The Path Towards an Under-Collateralized DeFi

Hello defiers! I have a treat for you today. Alex Masmejean is extremely active in the Ethereum community. He’s a “DAO fiend”; a founding member of MarketingDAO, and part of MetaCartel and Stake DAO. Recently, he’s been thinking deeply about under-collateralization, the ability to issue loans without requiring borrowers to put up more capital than what’s being lent. So far, DeFi has been dominated with over-collateralization to protect against asset volatility and loan default, in a space with no identity or credit checks.

To Alex, and to many others in the space, for DeFi to continue to grow, it will be key for platforms to be able to issue loans without requiring so much capital up front. In the following post, he outlines what the main ways forward for that to happen are. Read up and join the debate!

The Future of DeFi is Undercollateralized

By Alex Masmejean, Defiant contributor and DAO fiend

The future of decentralized finance is undercollateralized, just like the past.

Out of all growth signals in crypto, the decentralized finance (#DeFi) movement is the most visible one: it has grown to surpass $600M in Total Value Locked, up 6 times from the start of 2018. But its use cases remain centered around ‘speculation on top of speculation’, mainly driven by venture-backed startups such as Compound.

This market consists of either thrill-seeking crypto-natives performing margin trades, or whales willing to lend assets at an attractive return, sometimes hovering above 15% annual interest rate. To enforce repayments of these highly volatile loans, these platforms ‘over-collateralize’ as a safety net.

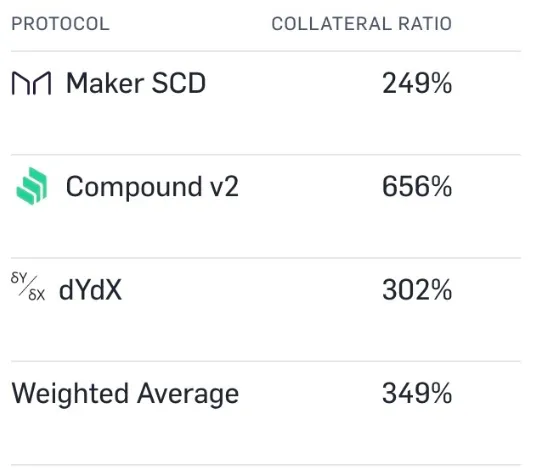

MakerDAO’s DAI has an average of 394% collateralization, meaning that almost three quarters of all ETH is locked for the sake of price stability. The arrival of multi-collateral DAI will potentially imply new, less liquid assets like Synthetix that are set to reach a crazy 750% collateralization ratio. Locking this much value is an extremely inefficient usage of such tokens.

Image Source: Loanscan

While this is fine in our emerging crypto market, it isn’t how most of the financial world operates. It’s logical to assume that most of the world’s populations is not willing nor able to deposit more funds to get a loan than the loan itself: in the U.S. alone, student loan debt was $1.4 trillion in the first quarter of 2019, and that’s just the tip of the iceberg. Crypto needs to rise to that challenge by introducing under-collateralization. But how to financially enforce something that isn’t financially backed?

Option 1: Social Fund Recovery

A first solution would be to shift the financial burden from the borrower to a better suited entity: have someone else guarantee repayments in case of defaulting. Much like smart wallets have ‘social key recovery’, where enough unrelated friends can help one recover access to their wallet, ‘social fund recovery’ relies on trusted parties buying an option covering and splitting the collateral cost.

An example would be: Alice loans $100 via this new service, and convinces 5 of her friends to buy a $20 option to cover the full amount. Since most people are taking out a loan to pay for a good or service in advance, and not betting on a cryptocurrency’s future, the loan itself will be stable, which relieves the volatility problem. But again, logic suggests that we usually are close to people with similar financial situations, and a person needing quick liquidity won’t always have relatives around who can afford to help them.

Option 2: A New Credit Score

A more ambitious way to allow undercollateralization to emerge is to replicate credit scores, allowing to go from friends to a macroeconomic scale. A ‘crypto credit score’ would take into accounts factors such as past salaries from X years, income stability, defaulting precedents and output whether someone has the ability to repay a loan. If the answer is yes, it will then determine an interest rate and the frequency of repayment according to that person’s financial health; the former could be volatile, discovering one’s solvability in real time.

But that opens up a catch-22 around identity: in the crypto world, can’t defaulters just run away? Also, even if you successfully solve the identity layer, the risk is designing a system that allows for censorship beyond lending. In this case, Alice does not repay her $100 loan, blocking her account and seizing as much assets in crypto as possible. She simply logs out and creates a new account with a different address. Her credit score is neutral again.

To avoid this pitfall without revealing one’s identity, a healthier system would be nuanced, separate identities of varying anonymity, as imagined by Balaji Srinivasan in this podcast. The financial identity problem would be to gather the entire financial information of an individual, without accessing any other type of data about that person. Non-financial reputation (e.g. your social identity) would be uncensorable, even though one turns out to be a poor borrower.

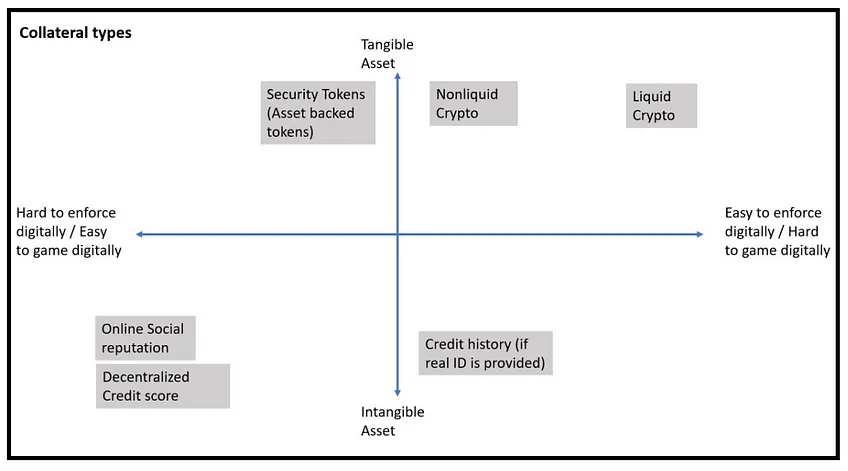

The enforcement problem: collateral types ranked by the tangibility spectrum

Option 3: Zero-Knowledge Proofs

Another solution would be to leverage zero-knowledge proofs, which in layman’s terms means ensuring someone has a convenient crypto credit score without revealing anything about that person, fulfilling the best of both crypto-anarchists and traditional finance. In the future, being asked to go to a club and verify your age shouldn’t disclose your full ID information to the bouncer. Instead, an immutable proof would either claim whether a person is over 21 or not. The same could protect your credit ratings.

One problem is that the data available to objectively assess our crypto credit score is not on Web3. We haven’t produced nearly enough data about the borrower target market to extrapolate from.

We have two choices. One is to make peace with Web2 and try to integrate data from it, even though it was previously described by Vitalik Buterin as ‘semi-decentralized.’ Social media logins for identity, as well as past earnings on platforms such as Airbnb or Uber could satisfy some elements around a person’s creditworthiness. The second is to pull data from traditional finance. Although an obvious choice, it would significantly slow down the process and apply censorship, repeating inaccuracies of a system we so dearly want to replace.

Option 4: Credit Market DAO

This isn’t what innovation is. It is unlikely that blindly replicating previous models will help. As Peter Thiel once said, the next Google will not be a search engine. Here is something new: what if the tight web of trust enabled by the internet — on average, each individual is linked to anyone else on our planet by an average of 3.5 connections — coupled with the wisdom of the crowds, could gauge people’s ability to honor a loan?

Social groups could form coalitions, collectively de-risking loans and share profits from interest rates, ending up stronger together. A DAO-like system could incentivize these groups to behave correctly, proportionally rewarding successful repayments. This system could even create new types of ‘credit checker’ jobs.

Individuals would not be judged solely for themselves, but by the overlap between the different groups they’re part of, maximizing the chance to have a group bet on people. This could stimulate a positive-sum game where lifting someone out of a borrower’s situation could end up reinforcing a group.

Maybe one of these options or a combination of them will prevail, or maybe someone will come up with an entirely different solution. But one thing is clear, undercollaterization is the future of #DeFi and the ecosystem will push to make it happen in the most trustless way.

The Defiant is a daily newsletter focusing on decentralized finance, a new financial system that’s being built on top of open blockchains. The space is evolving at breakneck speed and revolutionizing tech and money. Sign up to learn more and keep up on the latest, most interesting developments. Subscribers get full access, while free signups get only part of the content.

Click here to pay with DAI. There’s a limited amount of OG Memberships at 70 Dai per annual subscription ($100/yr normal price).

About the author: I’m Camila Russo, a financial journalist writing a book on Ethereum with Harper Collins. (Pre-order The Infinite Machine here). I was previously at Bloomberg News in New York, Madrid and Buenos Aires covering markets. I’ve extensively covered crypto and finance, and now I’m diving into DeFi, the intersection of the two.