Elastic Finance: Definition, Use Cases and Framework by AmpleSense DAO

Rebase Tokens and Elastic Finance: They’re Not What You Think

Elastic finance (EeFi) offers an exciting monetary and technological innovation, the likes of which has not been seen in the cryptocurrency market in many years. The emerging elastic finance sub-sector – led by Ampleforth – features tokens that experience dynamic supply adjustments called rebases. The rebase allows crypto assets to absorb demand (as measured by price) in order to produce significant reductions in volatility. In theory the rebase should help elastic finance assets be relatively price stable — as compared to Bitcoin and Ethereum.

However, as is common with any new and disruptive innovation, the rise of elastic finance has led to controversy, confusion and debate among developers, investors and others. In fact, the current sentiment around elastic finance is negative, primarily due to four factors:

- Lack of understanding about the rebase: The rebase is the automatic expansion (positive rebase) or reduction (negative rebase) of token supply in response to demand, as measured by price. The first area of confusion has to do with how or why token balances rebase. The second is how the rebase can reduce price volatility without requiring collateralization. Unfortunately, many investors have purchased elastic assets without understanding them, which has resulted in some losing significant capital.

- Price volatility: Many have criticized elastic assets for not achieving guaranteed stability compared to centralized and semi-decentralized stablecoins

- Concerns about utility: Elastic assets are highly experimental and use cases for these tokens have not been clearly communicated. This has led many observers to dismiss elastic finance as ponzi-nomics or suggest rebasing tokens offer no significant benefits over conventional cryptocurrencies.

- Limited Adoption: To date, elastic assets have mainly been used for speculation and have not been integrated into many popular DeFi projects. This is because, in most instances, elastic tokens are not composable with DeFi protocols. Also, developers and their communities believe (or have come to believe) these assets do not bring additional or desirable utility.

It’s time to take a second look at elastic finance and move past the conventional (negative) wisdom.

Our goal is to address common points of confusion and critiques of elastic finance by:

- Providing a clear explanation about what the rebase is designed to achieve and why it is important to the broader crypto economy

- Helping users, investors, developers and others objectively evaluate elastic assets to determine which ones deserve attention and may have the greatest odds of success

- Demonstrating that elastic assets have utility beyond trading and speculation

- Introducing resources that can be used to improve and expand understanding, execution and development in elastic finance

What is the Rebase Good For?

Let’s start out by revisiting the rebase. Many tend to focus on the mechanics of the rebase – specifically what triggers (from a mathematical and smart contract perspective) token supply expansions and contractions (positive and negative rebases). While the mechanics of the rebase are interesting, we think it is much more important to focus on the why rather than how.

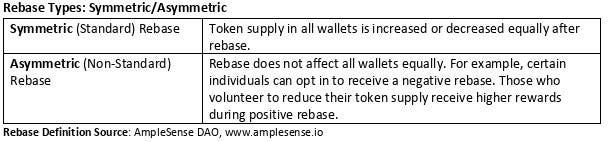

Why does the rebase exist? The sole purpose of the rebase is to incentivize individuals to engage in buying and selling activity that helps a token achieve stability around a specific price zone or target. There are two types of rebases: symmetric and asymmetric, as defined in the table below.

Ampleforth, the original elastic asset, has a symmetric rebase. Since Ampleforth was launched, a number of teams have introduced elastic tokens featuring asymmetric rebases, mainly in an effort to reduce the impact of negative rebases (supply contraction) on all token holders.

Whether the rebase is symmetric or asymmetric, elastic assets should be judged on their ability to maintain relative stability around their target price zone (or price peg) over extended periods of time. If an elastic asset has not achieved price stability over time, it has failed in its primary function.

For example, over a 12 month period (December 2019 to December 2020), Ampleforth’s price largely hovered around $1.00, as shown in the image below. (Ampleforth’s price target is plus or minus 5% the price of the 2019 US dollar.) During the same period, Ampleforth’s market capitalization grew roughly by 27,000% ($ 1.35 M to $ 367.11 M).

Ampleforth Price Target Performance, December 2019 – December 2020Data Source: AmpleSense DAO, DataMetrics Hub, forum.amplesense.io

From a utility perspective, users and development teams can develop products, services and applications that leverage:

- Certain elastic assets’ stability – i.e., their proven ability to eventually return to their target price zone (if they have achieved this difficult feat)

- The positive rebase’s ability to provide an organic source of liquidity that does not require the injection of additional capital (assuming demand for the asset is growing) or collateral

Navigating the Flood of Elastic Assets

Since Ampleforth exploded in popularity in July 2020, dozens of teams have introduced elastic assets featuring symmetric and asymmetric rebase mechanics. This flood of elastic assets has left many people asking how they can determine which protocols are worth their time and attention. Here we introduce a new resource: The AmpleSense DAO Elastic Asset Assessment Framework. The Framework features five criteria that can be used to analyze the short-, medium- and long-term viability of elastic assets. We are sharing this Framework with the crypto community in the hopes that it will encourage informed, objective discussion and decision-making about the relevance and viability of various elastic assets.

Evaluating Elastic Finance Assets: The AmpleSense DAO Elastic Asset Assessment Framework

1. Evaluation Metric: Value Proposition Credibility

Many elastic finance assets are being launched where the primary focus is on the rebase. Credible elastic assets will be designed to meet specific objectives (e.g., achieve price stability without collateralization), rather than simply positioning the rebase as a potential profit-generating mechanism.

Rating Criteria

- Low Value Proposition Credibility: Asset’s primary goal is to deliver potential profits to early investors via the rebase mechanic; other use cases are unclear or better served using standard cryptos.

- Moderate Value Proposition Credibility: There are other ways to achieve the asset’s goals with standard cryptos, but the rebase may help satisfy critical unmet needs in centralized or decentralized finance.

- High Value Proposition Credibility: The rebase mechanic is well-aligned with the intended purpose of the asset; alternative approaches are undesirable for key reasons (e.g., they raise regulatory concerns, increase systemic risk, etc.).

2. Evaluation Metric: Technical Robustness and Security

To be successful, elastic finance assets must be secure, operated via non-opaque smart contracts, and require the presence of a robust technical infrastructure, such as oracles.

Rating Criteria:

- Low Technical Robustness and Security: No security audits and fragile technical infrastructure (i.e., risk of oracle attack is high, or rebase is triggered manually)

- Moderate Technical Robustness and Security: Security audits, and oracles are present, but smart contracts are not open source, verified or feature hidden functions (e.g., a non-publicly auditable proxy contract drives the protocol).

- High Technical Robustness and Security: Contracts are well-audited, code is open source, there no hidden functions and robust oracles are present.

3. Evaluation Metric Decentralization

Successful elastic assets must be highly decentralized, non-censorable and widely adopted.

Rating Criteria:

- Low Decentralization: Asset ownership is highly centralized, transactions are censorable and adoption is limited beyond initial speculators.

- Moderate Decentralization: Asset ownership is moderately centralized, transaction censorship is present, but will be phased out over time, adoption is growing beyond speculation.

- High Decentralization: Asset ownership is widely distributed, robust use cases for protocol exist, transactions are non-censorable.

4. Evaluation Metric: Regulatory Exposure

Investors, users and developers should consider the emerging regulatory landscape surrounding cryptocurrencies, especially as they relate to issues such as stablecoin issuance and securities regulations, when considering the long-term viability of different elastic assets.

Rating Criteria:

- High regulatory Exposure: Elastic asset falls into an area of significant regulatory scrutiny, such as algorithmic stablecoins, or was sold via a non-compliant ICO.

- Moderate Regulatory Exposure: Asset is not a stablecoin, but it was sold via a non-compliant ICO, or asset could potentially qualify as a security.

- Low Regulatory Exposure: Asset is not a stablecoin, team held a compliant ICO (or no ICO conducted), token does not meet the criteria for a security.

5. Evaluation Metric: Temporal Price Stability

The primary objective of the rebase mechanic is to achieve price stability over time. Temporal Price Stability is a metric that measures the amount of time the asset spends within its target range. If an asset is outside its target, the contraction phase (negative rebase) is more impactful on investors, developers and users than expansion (positive rebase).

Note: It may be more difficult for elastic assets pegged to an individual cryptocurrency’s price, index (e.g., basket of currencies) or total crypto market capitalization to achieve high temporal price stability.

Rating Criteria:

- Low Temporal Price Stability: Asset has spent most of its life outside the target range – especially in negative rebase, which suggests insufficient demand for the asset; the market is not able to manage an elastic asset with a shifting rather than stable price target (e.g., if it is pegged to a specific cryptocurrency’s price).

- Moderate Temporal Price Stability: Asset spends significant time within target range, but also can experience long periods of expansion, as demand increases.

- High Temporal Price Stability: Asset spends most of its time within target range with modest and limited expansion and contraction phases (negative and positive rebases).

Are Elastic Assets Useful – or Useless?

A common critique of elastic assets is that they serve no other purpose than speculation, or offer a solution in search of a problem. This is not the case.

From a macro crypto perspective, elastic assets – specifically those with proven ability to serve as generally stable stores of value and mediums of exchange — could lead to a more robust DeFi ecosystem, and even used as currencies, an achievement that no crypto has achieved.

Many observers and analysts have noted that DeFi is increasingly vulnerable due to its over-reliance on collateralized and centralized stablecoins. Currently, policymakers and regulators are taking aim at stablecoins, with an eye toward reducing their impact and controlling their growth. One of the most recent developments was the publication of the STABLE Act in late 2020, which would prohibit centralized and decentralized stablecoin issuers from operating without securing a banking charter.

If adopted widely, elastic finance assets could greatly reduce the crypto ecosystem’s reliance on centralized stablecoins, and provide multiple ways to develop innovative, stable stores of value and financial instruments that have limited exposure to governments and regulators — and go beyond what stablecoins can offer.

Admittedly, utilizing elastic assets to help DeFi reduce its regulatory vulnerabilities is a long-term project. Are they any ways elastic assets are being utilized right now? Yes.

Are All Elastic Assets Stablecoins? No.

It is important to note that not all rebasing assets function as stablecoins. Many observers group all rebasing assets into the stablecoin category, which is inaccurate and incorrect. Different elastic tokens seek to achieve stability over varying time periods. Algorithmic stablecoins (that use the rebase mechanic to achieve a tight peg around $1 USD or another fiat currency) are only one type of elastic asset. There are others, as the table below illustrates.

Elastic Assets: Current Functions

1. Stable Store of Value and Medium of Exchange

(Over Longer Time Periods)

Rebase is designed to enable the token to function as a reasonably stable store of value (e.g., price generally returns to a target range over time), and uncorrelated asset.

Example: Ample

2. Algorithmic Stablecoin

(E.g., Token Value Pegged to $1 Majority of the Time)

Rebase is combined with other techniques that encourage token supply reductions, to help the token maintain a peg as close to $1 as possible.

Example: Empty Set Dollar

3. Rebasing Index/ Crypto Pegged Token

(E.g., Track Total Crypto Market Capitalization, etc.)

Rebase is tied to a moving target such as the total crypto market cap, or price of a specific cryptocurrency to provide investors with exposure to a large market or growing protocol/token via a single asset.

Example: Base Protocol, Digg

—

We are reserving judgment on which of these use cases will be most impactful. Over time the market will determine which ones are most successful and valuable to the cryptocurrency ecosystem.

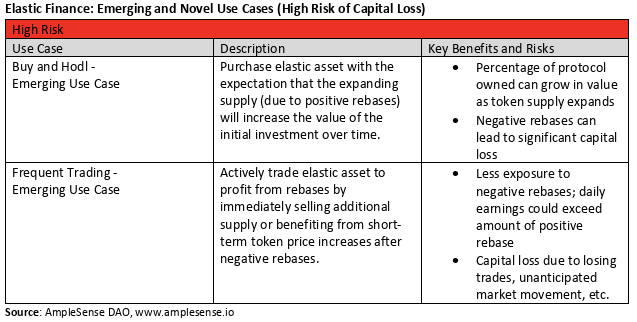

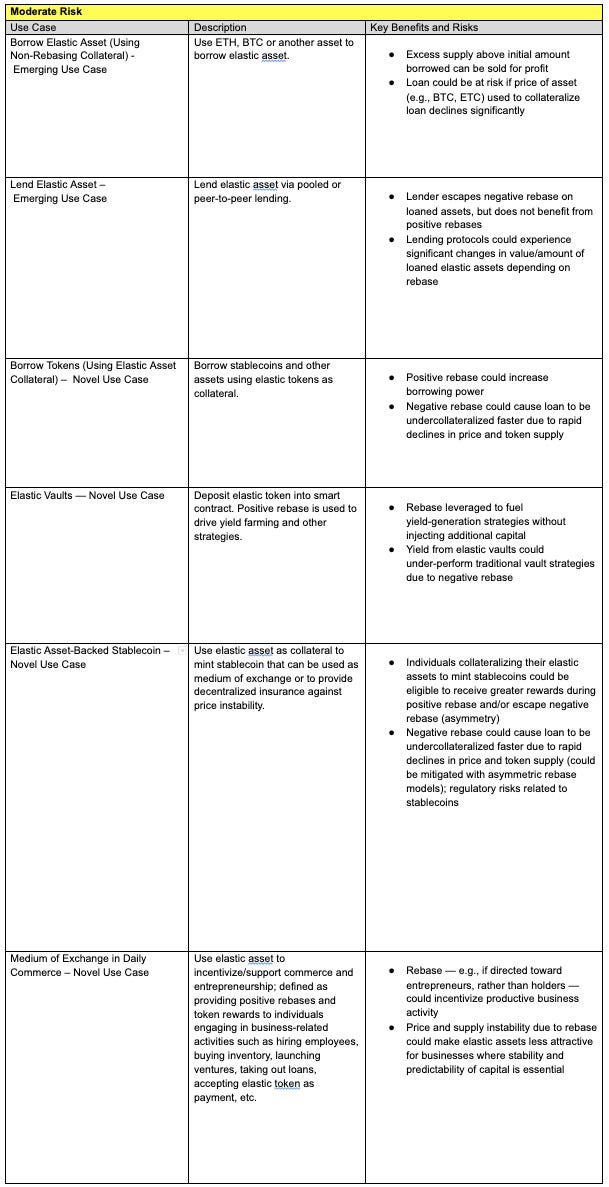

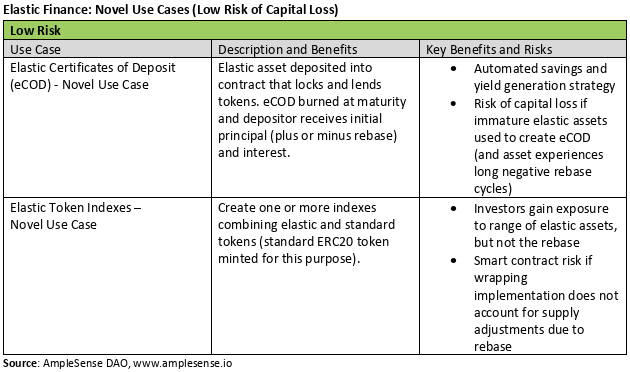

The objective of our independent, community-powered organization (the AmpleSense DAO) is to foster the development of a broad and robust elastic finance ecosystem. Given this, we have put a lot of thought into the various ways rebasing tokens can be utilized – along with the risk of these activities. Risk is defined as the potential for capital loss related to buying, trading holding or using these assets.

The three tables below describe emerging and novel (un-launched) use cases for elastic finance assets. Our DAO is working on developing a few of these implementations currently.

There is potential for numerous other use cases to be introduced over the coming months and years, including using elastic assets as a unit of account in financial contracts.

The Road Ahead: A Multi-Year Journey

Elastic finance represents a profoundly important innovation in crypto, on par with the introduction of Bitcoin and Ethereum. Similar to Bitcoin and Ethereum, the first rebasing asset (Ampleforth), helped to launch an expanding crop of elastic finance innovations.

Over time the rebase will shift from a source of negativity and misunderstanding to an integral and accepted part of DeFi. It took more than 10 years for people to understand and begin to more broadly accept Bitcoin. Likewise, it may take many years for elastic assets to reach their fullest potential and adoption.

But we do not have to wait for the far future to benefit from elastic finance today. As we have shown, elastic assets can be objectively evaluated, have a clear and vital purpose, and possess use cases that go far beyond speculation and trading.

We look forward to helping to innovate, explain, track and grow the elastic finance ecosystem as this sub-sector matures. We’ll be back with new insights about how elastic finance is evolving and influencing DeFi and the broader crypto market in the future.

The AmpleSense DAO leadership team developed this essay. The DAO is an independent, community-powered organization focused on improving understanding and adoption of Ample and other high-quality elastic finance assets. The DAO’s governance token is kMPL. Learn about and join the DAO’s mission at www.amplesense.io.

Advertisement

Get an edge in Crypto with our free daily newsletter

Know what matters in Crypto and Web3 with The Defiant Daily newsletter, Mon to Fri

90k+ Defiers informed every day. Unsubscribe anytime.