Uniswap Liquidity Near All-Time High – This Time Without Liquidity Mining

Uniswap liquidity is fast approaching an all-time high and this time the most used decentralized exchange (DEX) isn’t riding the wave of its liquidity mining program.

The automated market maker (AMM) hit a previous high of $3.36B in liquidity during the end of its incentive program when the exchange was awarding liquidity providers (LPs) with UNI, in addition to the .03% rewards granted to the capital pool. Liquidity is now over $3B again.

The spike in liquidity is yet another sign of rising interest and activity in decentralized finance.

Still, some of the increase should be attributed to higher prices. Wrapped ether (WETH), constitutes over one third of the total $3B of the liquidity staked in Uniswap. The exchange’s liquidity is up 44% on the year, but ether’s price is up 63% along with much of the crypto market.

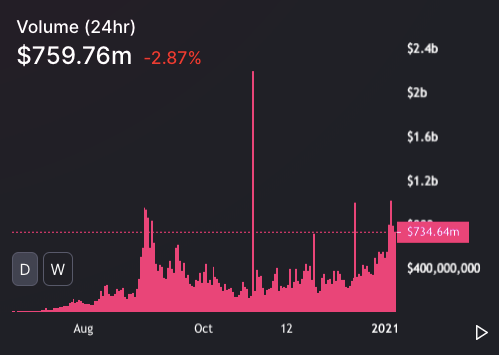

Liquidity isn’t the only metric on the upswing for the DEX. Volume too is up. Though that’s also in part because of the increase in the value of tokens flowing across the DEX’s smart contracts, rather than increased usage.

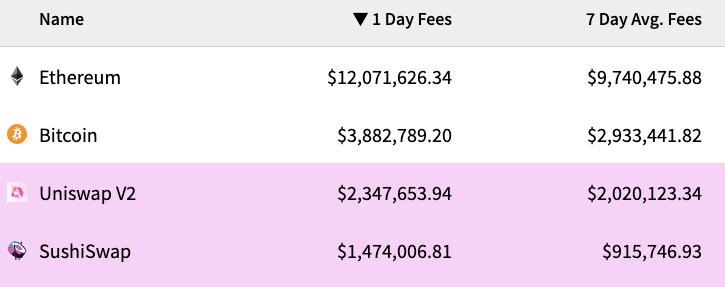

Regardless, the Uniswap team has much to celebrate, as fees paid to use the protocol (which go to LPs) are at two thirds of the level of Bitcoin’s over a seven day average according to Cryptofees.info, which tracks the data. The protocol checks in at number three in the average fee rankings across projects.

Also worth noting is that liquidity provided before the recent jump was at $1.5B, roughly double what it was before the liquidity mining program.

That may be the more bullish, albeit less headline-grabbing, sign that Uniswap is succeeding. The incentive program worked: ether’s price was relatively flat during the UNI liquidity mining period, but the overall liquidity doubled from the start to end of that time, meaning LPs continued to contribute liquidity despite reduced rewards.

With the UNI token’s ascension into the top 25 cryptocurrencies, plus a third iteration of the Uniswap protocol aiming to tackle slippage and capital efficiency issues, things are looking up for the original AMM.

It remains to be seen whether the DEX can start to more meaningfully compete with centralized exchanges.

Advertisement

Get an edge in Crypto with our free daily newsletter

Know what matters in Crypto and Web3 with The Defiant Daily newsletter, Mon to Fri

90k+ Defiers informed every day. Unsubscribe anytime.