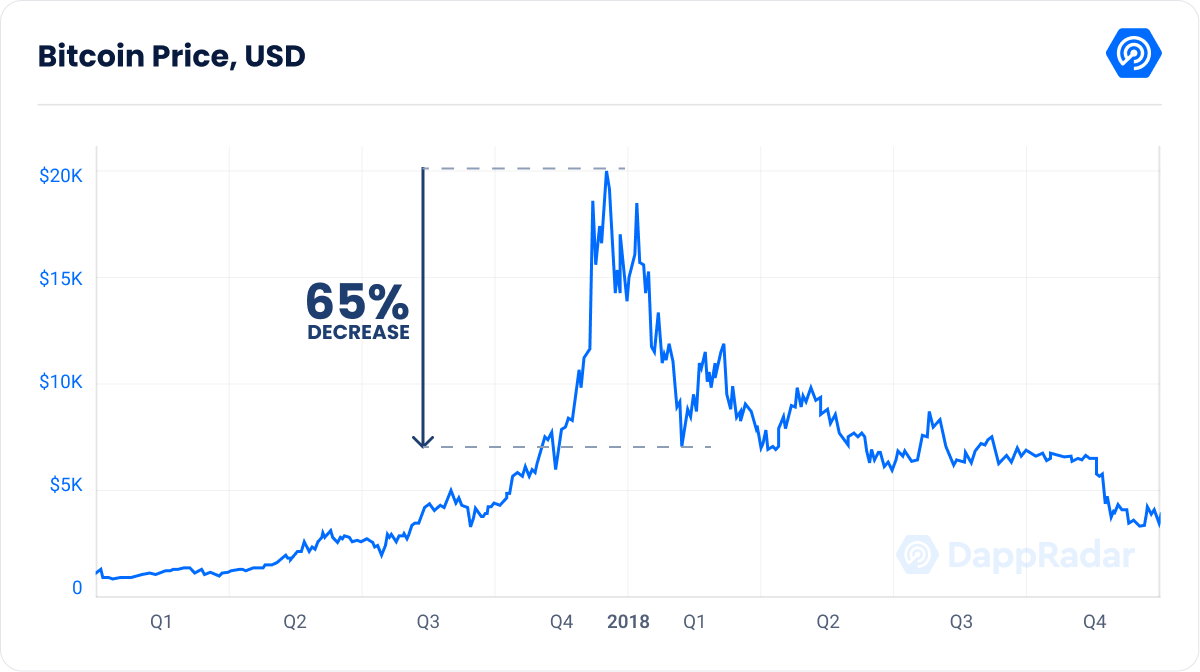

Multiple scams and failed projects created a sense of uncertainty around the industry. And after the price of BTC saw a new all-time high, reaching almost $20,000 in December 2017, a series of events put enough pressure on the industry to turn the biggest bull-run ever seen into the start of a grueling crypto winter.

In parallel to BTC’s all-time high, the first Bitcoin-based futures were launched on the CME, the world’s largest derivatives exchange. Institutional investors shorted Bitcoin en masse, applying unprecedented selling pressure to the digital asset.

Moreover, during the following months, rumors that South Korea, China, and other Asian nations could ban crypto trading, along with the Coincheck hack in which $530 million was lost, resulting in the halt of the Japanese OTC exchange, lured the bears back into the market.

As a result, the price of Bitcoin collapsed to $7,700, losing 65% of its value from the ATH reached in December 2017. The amount of capital lost by overleveraged retail investors and the uncertainty of an unstable market with imminent regulations gave rise to a cruel and prolonged winter that froze most of the still-nascent ICO industry.

The crypto winter of 2018 was an extended period of low prices that lasted almost 18 months. Besides the flat figures, this cycle was characterized by little to no levels of interest and engagement. Investor interest returned in July 2019, when the price of BTC surpassed the $10,000 mark, starting a recovery period that was derailed shortly thereafter when the COVID liquidity crunch crashed the markets in March 2020.

The 2018 crypto winter was precipitated by a series of factors inherent to the industry itself. Uncertainty from the high failure ratio from the ICO era, the overleveraged individual investor profile, and doubts about imminent regulations created the perfect landscape for a crypto winter. Will history repeat itself four years later?

Crypto Winter: No Hibernation, Time to Build

Before comparing the current market situation with 2018, it is necessary to understand how the blockchain industry got to its current state. The previous crypto winter became a critical period for the burgeoning dapp ecosystem. The foundations of the industry as we know it today were laid during this period.

The projects leading the blockchain space kept committed to building and enhancing their products despite the downward trend. Networks like Ethereum, EOS, and Bitcoin’s Lightning, achieved important milestones, while Web3 projects including Axie Infinity, ETHLend (now known as Aave), and even DappRadar, were successfully launched in a period when interest in the space was scarce.

After 18 months of continuous struggles, the crypto industry started to show signs of improvement. There was revived interest in the space and prices began to soar back. However, another setback halted the crypto recovery as COVID affected almost every industry.

In March 2020, the global markets collapsed amid the massive disruption to the supply chains and the intensive lockdowns worldwide. The price of BTC collapsed by almost 50% in one day, while the S&P 500 lost 23% in two weeks. The fear of another winter was real.

Despite the complex situation, several verticals took advantage of the accelerated digitalization we experienced as a society. The price of tech stocks like Amazon, Netflix, Zoom, and Peloton soared. Similarly, the dapp industry began to take shape as leading projects revealed their enhanced products after two years of building.

DeFi summer in 2020 saw a plethora of projects showcasing the potential of a decentralized financial ecosystem. Curve, MakerDAO, Uniswap, PancakeSwap, and a handful of other DeFi players paved the way for a multi-billion space barely learning to farm tokens named after food. The narrative in the dapp industry had changed completely.

Meanwhile, Biden and Powell’s expansive monetary policy printed 80% of all the USD ever issued in history in just two years. The amount of capital injected into the economy to incentivize spending saw retail and institutional investors turning their attention to the crypto market.

By October 10, 2020, the price of BTC had surged 120% from the COVID bottom, surpassing $12,000 for the first time since early 2018. The interest in the blockchain industry was back. Adoption, consumer confidence, and capital invested all rose, fueling the start of the next bull run. In just six months, the price of BTC rose 134%.

DeFi, NFTs and Games Fuel the 2021 Bull Run

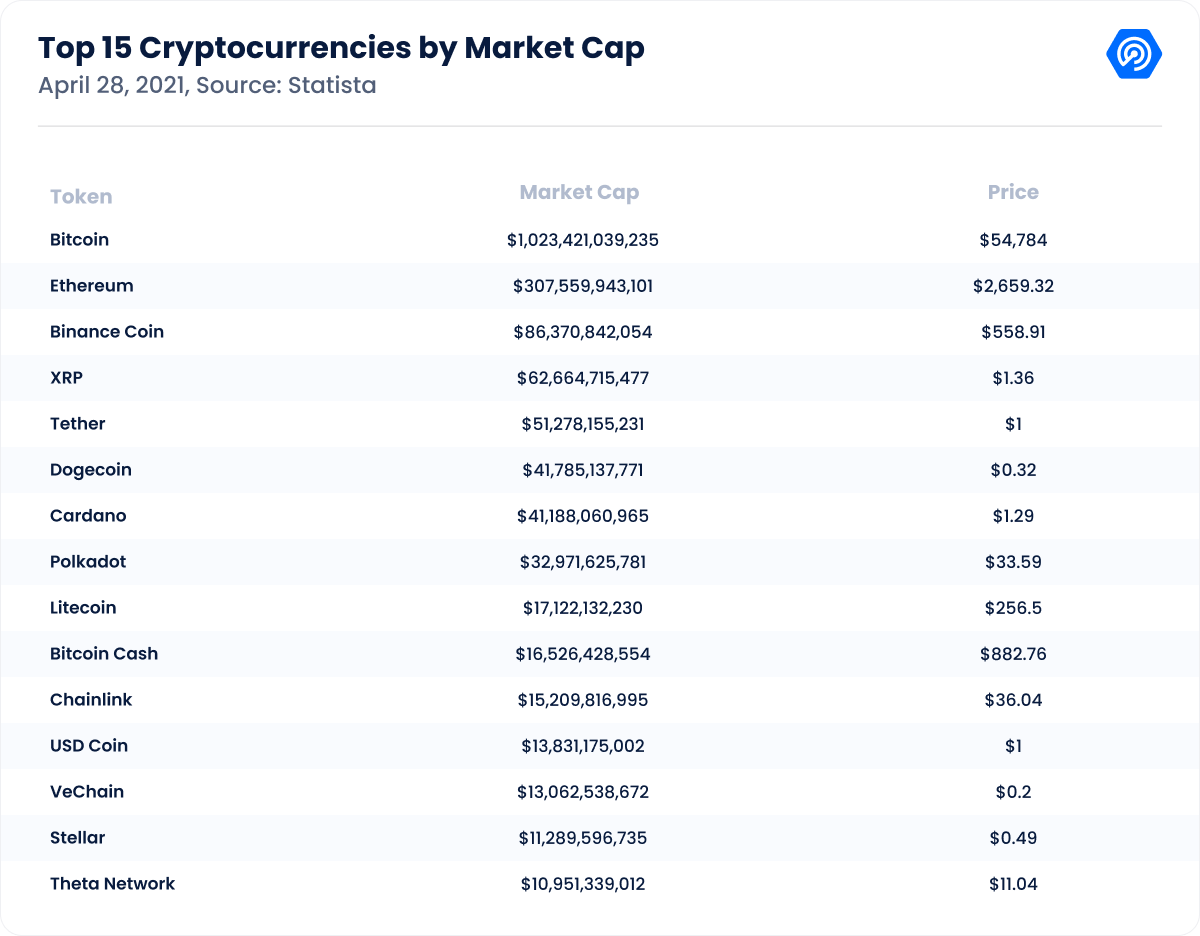

By 2021, crypto winter was a distant memory. The bull run sent BTC surging past $60,000 and the cryptocurrency market cap broke $2 trillion for the first time ever in April of that year. BTC and ETH were solidified as the top two cryptocurrencies with BNB, USDT, DOT, ADA, UNI, and LINK showing the new face of the industry.

At this point, the dapp industry began harvesting the seeds planted during the winter two years ago. The industry’s three main categories – DeFi, NFTs, and games, showed exponential growth through most of 2021, luring millions of new users and billions in investments. Web3 paradigms such as multichain interoperability and play-to-earn were on full display.

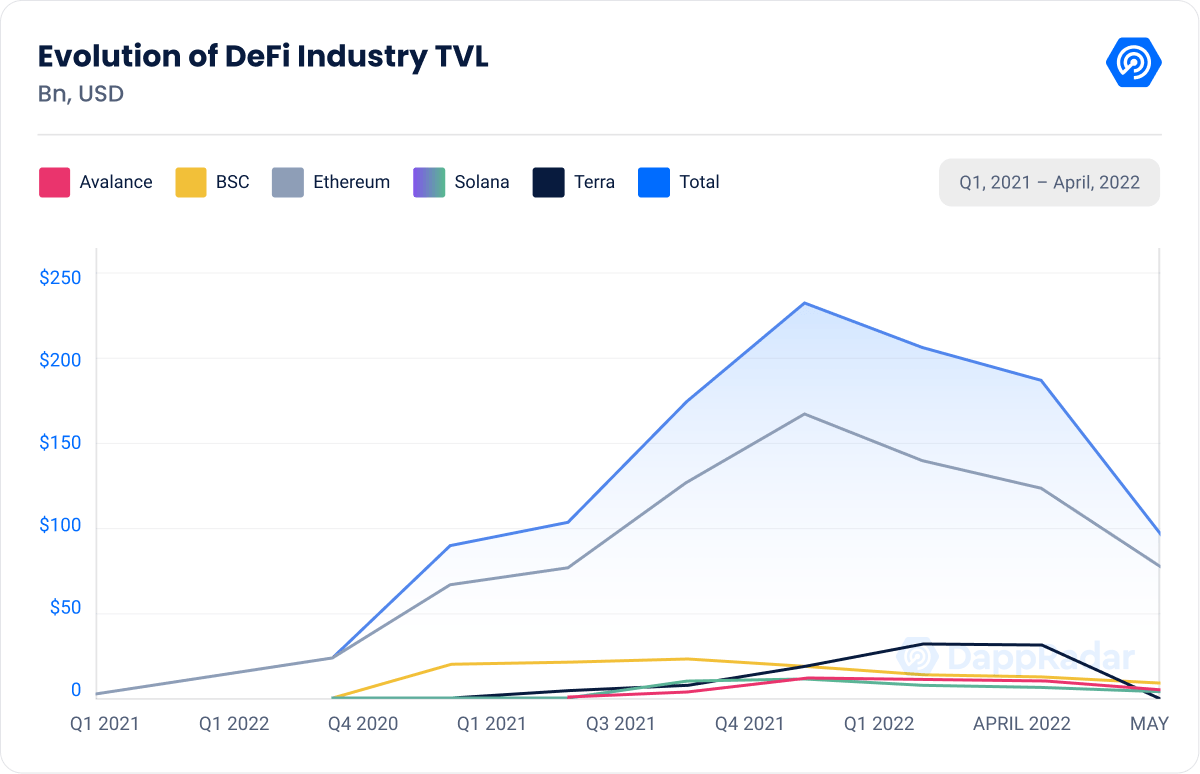

For instance, the DeFi space saw the value locked within its smart contracts surpassing $200B across all protocols in November of last year. The multichain paradigm helped blockchains like Polygon and Avalanche become hosts of DeFi ecosystems with billions in value locked.

NFTs also exploded as the space generated over $22 billion in trading volume last year. At the same time, the top 100 most valuable Ethereum collections were estimated to have a $16.7 billion market cap. NFT artists like Beeple, Pak, and Fewocious took NFTs to the mainstream stage. Collections like CryptoPunks and BAYC became a cultural phenomenon with the power of attracting celebrities and brands into the space. With NFTs enabling ownership and authentication, the potential of this blockchain use case was revealed.

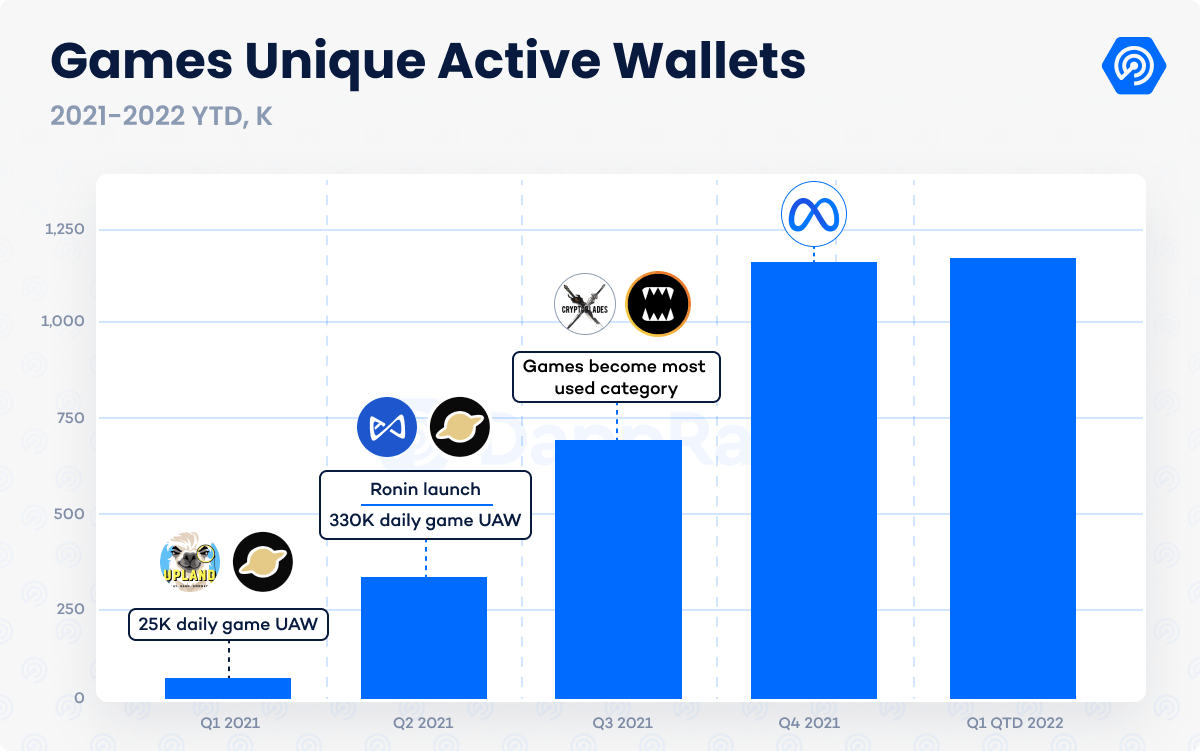

Similar to NFTs, blockchain-based games grew exponentially during 2021. Game dapps like Axie Infinity, Upland, and Alien Worlds compensate their players with cryptocurrencies and NFTs, creating new income streams. The popularity of this type of game, especially in emerging economies, gave birth to the play-to-earn concept.

As the industry appeared ready to capitalize on its recent expansion, Facebook’s rebrand created a new hype cycle around the metaverse narrative. Metaverse related cryptocurrencies and NFTs experienced visible growth in demand resulting in considerable value appraisal. In Q4 2021, metaverse dapps generated more than $330 million in NFT sales from more than 50,000 unique traders. VCs and other investors poured record capital on blockchain-based metaverse and game projects.

In November of last year, the blockchain industry reached its current ceiling. BTC reached $69,000, growing 360% in one year. Ethereum and the majority of the crypto market also peaked in the same month. The cryptocurrency market cap surpassed $2.8 trillion after Meta’s announcement. There was a feeling of optimism across the entire industry.

Complex Macro Scenario

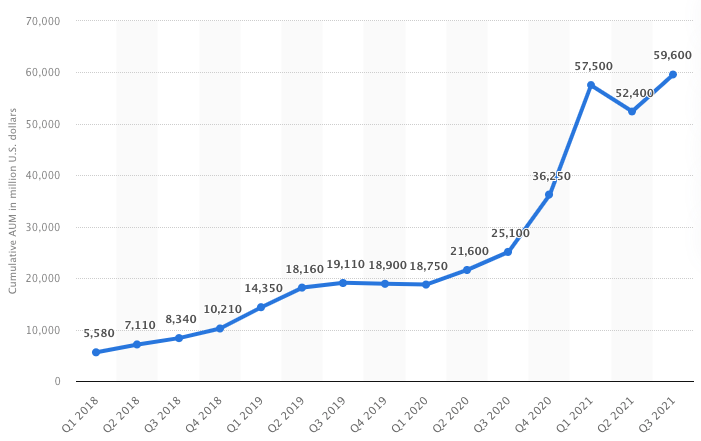

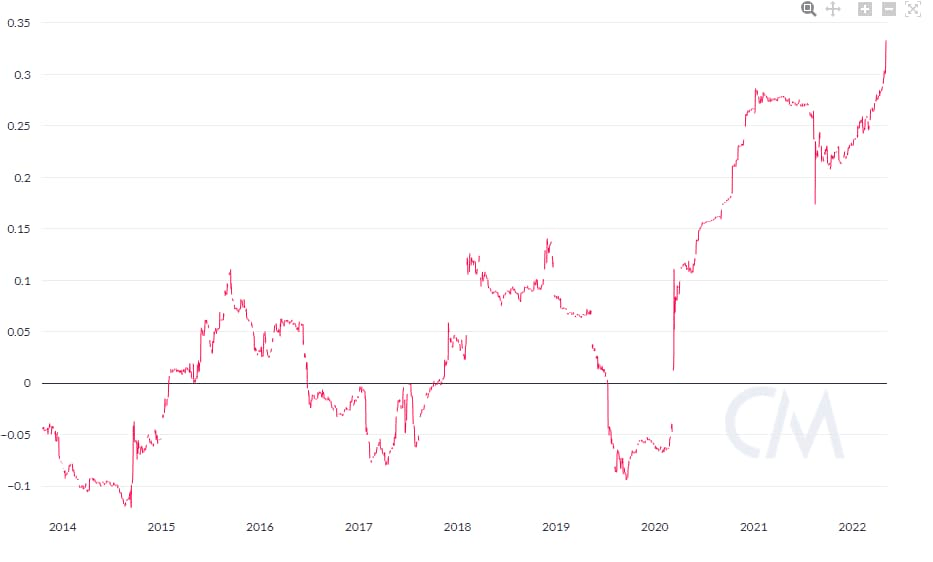

Run the clock forward to 2022 and the dapp industry is in a much better position than four years ago. Hundreds of dapps attract over 2.5 million daily Active Wallets across more than 50 blockchain ecosystems. The investor profile is entirely different as well. Institutional and corporate investors now dominate the crypto landscape. The amount of cumulative crypto assets under management (AUM) is nearing $60 billion as the popularity of crypto derivatives has grown as well. At the same time, VCs and private investors have poured over $30 billion into blockchain projects, with one-third going to games and virtual world projects to help them build the foundations of the Web3 metaverse.

Cumulative crypto funds assets under management; Source: Statista

From a macro perspective, the situation is different than in 2018 though. The negative effects accentuated by the war in Ukraine present a severe challenge to global markets. In addition, the early-year suspicions about the Fed’s imminent interest rate hikes to counter rising inflation were confirmed a few weeks ago when the FED raised interest rates by 0.5% for the first time in two years.

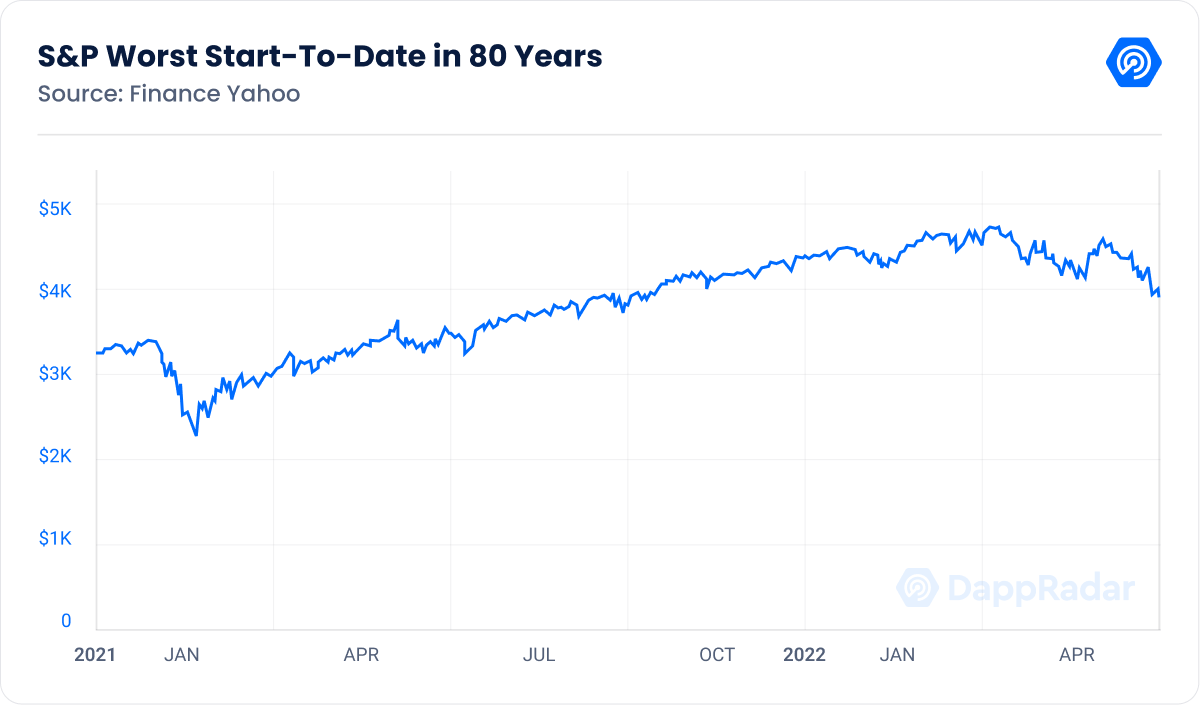

Moreover, the aftermath of the staggering money printing streak is already taking a toll. The S&P 500 is off to its worst start since WWII, and inflation has reached levels not seen in almost 50 years. The sum of these macroeconomic factors is leading the markets into what looks like a recession.

The macroeconomic situation hindered the bull trend which was fueled by the metaverse hype cycle. Despite the impressive evolution that the dapp industry observed over the last four years, Bitcoin has lost 55% of its value since its all-time high in November. The Terra situation put even more pressure on a crypto market that is about to experience a macroeconomic recession for the first time.

Is Winter Coming?

There are noticeable differences when comparing the series of factors that caused a crypto winter in 2018 and what we are seeing right now. Firstly, the blockchain industry has gone from a small group of siloed networks to a series of interconnected ecosystems attracting millions of daily users. The three main categories – DeFi, NFTs, and games flourished into multi-billion dollar verticals.

In the same way, the investor profile went from mostly retail investors to large institutions and corporations with more economic power. The awareness for the space is higher than ever, with crypto sponsorships seen in almost every major sport and billboards advertising Web3 products in multiple cities across the globe. Bitcoin has been adopted as legal tender and might act as a hedge for countries facing hyperinflation like Venezuela, Argentina, and others.

The same can be said for NFTs. This type of digital asset is decoupling from the stock and crypto markets, proving to be one of the most resilient assets in recent history. Similar to art, which historically has been one of the most resistant investment vehicles.

The rise of Web3 brands building at the forefront of the metaverse shows organic growth from within the space. Web3 brands like Yuga Labs, The Sandbox, and RTFKT have partnered with numerous retail giants, including Adidas, Nike, HSBC, Warner Bros, etc. We are witnessing an exodus of talent from leading Web2 projects into the blockchain world.

As significant as the blockchain industry has become, challenges remain. The collapse of Terra brought the sector down to its knees. Except for DAI and a few other tokens, many stablecoins, including Tether, struggled to maintain their peg during the high volatility period. The trust levels in algorithmic stablecoins and the space, in general, could discourage smart money from entering the weakened DeFi space. Security and regulations are other topics that require special attention as soon as possible.

In addition to these challenges inherent to the blockchain, the record high correlation between stock and crypto markets presents another burden. As mentioned before, capital markets have had their worst start to a year since the 1940s. The prices of high-flying tech stocks like Netflix, Facebook, Roku, Wix, and Robinhood, have fallen sharply with some exceptions. And as a recession seems more probable by the day, the short-term outlook for the capital markets does not look promising.

Historical correlation between BTC and S&P 500; source: Finbold

Winter Is Here

So after assessing the current situation and contrasting it with 2018’s, a crypto winter is probably upon us despite the impressive maturity of the dapp industry and the accelerated expansion of the Web3 community.

The macroeconomic situation, coupled with the Terra collapse, might be too much for the crypto market already facing a pullback phase from the Meta bull run. However, due to the level of adoption, the interest in the industry shouldn’t decrease as much as in 2018.

Bitcoin, NFTs, and other cryptos should continue to be demanded as a new class of digital assets with unique economic properties. Also, corporate and government adoption will force lawmakers to work on policies to regulate digital assets bringing headlines to the mainstream media.

Furthermore, it is necessary to consider that the crypto market is composed of cycles. It is unsustainable for any industry to maintain constant growth. Consolidation and capitulation cycles are healthy to create financial stability within the markets. After the Meta hype cycle, a pullback was expected. However, the war in Ukraine triggered a financial crisis at a time when stocks are more correlated to crypto than ever before.

Quoting Elon Musk, “Recessions are not necessarily a bad thing. I’ve been through a few of them. And what tends to happen is if you have a boom that goes on too long, you get a misallocation of capital. It starts raining money on fools.” Something similar applies to the crypto winter, a period that should be viewed as an opportunity to depurate the market. Successful projects will continue building during harsh times, while empty projects will fall flat.

For newcomers, a crypto winter might feel like the bubble has burst, but the truth is it is not. The blockchain industry has already experienced crypto winters in the past but has been resilient. Although the space is about to undergo its first recession, the maturity showcased across multiple verticals has the crypto space in a good position to resist a prolonged bear market.

The main question now becomes, how long until spring arrives?

Advertisement

Get an edge in Crypto with our free daily newsletter

Know what matters in Crypto and Web3 with The Defiant Daily newsletter, Mon to Fri

90k+ Defiers informed every day. Unsubscribe anytime.