What's Behind the Converge Delay?

Olivia Capozzalo & Camila Russo

December 02, 2025

gm, Defiers!

Today’s big story:

- Ethena and Securitize have yet to launch their Converge blockchain , which was set for Q2, while Ethena’s USDE supply continues to crater since 10/10

In other news:

- Yearn suffers an exploit

- SushiSwap’s longtime leader steps down

- Strategy reveals USD reserve

Read more below! But first, please give our sponsors some love; they make this newsletter possible.

Filecoin Onchain Cloud is live! Verifiable and programmable storage, fast retrievals, and onchain payments so builders can run real workloads without Big Cloud lock-in. Let's open the cloud: Filecoin.Cloud

Stake MON to earn yield and Magma Points. Magma is the leading native LST protocol on Monad. Start staking today: https://www.magmastaking.xyz/

We’re back! Here’s what you need to know in web3 today

📈 Markets in the Past 24 Hours

| TICKER | VALUE | 24H | |

|---|---|---|---|

| Bitcoin | $91,592 | 7.61 % | |

| Ethereum | $3,020.26 | 9.92 % | |

| XRP | $2.17 | 8.54 % | |

| BNB | $878.17 | 7.80 % | |

| Solana | $139.75 | 12.13 % |

Today’s Big Story

The 10/10 Hangover is Catching up With Ethena

When Terminal Finance said it's shutting down because the Layer 1 that Ethena had announced with great fanfare just months ago has been indefinitely postponed, it raised the question: Is Ethena okay?

Turns out, the high-flying DeFi project isn’t doing so great. Ethena is still feeling the aftershocks of 10/10, the day nearly $20B in leveraged positions vaporized in under 36 hours. For a protocol whose stablecoin, USDe, lives and dies by delta-neutral leverage and perp-funding arbitrage, 10/10 is proving to be an existential stress test.

And here’s why. The entire Ethena system depends on one structural truth in crypto markets: perpetual futures funding rates tend to be positive. When traders are overwhelmingly long, they pay shorts a periodic funding fee and Ethena, on the short side of the trade, harvests that yield to reward sUSDe stakers.

But when 10/10 hit, that long/short imbalance inverted. Liquidations flushed out leveraged long positions across Binance, Bybit, OKX, Hyperliquid and the rest of the perp ecosystem. Open interest collapsed, the long bias disappeared, and funding rates compressed to zero and even went negative. Suddenly, the engine powering USDe’s entire economy had no fuel.

Ethena’s growth is driven by a specific type of user: leveraged traders running basis trades, market makers seeking yield, and funds managing delta-neutral strategies across CEXs. These users don’t care about brand or community. When funding was high, they levered up into USDe. When funding collapsed after 10/10, they exited en masse, unwinding hedges and redeeming USDe to close positions. The post-10/10 environment was a sharp deleveraging cycle, and Ethena’s TVL chart shows it like a cliff face.

Let’s look at the charts and h/t to Entropy advisors for compiling the data on Dune:

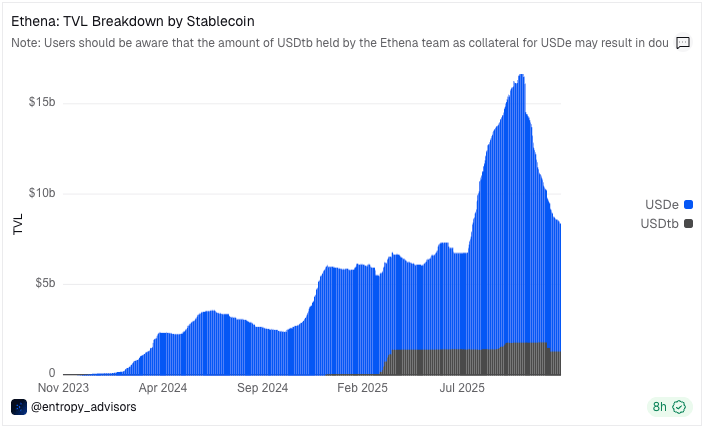

Start with TVL. At its peak in mid-2025, Ethena was sitting on nearly $15B of liquidity — an astonishing rise for a synthetic dollar that didn’t exist 18 months earlier. But the charts show the comedown just as clearly: TVL has slipped by billions as leveraged traders closed positions in the aftermath of funding-rate compression.

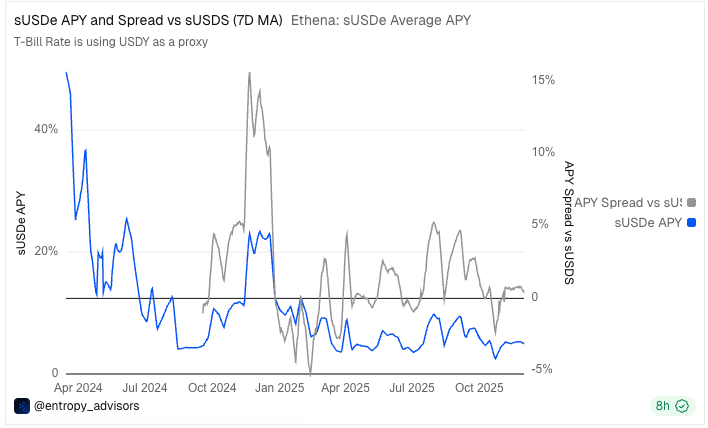

And the yield is gone.

The sUSDe APY, which once spiked into the 20–40% range during crypto’s risk-on periods, has flatlined to ~5% in recent weeks. The spread between sUSDe yields and treasury-backed stablecoins like USDY, once Ethena’s strongest selling point, has almost evaporated.

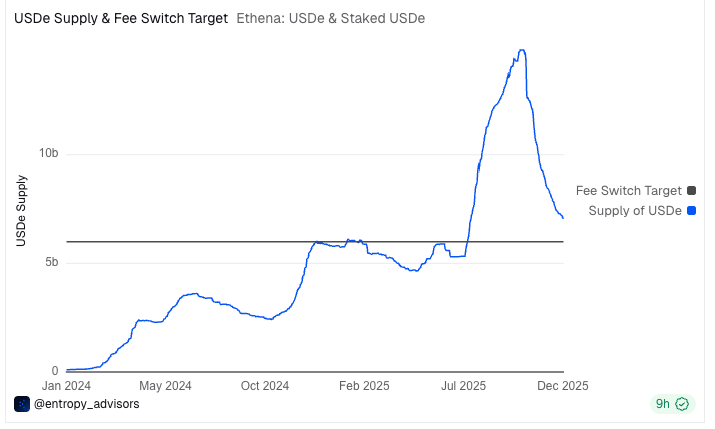

When yields disappear, stakers follow. Staked USDe is also falling sharply, now at under 4B from 6B at the 2025 peak, in September. Unstaking is a lagging indicator of confidence, and traders are voting with their feet.

The network effects unwind from there. USDe supply, which had marched relentlessly upward to a high of 14.8B, dropped by 3B after 10/10.

Meanwhile, the reserve fund, meant to buffer volatility, has held steady around $40–60M, but that stability masks a deeper issue: the fund is tiny relative to a multi-billion-dollar synthetic dollar system. With less funding coming in, Ethena has fewer tools to rebuild that buffer.

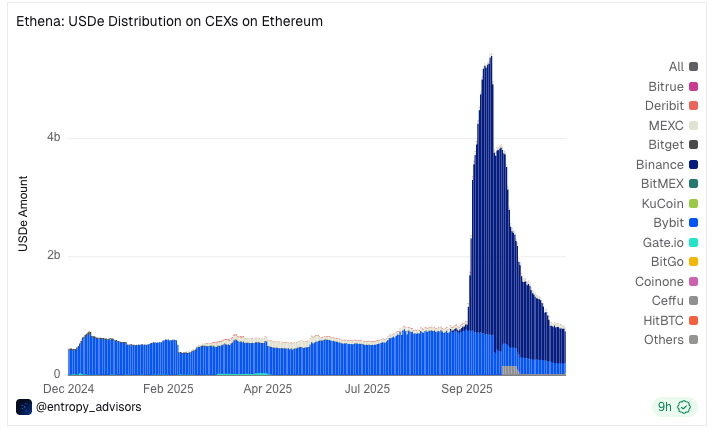

CEX data paints the clearest picture of the unwind. USDe holdings on centralized exchanges, once surging as traders used the synthetic dollar for margin, have crashed back to earth. Ethena’s users were always institutional, directional, and yield-driven. After 10/10, that cohort is deleveraging everywhere.

And it’s not just USDe that’s feeling the pressure. The ENA token has repriced dramatically. Market cap and token price have slid from their summer highs, while ENA staking remains static near 5–6%.

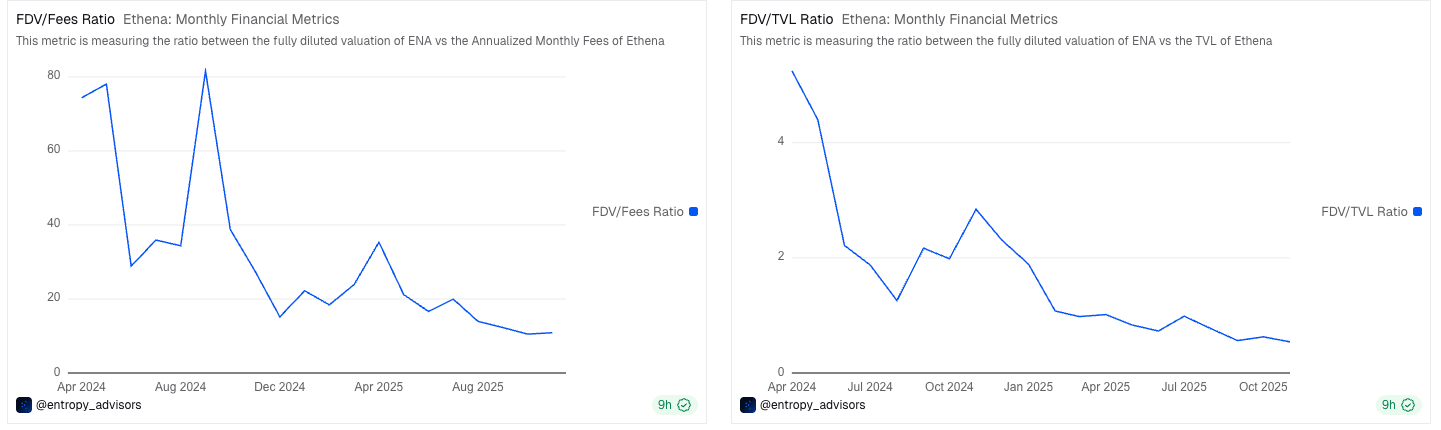

Even more telling: Ethena’s FDV/TVL ratio has collapsed from above 4x in early 2024 to under 1x today. Its FDV/Fees ratio tells the same story, collapsing from 60–80x at peak hype to the teens now. The market is no longer valuing Ethena as a hyper-growth protocol. It’s valuing it like a mature, low-yield business tied to a single macro input: funding rates.

As if the macro headwinds weren’t enough, Ethena is now facing operational fallout. As mentioned, the blockchain Ethena co-announced with Securitize, Converge, pitched as a high-speed RWA L1, has been delayed. The failure to launch the chain on schedule forced at least one project, Terminal Finance, to shut down entirely.

Ethena isn’t collapsing — its core delta-neutral engine still works — but the charts are unmistakable. The era of easy funding is over. The post-10/10 hangover is real. And the synthetic dollar that took over DeFi may now need a new growth model to survive its first real cycle.

With love,

Cami, founder of The Defiant

Forwarded this newsletter? Subscribe for daily insights and curated news from The Defiant team, Monday-Saturday. It’s free.

🎬WATCH

More than wrappers | RWAs on Avalanche | Ecosystems, Ep.3

In our third episode of the Avalanche Ecosystems mini-series, we dive into one of the most important trends in crypto: tokenization of real-world assets (RWAs). From land records to treasuries, private credit, and publicly traded equities, Avalanche is enabling institutions to not just issue onchain wrappers, but to create the real thing. It's tokenization the right way.

With interviews from Luigi D’Onorio DeMeo and Morgan Krupetsky (Ava Labs), Dan Silverman (Balcony), Kevin Chan (Grove) and Gabriel Otte (Dinari), we explore how Avalanche’s architecture is powering a new wave of RWAs across finance, government infrastructure, and consumer applications.

Watch the mini doc here:

This content is part of a media partnership between The Defiant and Ava Labs

Top News in the Past 24 Hours

- Yearn Finance Suffers $9 Million Exploit Yearn Finance, the veteran yield-aggregation protocol, has suffered another attack that drained millions from yETH, a Yearn token that bundles several types of staked Ethereum into a single asset. Why it matters: The team said the hack was similar in complexity to the Balancer exploit last month.

- SushiSwap’s Jared Grey Steps Down as Head Chef SushiSwap’s longtime leader, Jared Grey, is stepping down after more than three years as Head Chef and Managing Director of the DEX. Why it matters: SushiSwap was one of the top DEXs during DeFi’s 2020-2021 peak; Its TVL is currently just over $100 million, down significantly from its ATH of over $9 billion in November 2021.

- Strategy Sets Up $1.44 Billion Dividend Reserve The largest publicly traded Bitcoin treasury company announced plans for a $1.44 billion U.S. dollar reserve.Why it matters: The move quickly sparked backlash on social media, with some calling the decision “hypocritical,” given Michael Saylor’s longstanding critique of fiat currencies.

Trending on The Defiant

- Tokenized Gold Gains Ground as Crypto Markets Wobble

- SushiSwap’s Jared Grey Steps Down as Head Chef

- Bitcoin Craters to $84,000 as Asia Signals Risk-Off Sentiment

- Yearn Finance Suffers $9 Million Exploit

- Bitcoin Consolidates at $91,000 as Stocks and Gold Rally

- Optimism CEO Teases New Enterprise Strategy

That’s it for today — if you enjoyed this newsletter, tell your friends! https://thedefiant.io/subscribe