Concentrated Liquidity Increases Risk of Impermanent Loss, Bancor and IntoTheBlock Found

On-Chain Markets Update by IntoTheBlock Uniswap v3’s concentrated liquidity improved capital efficiency, but also amplified the risks of impermanent loss. Here is the breakdown of the profitability of liquidity providers and how it could potentially be improved. Recently an interesting paper was published by the Bancor team related to impermanent loss when providing liquidity on…

By: Juan Pellicer • Loading...

Research & Opinion

On-Chain Markets Update by IntoTheBlock

Uniswap v3’s concentrated liquidity improved capital efficiency, but also amplified the risks of impermanent loss.

Here is the breakdown of the profitability of liquidity providers and how it could potentially be improved.

Recently an interesting paper was published by the Bancor team related to impermanent loss when providing liquidity on the protocol. The study gathered data from the launch of Uniswap v3 in May until the end of September. It concluded that the impermanent losses (-$260.1M) out shadow the returns earned from trading fees ($199.3M). Also, it found no evidence that certain highly active management strategies would be outperforming those more passive strategies when readjusting liquidity.

The methodology used for the study took into account a total of 17 liquidity pools accounting for 47% of the TVL of the platform at that time. The rest of the TVL was not analyzed due to being in liquidity pools with stablecoins or coins pegged in price between each other, or in pools with not enough liquidity (less than $10M). The data is segregated into three main categories: positions, wallets and pools. This is useful since many wallets tend to deploy several different liquidity positions, on average from 1.25 to 4 positions, depending on the pool. So the performance can be measured either by wallet or by position.

Also, it allows to measure which kind of pools incurred more impermanent losses or accrued more fees, something that can help learn how to mitigate impermanent losses and provide liquidity minimizing risk. Although the gas fees are measured in the study, these conclusions were taken into account without accounting for them, so it is expected that they would exacerbate the losses if they would be considered.

Positions, Wallets and Pools

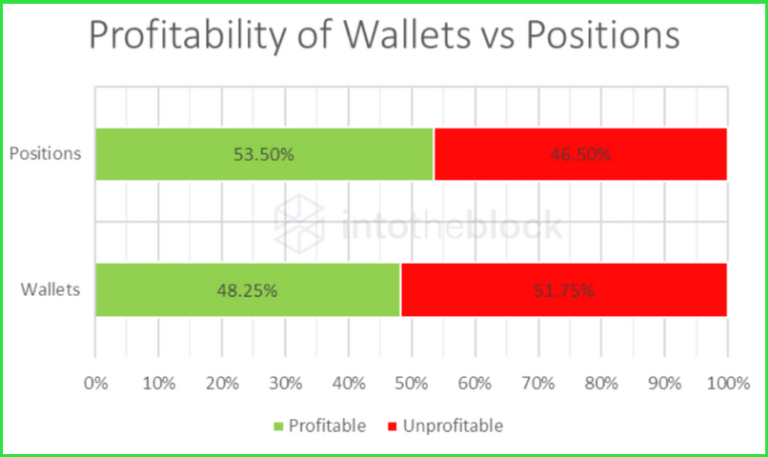

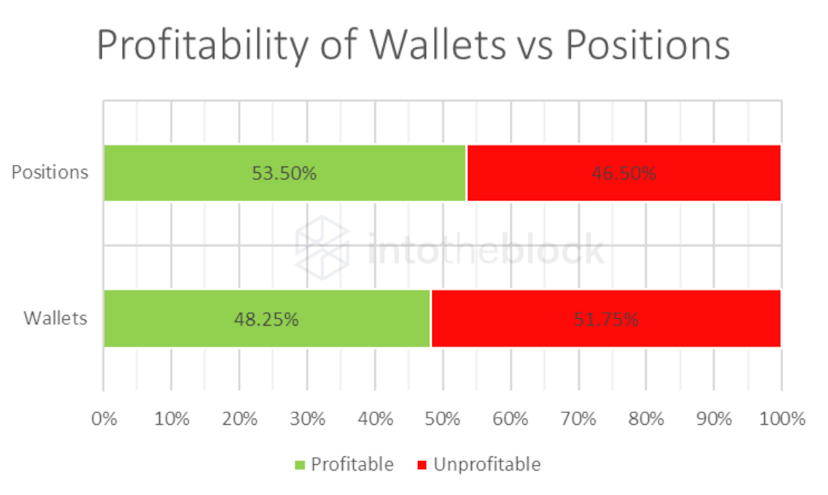

At IntoTheBlock we had access to the raw data of the study and were able to replicate the results. We were particularly interested in how the performance was per wallet and per position and to compare each of them. Summing up, 53.50% of the positions were profitable versus 46.50% that were not. When looking at wallets those that were in profit were a minority with 48.25% over 51.75% that were unprofitable. So up until the date of the study, we can state that the majority of the addresses providing liquidity in Uniswap v3 were not making money.

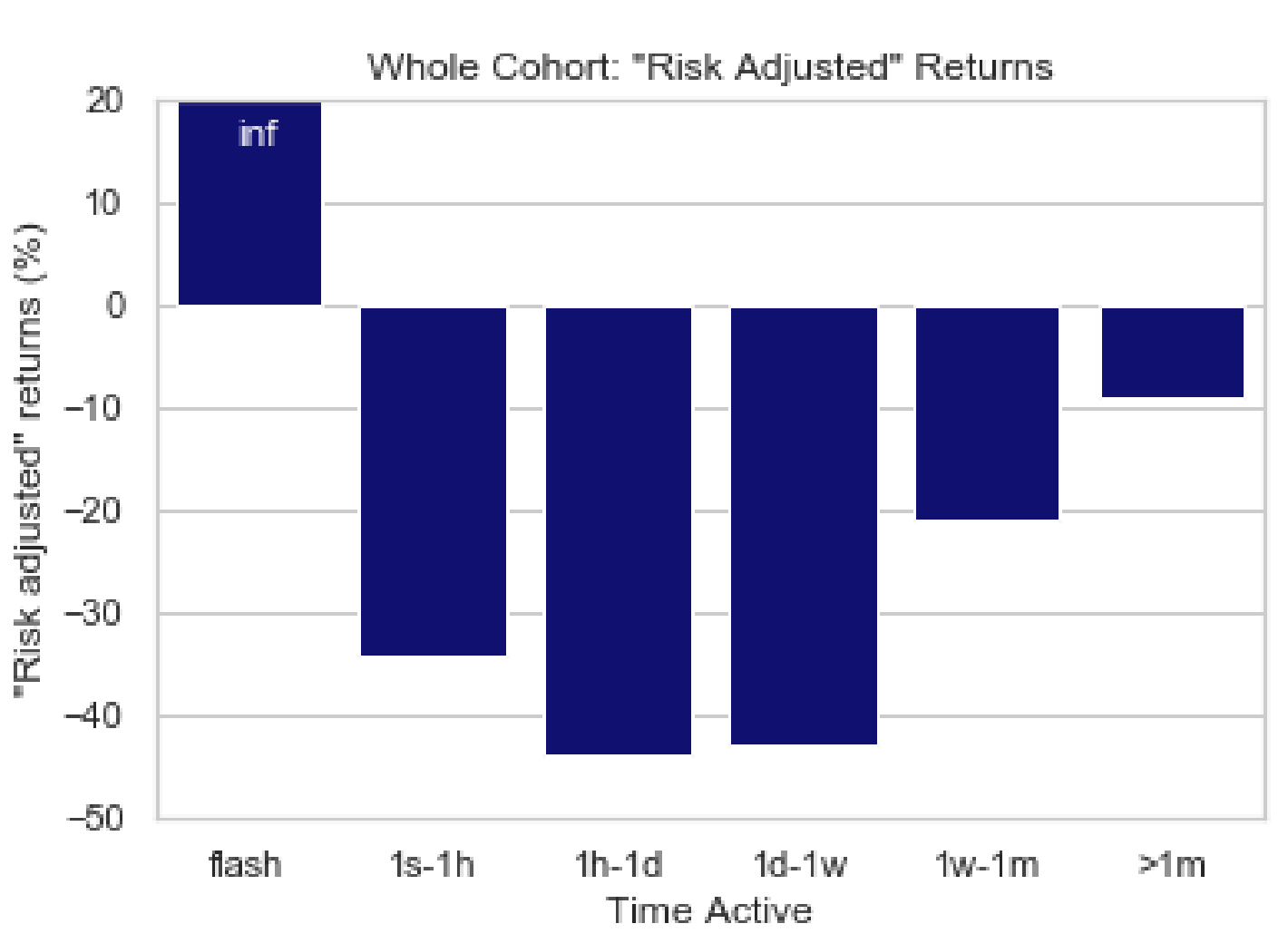

The study goes deeper than that and analyzes the risk-adjusted returns of each position accounting for the time that they were active. After analyzing how active the positions are over different time periods it can be seen that there were no periods where positions earned more fees than impermanent losses, besides flash liquidity providers. This is an advanced and convoluted strategy known as just-in-time liquidity, performed by providing and removing liquidity in the same block as a big trade is seen in the mempool to be about to happen. So managing the liquidity actively does not outperform certain timeframes over others.

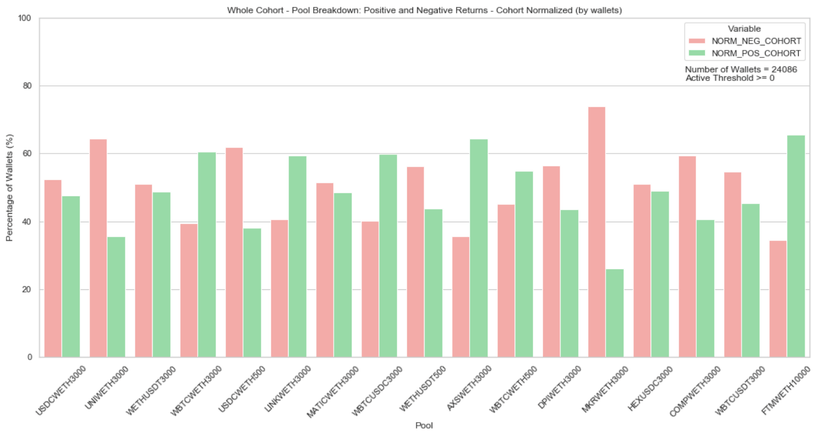

The study also found that it is usual that wallets have several different positions for the same pool, so it studied the performance of wallets by accounting for all of their positions and segregating them by pools. Those pools that have the majority of the addresses providing liquidity profitable are those that have a high correlation (BTC-ETH, LINK-ETH, AXS-ETH, FTM-ETH).

Another one not correlated is curiously BTC-USDC. This is due to the high utilization ratio that it gets (Fees/TVL). This showcases the importance of keeping in mind first the correlations in price between assets which will minimize impermanent loss and then the utilization ratios of each pool, which will maximize returns. So certain pools achieve to accrue more fees than impermanent loss, but they are the minority.

Teachings and Solutions

After analyzing the paper we can conclude that engaging in providing concentrated liquidity is an activity with a higher risk but higher reward profile more suited for professional LPs and experienced DeFi users, similar to how market making is done (liquidity by ranges is an abstraction related with central limit order books). Novel users seeking to provide liquidity might find easier other protocols where the impact of impermanent loss is minimal or even non-existent. Being profitable in Uniswap v3 can be approached by adjusting how the user is providing liquidity profitably or by the protocol mitigating some of these losses through design changes.

A user should always have in mind best practices like for example that those pools with highly correlated assets will suffer considerably. Those deciding to deploy positions in tight ranges can expect higher returns but at the expense of a higher risk of incurring more impermanent losses, and the time that the positions are kept open does not seem to have much effect. Risk can be taken sometimes in certain pools that despite being initially composed of uncorrelated assets, their utilization is high and its trading fees overcome impermanent losses.

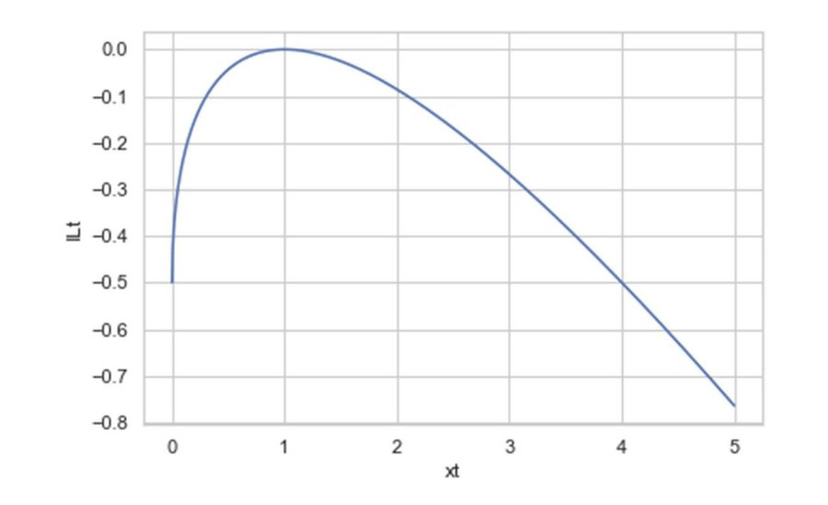

Comparing the incurred impermanent loss relative to the variation in price between two assets

From the side of Uniswap v3, there are certain ideas that would be cool to try out to mitigate impermanent loss on their users, at least partially.

The most direct one would be some sort of liquidity mining program, offering UNI tokens in those popular pools that are expected to have greater impermanent loss due to their low correlation. Covering the losses with governance tokens can be implemented in some sort of impermanent loss coverage or insurance for those positions that really were impacted by it (similar to Bancor). Another more adventurous endeavour would be to try out the popular topic of protocol owned liquidity (Tokemak, Olympus).

Do readers think that this change would be feasible for an already deployed protocol with such a big TVL? Let us know.

Advertisement

Get the best of The Defiant directly in your inbox 💌

Know what matters in Web3 with The Defiant Daily newsletter, every weekday

90k+ investors informed every day. Unsubscribe anytime.