What Is Silo Finance?

Sponsored![What Is Silo Finance? [Sponsored]](/_next/image?url=https%3A%2F%2Fcdn.thedefiant.io%2Fa233fc6609da6356012236afddc0c6ab07287410-600x338.jpg&w=1920&q=100)

As a self-custodial lending protocol, Silo Finance represents the next evolutionary step in decentralized finance (DeFi). Although DeFi already offers dozens of lending platforms, Silo pushes the envelope by isolating the risk posed by specific tokens.

To understand what makes Silo Finance the second-generation lending protocol, compared to the likes of Aave and Compound, we must first grasp the dangers DeFi users are exposed to.

DeFi Benefits and Risks

Riding on the wave of Bitcoin as “sound money,” DeFi expanded the use of smart contracts to recreate the cornerstone of banking in blockchain form — borrowing and lending.

What was previously the purview of bank tellers, was supplanted by smart contracts, accessed through self-custodial wallets. This effectively eliminated the need for credit history scores, checks, and intermediaries. In DeFi, one only needs a funded wallet to deposit a collateral for a loan, leaving everything else to smart contract automation.

Nevertheless, DeFi is not all sunshine and rainbows. There are three probable risks users could be exposed to.

1. Oracle Manipulation

As third-party blockchain networks, such as Chainlink, these oracles feed information about the value of real-world assets back to smart contracts. Consequently, if that feed is intercepted and manipulated, the exploiter could inflate the value of a loan’s collateral.

One of the first such oracle exploits happened in 2019 where the price of sUSD stablecoin was manipulated on the Synthetix exchange. This caused the oracle to report an inflated price for sUSD, which allowed the exploiter to buy and sell sUSD at inflated prices, taking the profits and draining the protocol’s liquidity.

Cream Finance and Venus also suffered similar oracle manipulation, to name a few. These smaller protocols often use sub-standard code to facilitate price feedback. In the case of Cream Finance, the flash loan attacker exploited a poorly implemented oracle price proxy, as the protocol’s own custom oracle.

2. Failure To Liquidate

DeFi or no DeFi, there are always bad loans. Inevitably, this means that bad debt has to be liquidated at some point. But if the DeFi platform fails to liquidate the debt promptly, it can lead to a catastrophic cascade affecting all the protocol’s depositors (liquidity providers).

Even the largest lending protocol, Aave, came very close to being unable to liquidate large amounts of Curve DAO (CRV) tokens as bad debt, after the notorious crypto miscreant Avraham Eisenberg short-squeezed $1.6M worth of CRV.

Failure to liquidate could also happen without external manipulation. In 2020, DAI on the MakerDAO platform plummeted following the price drop in its underlying asset, ETH. This created a scenario in which the value of the collateral backing DAI was insufficient to cover the total amount of the stablecoin in circulation.

In turn, MakerDAO had to quickly intervene to update the protocol to ensure that the collateral value was sufficient to cover the value of Dai stablecoin.

3. Token Exploits

Outside tampering with the price feeds, one could also tamper with the token’s smart contract itself. This happened with xSUSHI, serving as a collateral token on Aave. The token’s poor code allowed it to be exploited in such a way as to mint an unlimited amount xSushis, and then leave with the borrowed funds.

Aave’s team had to go to extraordinary measures to borrow funds to update the protocol and disable xSUSHI-based borrowing before the vulnerability was materialized. In another example, Harvest Finance was exploited when the attacker manipulated the price of USDT stablecoin on a decentralized exchange (DEX), which he used to trade in other tokens and then leave with millions worth of cryptos.

Keeping these three main DeFi risks in mind, how does Silo Finance mitigate them?

Silo Finance Isolates Token Exploit Risks

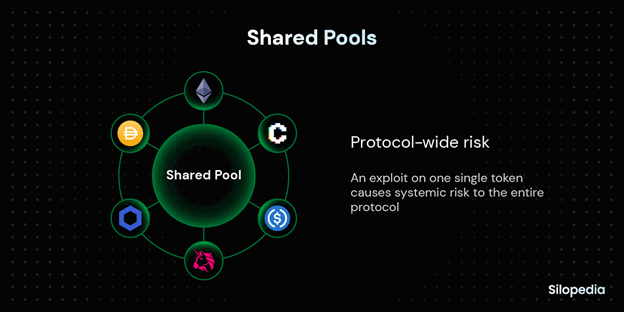

When DeFi users go to the biggest lending platforms, such as Aave or Compound, they are often not aware that these platforms operate by sharing liquidity pools for multiple token assets. This creates a market environment in which a single token exploit creates a domino effect, endangering the entire liquidity pool.

You have already noticed how Aave/Compound deal to cut-short such risk. They meticulously whitelist tokens that are eligible to be used as collateral, leaving borrowers with a limited offering of tokens.

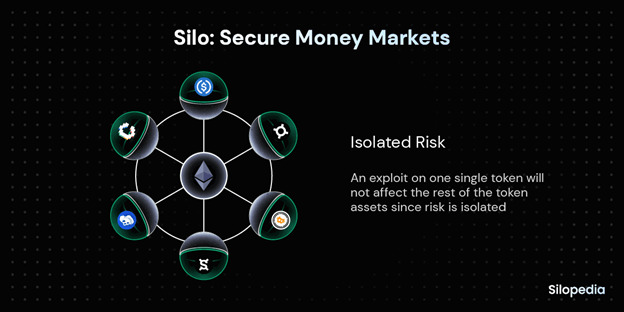

Silo Finance employs a different approach, a Siloed one. Instead of pooling token collaterals into a single pond, Silo isolates each token into its own lending market. Specifically, each token is paired against ETH, as the bridge asset, and against Silo’s own over-collateralized stablecoin called XAI.

So, Silo Finance users are only exposed to the risk of ETH and XAI. In addition to isolating the risk, pairing tokens against ETH/XAI has the benefit of creating a deeper protocol’s liquidity instead of a fractured one.

How Does the Silo System Work?

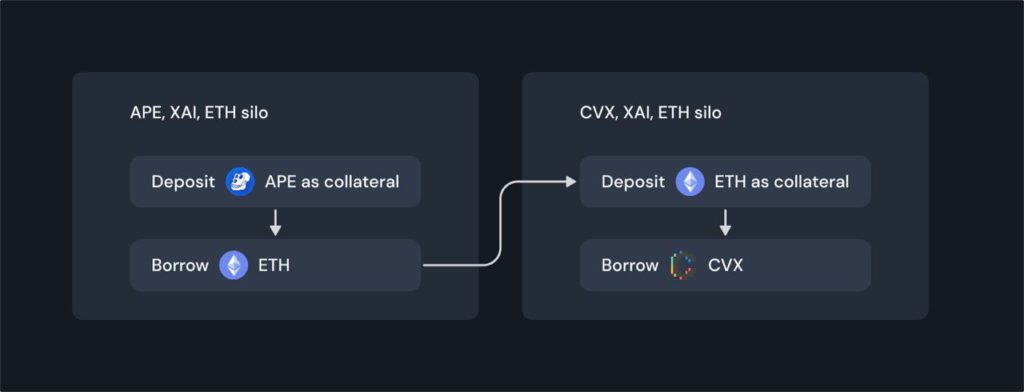

Let’s say you want to borrow token B against your token A collateral. To do so, you would move the bridge asset (ETH) between the tokens’ Silo pools. While ETH is the first bridge asset, the XAI stablecoin is the second one.

Accordingly, token A would not pose a collateral risk, but the bridge asset itself — ETH. With the bridge asset mechanic, each Silo pool has instant access to the protocol’s entire liquidity. Simultaneously, all tokens serving as collateral are isolated within their own Silo pools.

Unlike Aave, this allows Silo Finance to employ any token as a collateral, removing the need for white-listing.

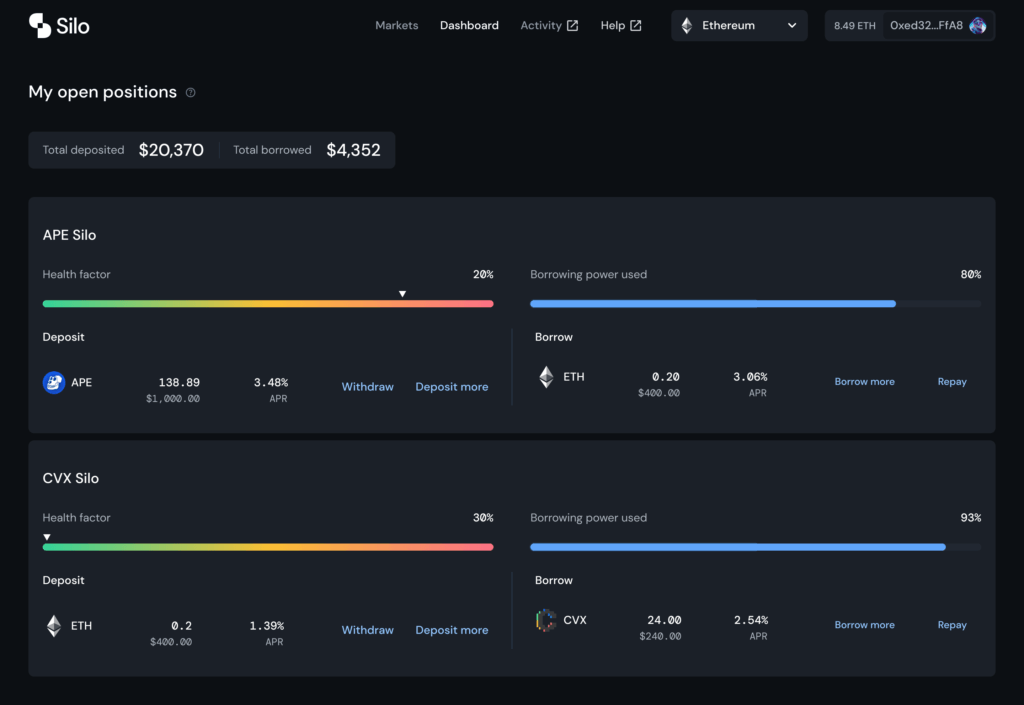

In practice, this means that you borrow ETH or XAI stablecoin by depositing any token in your wallet supported by the underlying network — Ethereum or Arbitrum. The borrowed ETH or XAI can then be deposited in either single or multiple Silos.

If you had used ApeCoin (APE) as a deposit to borrow ETH, you would have utilized the APE Silo. Likewise, if you had deposited ETH to borrow CVX, you would have utilized the CVX Silo.

Whatever your Silo position is, the APE and CVX Silos are isolated, so if either tokens are exploited, both borrowers and lenders remain safe. As explained in previous token exploit examples, other lending platforms lack such safety because their tokens share a single liquidity pool.

XAI’s Soft Peg and Rewards System

No doubt, the collapse of Terra, owing to its depegged stablecoin UST, forever tainted the concept of decentralized stablecoins. So, what makes Silo’s XAI stablecoin different?

Firstly, XAI doesn’t rely on the dynamic contraction/expansion of another cryptocurrency like LUNA within its own ecosystem. Instead, XAI is an over-collateralized stablecoin using external assets — either ETH or other stablecoins — DAI, USDC, FRAX, LUSD, and others.

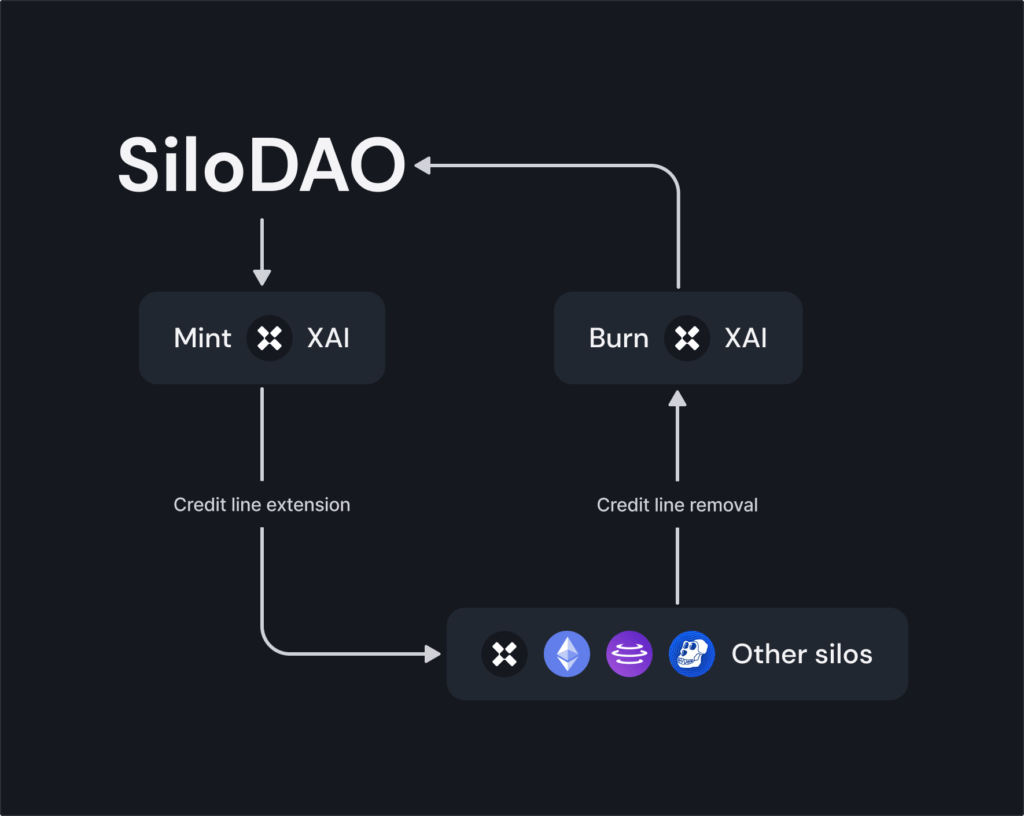

In the crypto world, this makes XAI a soft-pegged stablecoin, as opposed to hard-pegged USDC, which relies on holding USD cash/treasuries reserves in a traditional bank. Nonetheless, XAI’s soft peg robustness is automated by SiloDAO.

As a decentralized autonomous organization, the SiloDAO either contracts or expands XAI liquidity into any token Silo. The conditions of minting XAI, as the second asset bridge into Silos, depends on the type of the deposit, with ETH as the only one incurring fixed interest rate.

This is to ensure that more established, large market cap assets like ETH provide stability for XAI credit lines. Typically, USDC is the most commonly used XAI borrowing collateral, owing to its highly regulated reserves by Coinbase and Circle.

So, XAI’s soft peg to USD is wedged between users’ credit extension (which tokens can be used as XAI minting collateral) against users’ credit retraction (removing XAI out of Silos). SiloDAO’s smart contracts have access to the totality of the funds circulating in token Silos, so it maintains XAI soft peg by either increasing or decreasing interest rates.

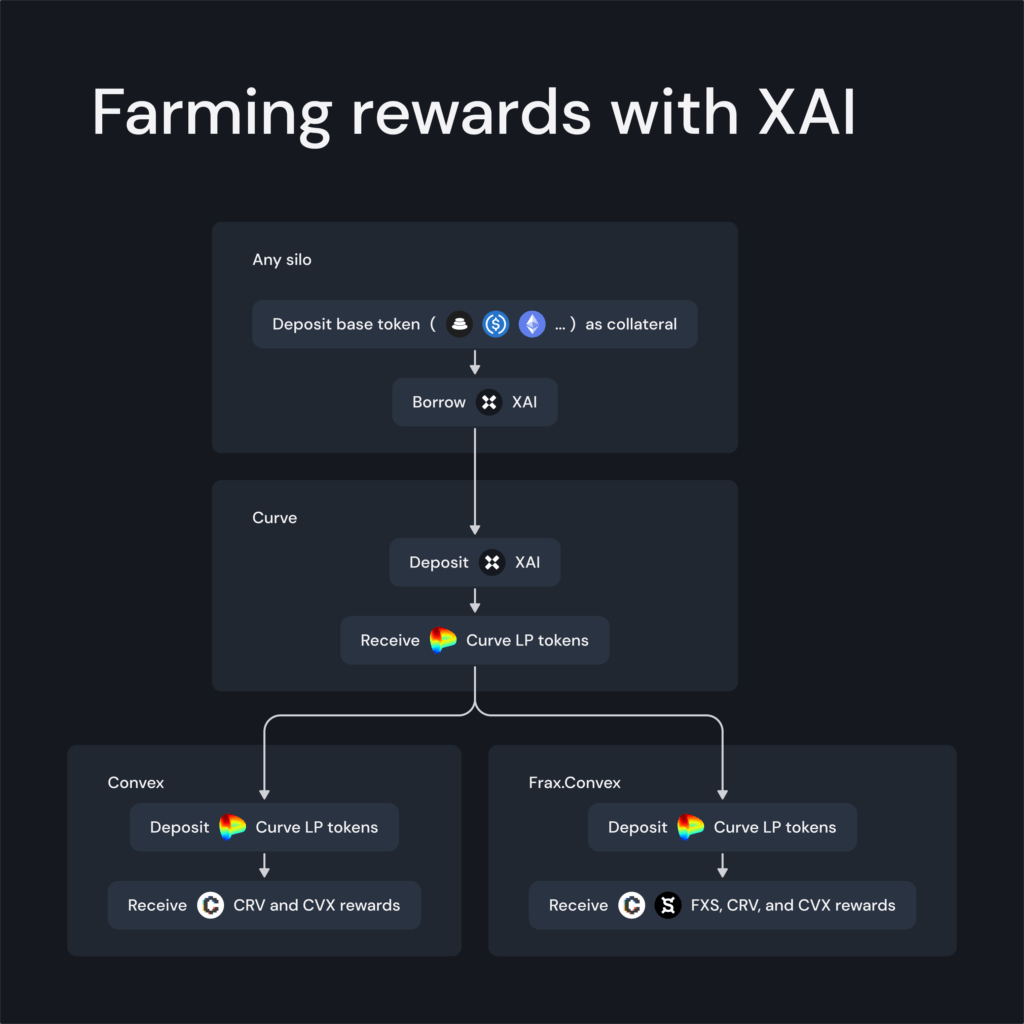

In the case of borrowing XAI for ETH deposit, the fixed interest rate would be 0.1%, while other Silos would impose more dynamic interest rates to maintain the peg. Of course, the interest earned against the borrowed XAI stablecoin goes to SiloDAO treasury, allowing users to farm rewards in several different combinations.

This is also where DeFi’s liquidity staking comes into play on Silo Finance.

Liquidity Staking Incentivized by SILO Tokens

Liquidity staking has become exceedingly popular and is poised to grow even further. What’s not to like?

You use a platform to stake your ETH to secure Ethereum’s Proof of Stake network. But instead of having those ETH locked on the network, unavailable for use in dApps, the staking platform would issue the equivalent of the staked ETH.

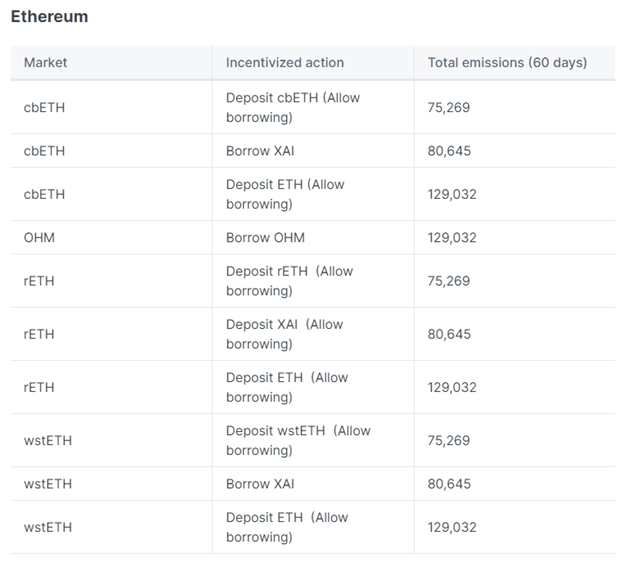

In the case of Coinbase, it would issue Coinbase Wrapped Staked ETH (cbETH). You could then deposit cbETH on Silo Finance, presently offering a 4.64% annual percentage rate (APR). You would also receive an additional incentive in the form of SILO rewards.

SiloDAO holds 1.73M SILO tokens, with the simple goal to incentivize borrowing and lending, having launched on March 13, 2023, and lasting 60 days. Within the Ethereum ecosystem, people are eligible to receive SILO tokens with these actions:

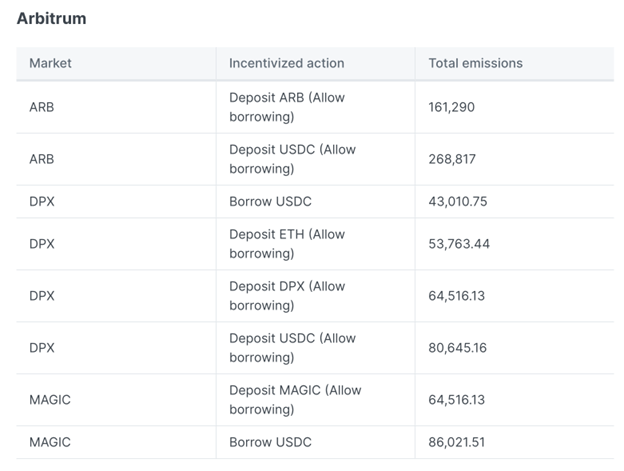

Updated number to reflect incentives added yesterday to the ARB market.

On Arbitrum, the ecosystem is dominated by Dopex (DPX) decentralized options exchange, alongside MAGIC (MAGIC), a decentralized marketplace for blockchain gaming.

Year-to-date (March 2023), SILO price performance is +58%, ranging between $0.03 and $0.07 per SILO. All SILO rewards are earned passively, without staking, so one only needs to claim them on the Silo Finance dashboard.

In the second half of 2023, the Silo Finance team plans to launch veSILO tokens, which will provide liquidity to Balancer and Aura on Ethereum, and to Sushi on Arbitrum. Of course, users will receive generous APR for this service.

Yield + Risk Mitigation = Silo Finance

With so many examples of token price manipulation, it is likely that Silo Finance is starting a new trend of deposited tokens having their own, Siloed lending markets. Without sacrificing safety through shared-pool lending protocols, Silo Finance provides SILO incentives and XAI leverage to maximize returns.

In turn, Silo Finance is mainstreaming liquid staking derivatives (LSD) markets. With a combination of Siloed liquidity pools and automated market makers (AMMs), LSD markets are crafted to minimize the difference between the expected price of a trade and the actual price at which the trade is executed.

The same principle applies to lending and borrowing as well, entirely reliant on the integrity of the provided collateral. By isolating tokens into their own Silos, the platform bolsters such integrity.

Note: This explainer was sponsored by Silo Finance

Series Disclaimer:

This series article is intended for general guidance and information purposes only for beginners participating in cryptocurrencies and DeFi. The contents of this article are not to be construed as legal, business, investment, or tax advice. You should consult with your advisors for all legal, business, investment, and tax implications and advice. The Defiant is not responsible for any lost funds. Please use your best judgment and practice due diligence before interacting with smart contracts.

Advertisement

Get an edge in Crypto with our free daily newsletter

Know what matters in Crypto and Web3 with The Defiant Daily newsletter, Mon to Fri

90k+ Defiers informed every day. Unsubscribe anytime.