Crypto Lender BlockFi Suspends Withdrawals

BlockFi, a centralized crypto lender which pays users a return on deposits of digital assets, has paused withdrawals on its platform.

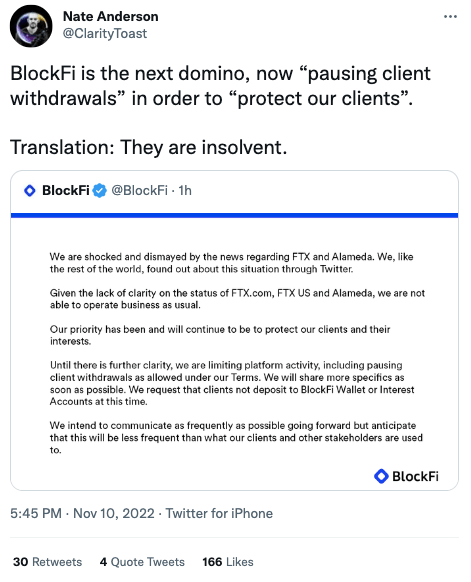

“Given the lack of clarity on the status of FTX.com, FTX US, and Alameda, we are not able to operate business as usual,” the company said on Twitter, before saying that pausing withdrawals was part of a move to “limit platform activity.”

While not explicitly stated, the simplest explanation for the move is that BlockFi doesn’t have enough assets on hand to cover clients’ withdrawal requests.

Nate Anderson, the founder of Hindenburg Research, a firm which specializes in short selling, tweeted that BlockFi was insolvent.

As with FTX and Alameda’s potential insolvency, a key issue is that BlockFi is not actually an on-chain crypto protocol, and as such, what the company does with customer deposits isn’t transparent.

Over the summer, we saw similar situations unfold at Celsius and Voyager in the wake of Terra’s implosion and the collapse of another high-flying crypto hedge fund, Three Arrows Capital.

FTX Acquisition

FTX’s U.S. arm signed an option to purchase the lender in July. The acquisition is yet to be completed, according to BlockFi’s co-founder and COO, Flori Marquez, who tweeted that the company was still an independent business entity.

The beleaguered Sam Bankman-Fried, who founded both FTX and Alameda, tweeted about BlockFi’s finances in July. “BlockFi is financially strong,” he wrote. “All operations are normal, as they always have been, and assets are safe.”

BlockFi raised a Series D round that valued the company above $3B in February 2021, according to Crunchbase.

With another major entity showing signs of insolvency, the worry for many crypto participants is that the contagion will spread throughout the industry, as it did over the summer.

Advertisement

Get an edge in Crypto with our free daily newsletter

Know what matters in Crypto and Web3 with The Defiant Daily newsletter, Mon to Fri

90k+ Defiers informed every day. Unsubscribe anytime.