Uniswap LPs Prove to be Fickle as UNI Holders Stick Around

Markets Update by Lucas Outumuro IntoTheBlock. On-Chain Impact of the End of UNI Mining

Uniswap’s UNI release had major effects on the DeFi space. Just hours after the UNI airdrop, Ethereum hourly fees and gas costs reached a yearly high. Similarly, UNI’s liquidity mining program led Uniswap to become the DeFi protocol with the highest TVL, increasing its liquidity supplied by 4x to a high of over $3 billion.

Since UNI’s liquidity mining ended on November 16, Uniswap’s liquidity dropped by over 50% in a matter of days. At the time of writing, Uniswap has $1.32 billion in liquidity supplied, which is still 76% higher than the liquidity locked on September 16 prior to the announcement of UNI’s yield farming. However, the $1.7 billion+ that left Uniswap as soon as the rewards stopped point to the unloyal yield-seeking behavior incentivized by yield farming.

While the migration of liquidity may not come as a surprise to many readers, Uniswap’s liquidity mining program also showcases other interesting patterns. By analyzing on-chain data provided by IntoTheBlock, we are able to better understand the implications of UNI’s liquidity mining on Uniswap and the broader DeFi space.

Here are three key insights of UNI’s liquidity mining and general lessons learned:

1. Uniswap Liquidity Shifts to Competing DEXes

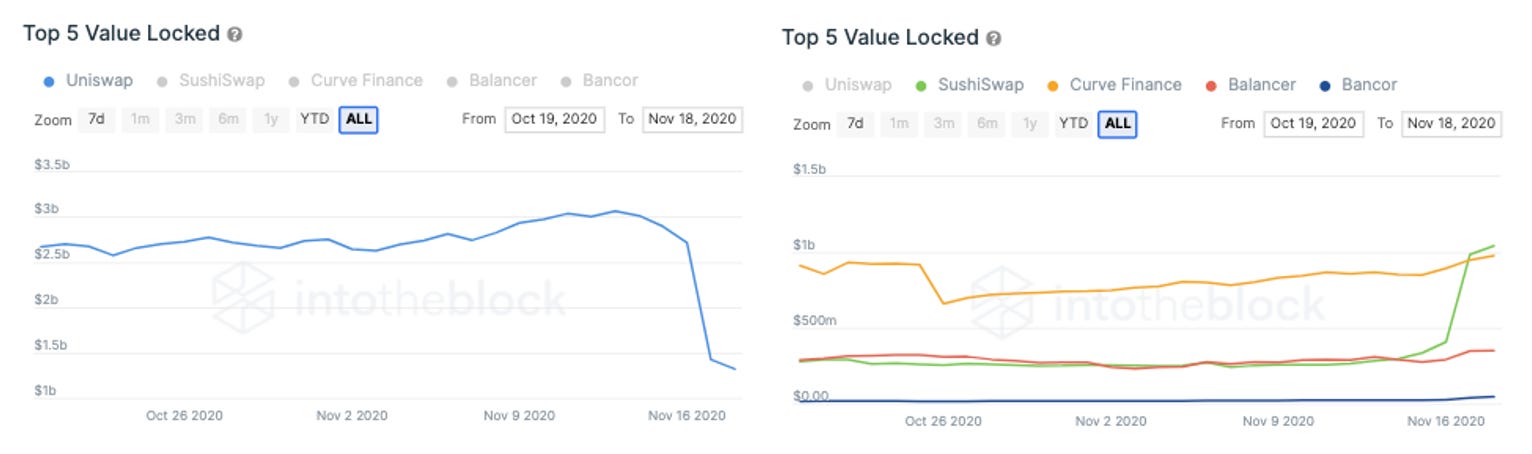

The main benefactors of Uniswap’s liquidity mining expiring were other decentralized exchanges. In terms of TVL, it is clear that LPs quickly migrated in search of high rewards. This is observed in the contrast between the liquidity supplied to Uniswap and its competitors as soon as UNI rewards ceased.

Source: IntoTheBlock’s DEXes Insights

In particular, SushiSwap has gained the most in terms of liquidity as can be seen in the graph in the right. Month over month, SushiSwap has seen an increase of 257% in liquidity supplied, while Bancor, Balancer and Curve grew by 193%, 17% and 6%, respectively. This demonstrates that liquidity providers (LPs) favored direct Uniswap AMM competitors with 50-50 pools over DEXes with slightly different models or scopes such as Balancer and Curve.

2. Uniswap Continues to Dominate in Volume, Proving it’s Stickier

While Uniswap continues to have higher liquidity overall than SushiSwap, the latter has dethroned the former with the most liquid trading pair out of all DEXes. At the time of writing, the USDC-ETH pair in Sushiswap has the highest liquidity. Note that the charts below do not consider liquidity mining rewards for the values shown for return on liquidity (ROL).

Source: IntoTheBlock’s DEXes Insights

The chart above also shows that while LPs quickly reallocate capital based on expected yields, traders do not switch as easily. The most traded pairs across DEXes were still in Uniswap, even for the less liquid USDC-ETH pair and ETH-USDT pairs. In aggregate, Uniswap traded a total of $419 million on November 17, which is five times greater than the $73 million settled by Sushiswap.

While in theory higher liquidity benefits traders protecting them from slippage, traders still opted to trade at Uniswap. It is unclear if these traders effectively incurred higher costs by trading these pairs in Uniswap instead of in SushiSwap. Although the higher volumes persist in the meantime, it is also uncertain whether traders will eventually migrate as well, or if they will be more loyal to Uniswap than their liquidity provider counterparts.

3. Money Flows into UNI as Holders Continue to Grow

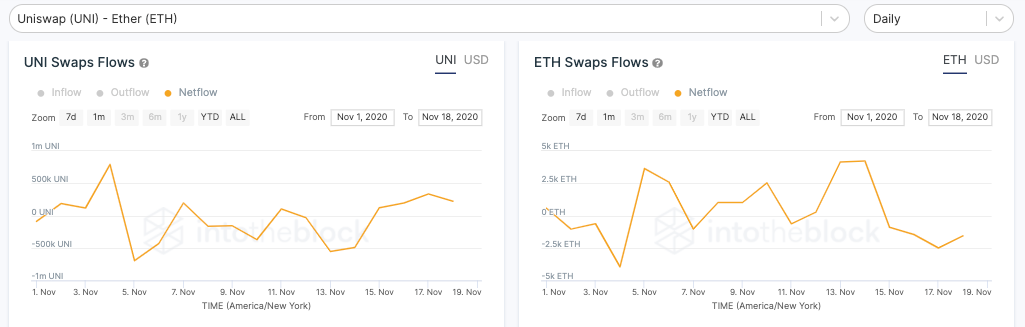

Some have pointed to a potential sell-off in UNI to occur as liquidity providers claim their rewards upon the ending of liquidity mining rewards. UNI prices have indeed dropped approximately 10% since these ended, but have done so in the midst of a broader sell-off in crypto. By analyzing Uniswap flows data, we observe that swaps in the UNI-ETH pair have actually been more inclined towards UNI in November.

Source: IntoTheBlock’s Free Uniswap Protocol Metrics

Uniswap Pair flows show whether the liquidity taken from traders is from swapping UNI for ETH or vice versa. If there is a greater inflow than outflow into a token, then its net flow would result positive. Throughout November, the UNI-ETH pair has seen negative net flows for UNI of -816k UNI, meaning that is the net amount withdrawn from traders swapping ETH for UNI so far this month.

Similarly, in centralized exchanges UNI has left more exchanges than entered them in November. The net flow for UNI to centralized exchanges has also been negative, pointing to 715k more UNI leaving centralized exchanges than entering them throughout the month. This is generally seen as an indication of positions being taken and traders opting to hold their own tokens.

Source: IntoTheBlock’s Uniswap UNI Analytics

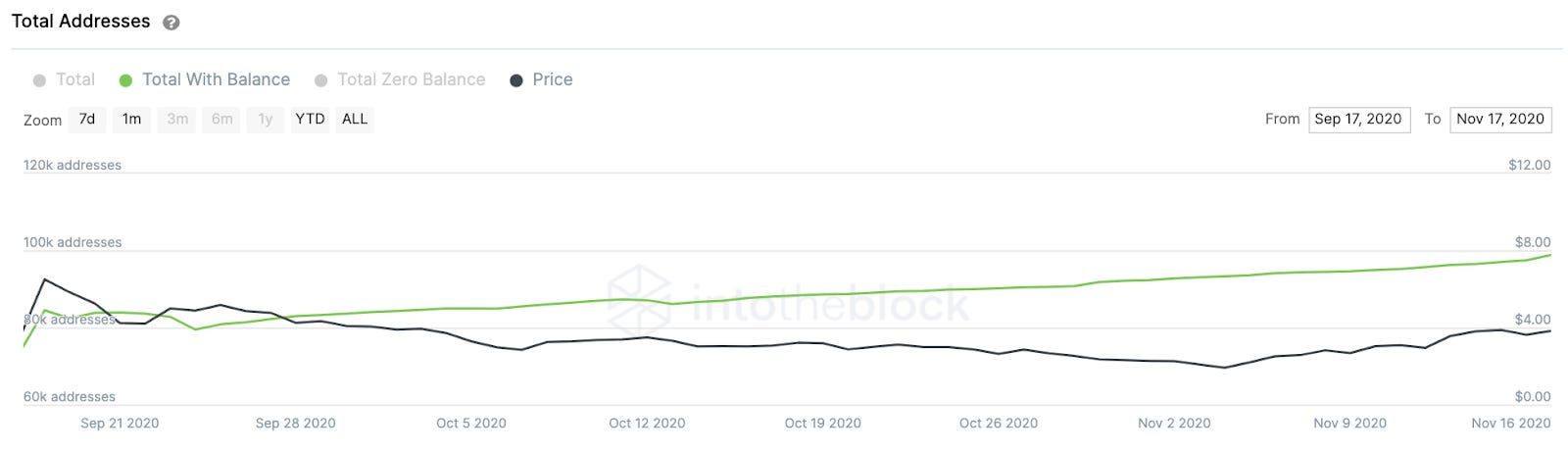

This trend suggests that both CEX and DEX traders continue to trade into UNI in spite of its liquidity mining rewards coming to an end (at least for now). This pattern is echoed in the total number of addresses holding the UNI token. The total number of addresses holding UNI has been increasing steadily since late September, approaching 100k holders.

Source: IntoTheBlock’s Uniswap UNI Analytics

Overall, the end of UNI’s liquidity mining has had strong effects on Uniswap and the broader DeFi space. It proved the fickle nature of liquidity providers and how these rewards may not sustainably improve supply-side metrics by themselves. At the same time, it demonstrated that traders do not switch platforms as easily and continue to acquire UNI despite the 50% decrease in Uniswap’s liquidity. It will be interesting to see how Uniswap adapts future UNI incentives to mitigate short-term-minded LPs and continue to engage traders.

Advertisement

Get an edge in Crypto with our free daily newsletter

Know what matters in Crypto and Web3 with The Defiant Daily newsletter, Mon to Fri

90k+ Defiers informed every day. Unsubscribe anytime.