DeFi Projects Clash After MakerDAO Adds Ethena’s USDe As Collateral

DeFi projects are up in arms with MakerDAO after the veteran DeFi lending protocol added Ethena’s USDe ‘synthetic dollar’ to its collateral basket as part of its Endgame overhaul.

On March 29, MakerDAO approved an executive proposal setting a debt ceiling of $100 million DAI for the Spark DAI Morpho Vault, which lets investors borrow DAI against USDe and sUSDe (staked USDe).

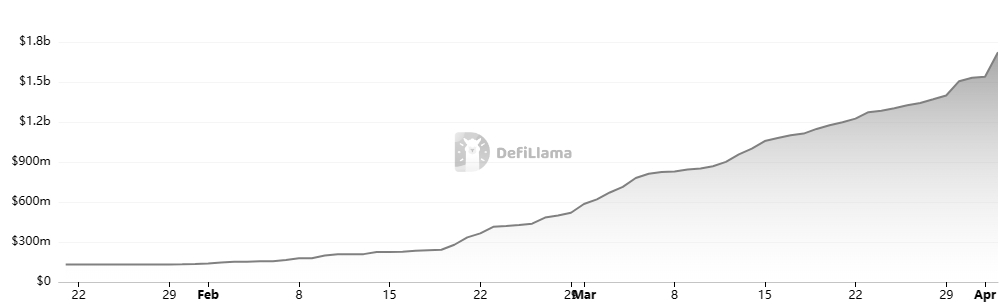

Adding both assets, the first of which currently holds fifth place for stablecoins by market cap – sitting firmly above $1.6 billion – has caused a stir in the DeFi lending sector.

“MakerDAO has become unpredictable in terms of risk management,” said Marc Zeller, founder of the Aave Chan Initiative. Zeller has authored a proposal in Aave’s governance forum to revoke the collateral status of DAI on Aave.

“This will mitigate potential contagion risks for the Aave users,” posted Zeller today on X, adding that “DAI remains an onboarded asset that users are free to borrow. "Endgame" it is,” he wrote.

He told The Defiant that de-risking is better because MakerDAO is “simply not the conservative protocol we used to love.”

His remarks echoed those of David Garai, founder of Nostra Finance, a permissionless, non-custodial lending and borrowing protocol on Starknet.

“We are basically disabling DAI as a collateral asset,” Garai told The Defiant. He explained that his team has observed that the collateral backing USDe and now DAI is being held at custodians, who deposit those assets to centralized exchanges.

“We aren't confident that in a bear market, these centralized exchanges will remain solvent, and in case of insolvency, the custodians will make up for any shortfall,” he concluded, pointing out that existing lenders and borrowers will not be affected by the change.

Controversial Architecture

Ethena Labs, the startup behind USDe and sUSDe, has drawn comparisons to Terra and its ill-fated UST stablecoin with its double-digit yield when it launched on Feb. 21.

However, its architecture has been widely celebrated by crypto heavyweights.

The “synthetic dollar” is collateralized with crypto assets – such as staked Ethereum (stETH) – that are hedged with corresponding short futures positions on centralized exchanges. Ethena Labs is able to offer its high yield – currently 35% APY on sUSDe – thanks to a blend of native staking returns and average funding fees paid to shorts.

Funding fees are the mechanism through which exchanges get perpetual futures to trade in line with spot prices. Positive funding means that traders holding long positions pay a fee to those holding short positions, like Ethena.

Pushing back against today’s outcry is MonetSupply, the pseudonymous co-founder of Block Analitica, a risk intelligence platform for DeFi.

“Is it too much to ask that people read (or even just skim) risk analysis post[s] on the dai vault before posting wild hot takes?” he wrote on X before explaining his thesis.

According to him, DAI borrowers bear the majority of the risk exposure via overcollateralization, with a surplus buffer that covers the additional $100 million approved last Friday.

MKR acts as the final backstop, MonetSupply wrote, explaining that the token is “very liquid” thanks to roughly $145 million of liquidity on decentralized exchanges. Since this makes up only a small part of overall DAI collateral, it allows MakerDAO to quickly and easily grow the surplus before, “making DAI more resilient,” he added.

MonetSupply highlighted that multiple backstops protect DAI in case of potential problems: the Ethena insurance fund, Morpho DAI borrowers' excess collateral, the MKR surplus buffer, and finally, MKR holders via minting/selling to recapitalize the protocol.

Advertisement

Get an edge in Crypto with our free daily newsletter

Know what matters in Crypto and Web3 with The Defiant Daily newsletter, Mon to Fri

90k+ Defiers informed every day. Unsubscribe anytime.