DeFi10 Returned 370% Thanks to ETH and Airdrops

TLDR: At the start of the year, I invested $1,100 in 10 DeFi applications, plus MakerDAO’s Dai Savings rate as a benchmark. The requirement was that they could give me passive income; I would just send 100 Dai into their smart contracts, never touch it again, and then hopefully have more than 100 Dai at the end of the year, whether it be through interest, fees, or automated trading strategies.

[Read: DeFi10 Part 1: Lessons in Building a DeFi Portfolio, DeFi10 Part2: Becoming a Programmable Money Fund Manager]

Fast forward to Dec. 31, and I had just over $5,200 in my wallet.

DeFi10 portfolio as of Jan. 3. Image source: Zerion

At the start of 2020, DeFi was very different. The budding financial system’s favorite metric, Total Value Locked, was at $680M on DeFi Pulse, compared with $15B today. The closely-tracked dashboard listed only 21 projects, while the list has swelled to 56 now. There was no yield farming, no governance token or food coin boom, and some of the space’s most popular protocols today, like Yearn Finance and Curve, weren’t even live.

But even then, as it’s true now, anyone with an Ethereum wallet and an internet connection was able to access these financial applications to do from complicated things, like leveraged trading and arbitrage, to simply open a dollar-based savings account. And it was this latter use case that interested me the most: how (1) easy, (2) safe and (3) profitable is it to just set and forget a chunk of savings in DeFi?

Let’s go one by one.

1. Easy: Very —But it Takes Getting Used To

It took me about two hours and change, or ~15 minutes per dapp, with about three to four steps involved in each one, to complete the entire experiment. This is pretty wild. Think about it: First, I transferred 1,100 Dai from one wallet to the DeFi10 wallet, and that took seconds. Next, I was able to distribute that digital cash among 11 different financial applications in about the time it took me to watch Home Alone 2 on Christmas Eve. Imagine the headache doing that would have been in traditional finance or even in CeFi; creating accounts on each app, connecting bank accounts, waiting for IDs to get validated —in DeFi, each app automatically connects to your wallet, and you’re ready to go.

And what about the cost? The bunch of transactions to do all of this came to a grand total of just $3.43 (!!) Which is making me nostalgic for pre-yield farming times when gas was that cheap. We’ll find out how much the cost has risen when I repeat the experiment this year. [For newcomers: Users of Ethereum DeFi applications have to pay the network to process transactions a fee that’s priced in “gas” and paid in ETH.]

Of course, the hurdle is buying ETH most likely in a centralized exchange, getting that ETH into a decentralized wallet, and then getting used to having to approve and pay for transactions in each step —it’s all pretty weird if you’re not used to it. And not just that, but it’s an entire paradigm change realizing that your “user” is your wallet, and that you control, and are responsible for, the tokens inside.

2. Safe: Not Yet

If there’s one thing we’ve learned this year is that decentralized finance has a long way to go before it’s safe for users. There was $154M lost in hacks and attacks in 2020, according to Coingeek. These attacks were largely of a different nature than what we’re used to seeing in centralized finance; rather than a hacker actually stealing funds kept in a centralized vault, they find ways to exploit loopholes in the code to manipulate prices in such a way that they ultimately buy and sell mispriced tokens. But there is also old fashioned stealing, and what’s worse is that it’s the dapp founders themselves who sometimes run off with the money —what’s known as a “rug pull.”

None of the applications I tested did a rug pull, but one of them was hacked multiple times. I had deposited 100 Dai in bZx’s lending platform and gotten the iDai interest-bearing token in return. Now, after the project was hacked twice in February and once more in September, the iDai token is inactive and there is now a v2 of the token. To be clear, I didn’t lose any funds and can withdraw the Dai I deposited plus the interest I made by going to the legacy bZx site.

I said it at the start of the experiment, and it’s worth saying again because I don’t think much has improved in this regard: DeFi needs more disclaimers. Users need to know precisely the risks they’re taking on, and it’s not enough to say “this project is in beta use at your own risk.” DeFi builders: You can do better.

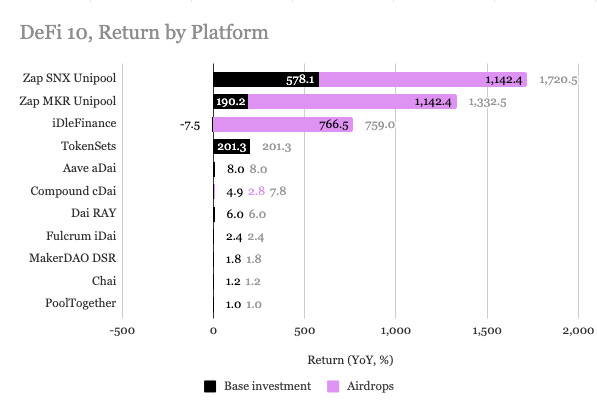

3. Profitable: DeFi10 Outperformed Everything But Holding ETH

The DeFi10 wallet was holding $5,233.67 on Dec. 31, that’s a 376% increase from $1,100 at the start of the year. But there’s an important precision to make: much of that return was thanks to token rewards, or “airdrops,” from three of the protocols I used: Compound Finance, Uniswap, and IdleFinance.

After frowning upon tokens after the ICO craze, DeFi fully embraced them again last year, and every protocol, from new ones pieced together over a weekend, to those which had been tokenless for years, started issuing their own native digital asset to reward previous users and attract new ones.

It literally paid to be a DeFi user in 2020.

Without the token airdrops, the DeFi10 portfolio would have returned almost 90%, which is still pretty good, beating most (if not all) major asset classes outside of crypto.

The DeFi10 portfolio had four categories:

- Interest-bearing tokens (aDai, cDai, iDai, Chai)

- Yield aggregators / bouncers (IdleFinance, RAY)

- ETH-exposed investments

- Liquidity pools (MKR-ETH and SNX -ETH on Uniswap, via Zapper)

- Automated Investment strategies (ETH20DMA on TokenSets)

- Out of the box (PoolTogether)

ETH-Exposed

The best performers were ETH-exposed investments because ETH ended up soaring by more than 400% this year. Funds deposited in Uniswap liquidity pools at least doubled, and swelled by 30x to ~$3,000 when accounting for the UNI tokens I got thanks to providing liquidity (I split the ~$2,284 in UNI between the two Uniswap pools in my results).

Of course, this wasn’t the case in March when Ethereum’s cryptocurrency plunged —at the time, Uniswap liquidity pools were the only DeFi10 investments in the red.

TokenSets’s automated trading strategies —I picked one that buys and sells ETH following its 20-day moving average— is the second-best performer after Uniswap liquidity pools. It had the advantage of maintaining gains all throughout the year, even when ETH plunged.

Interest-Bearing Tokens

Returns on interest-bearing tokens were a bit underwhelming at just 3.7% on average, not counting the COMP airdrop. [For newcomers: In DeFi, there are a multitude of tokens that represent deposits in lending platforms, so that the amount invested plus the interest earned are reflected in the actual price of the token].

That may be better than 0.01% US banks give on deposits, but savers would be taking on considerable risk by putting funds in a smart contract, which can be exploited, hacked or which the founding team may have access to. I’m not sure ~4% is enough to compensate for the risk. To be fair, the rate is variable and it’s now at ~8% for Dai deposits on Aave.

Yield Bouncers

Yield bouncers are meant to automatically move users’ deposits to the lending platform with the best rate. The most popular yield bouncer today is Yearn Finance, but the project didn’t exist when I started the experiment. I went with RAY and IdleFinance, which surprisingly, underperformed lending Dai directly on Aave or Compound. In the case of IdleFinance, I wasn’t able to find the interest I made on my initial deposit on the platform. I was prompted to migrate to v2, but the transaction was more than $40 in gas on Jan. 1. I reached out to the team late last night about it and will update once I hear back or figure it out.

No-Loss Lottery

Finally, the “out of the box” project. PoolTogether is a no-loss lottery where users deposit cryptocurrency in exchange for lottery tickets, and the platform directs those deposits into lending platforms. The winner gets the interest earned, while the ticket holders are able to withdraw the crypto they deposited. With weekly prizes at ~$3,000, this could have been the top performer. Alas, it wasn’t my luck.

Most investments outperformed the benchmark, MakerDAO’s Dai Savings Rate.

Trackers

Another point to make: When I started the experiment one of my complaints was that it was hard to track my investments. I’ll mention that has greatly improved. The main tool I used was Zerion, as I appreciate the chart outlining the overall performance of the portfolio over time. I also found it reflected most of the investments I made, though RAY was missing. Zapper and DeBank also offer great portfolio tracking tools.

All in all, DeFi10 was a success. It made $5,000 from $1,100 thanks to DeFi — and I didn’t even do one bit of yield farming! Which projects should I test for this year’s experiment?

Appendix:

Advertisement

Get an edge in Crypto with our free daily newsletter

Know what matters in Crypto and Web3 with The Defiant Daily newsletter, Mon to Fri

90k+ Defiers informed every day. Unsubscribe anytime.