Voyager Rejection of FTX Buyout Leaves Investors Searching for Answers

Thanks but no thanks.

That was the message Voyager Digital, a bankrupt crypto lender and exchange, delivered to FTX and Alameda Ventures on Sunday.

On July 22, Sam Bankman-Fried, the CEO of digital asset exchange FTX, proposed a restructuring deal to Voyager. The stricken platform’s customers would get immediate relief in the form of liquidity and the option to join FTX, one of the top crypto exchanges worldwide.

But two days later, Voyager rejected the proposal out of hand as “a low-ball bid dressed up as a white knight rescue,” according to a court filing. Translation: FTX was attempting a takeover adverse to Voyager’s interests.

Extending Credit

The bankrupt firm also described the proposed deal as “a liquidation of cryptocurrency on a basis that advantages AlamedaFTX.”

Alameda Ventures is an affiliate of Alameda Research, a crypto trading firm founded by billionaire Bankman-Fried. While the crypto mogul has relinquished day-to-day control of the Alameda companies, they and FTX have occasionally acted in concert during this year’s digital asset meltdown, extending credit to or buying distressed companies.

Under Bankman-Fried’s two-part proposal, Alameda would purchase Voyager’s cryptocurrencies and digital assets loans — excluding debt issued to Three Arrows Capital — at market value. Alameda would also write off its own $75M loan claim as part of the proposal.

FTX said that Voyager customers could then receive “immediate liquidity” by opening an account with a cash balance funded by a portion of their bankruptcy claims.

Unsecured Claims

In a news release, FTX said the proposal would allow Voyager customers to “reclaim a portion of their assets without forcing them to speculate on bankruptcy outcomes,” adding that “Voyager’s customers did not choose to be bankruptcy investors holding unsecured claims.”

In a strongly-worded response, Voyager implored interested parties to “really read [the proposal].”

“To anyone who reads the Proposal even in a cursory way,” the company said, “it will be obvious that the stand-alone Plan that Voyager filed is capable of delivering far more value to customers than the AlamedaFTX proposal.”

Voyager Delivers Painful Lesson on Perils of Counterparty Risk in Bankruptcy Drama

Voyager Delivers Painful Lesson on Perils of Counterparty Risk in Bankruptcy Drama

Exposure to Three Arrows Sinks Crypto Exchange as Dominoes Fall

Among other things, Voyager slammed the proposal for “converting customer cryptocurrency claims into U.S. dollars based on prices as of July 5, 2022, and paying cryptocurrency claims in U.S. dollars, with customers bearing the tax consequences associated with dollarizing and liquidating their claims,” its court filing said.

Graeme Fearon, special counsel at Australian law firm Moulis Legal, suggested that FTX’s proposal may be appealing to Voyager’s anxious clients, especially compared to what the company itself was capable of producing as it moves through administration.

FTX’s proposal “needs to be seen against the backdrop of Voyager’s own offer to repay customers in a mixture of cryptos (including Voyager’s own token), stock and any funds recovered from [Three Arrows Capital],” the lawyer told The Defiant.

“Given the current Crypto Winter, there can be no expectation of a better ‘white knight’ riding to the rescue, so FTX’s offer may be as good as it gets.”

Graeme Fearon

“Given the lack of clarity as to how much this offer might actually be worth and when it might be finalized (and the fact that it represents no change in management), customers could be forgiven for preferring FTX’s bird in the hand,” Fearon added. “Given the current Crypto Winter, there can be no expectation of a better ‘white knight’ riding to the rescue, so FTX’s offer may be as good as it gets.”

Ramnik Arora, head of product at FTX, responded to Voyager’s filing on Twitter, asserting the firm would pay the current market value of assets purchased as part of the proposal. “If this transaction was happening today, we’d buy ETH from the ‘estate’ at $1,600 as opposed to $1,150 on Jul 5th,” he said.

Succumb to Insolvency

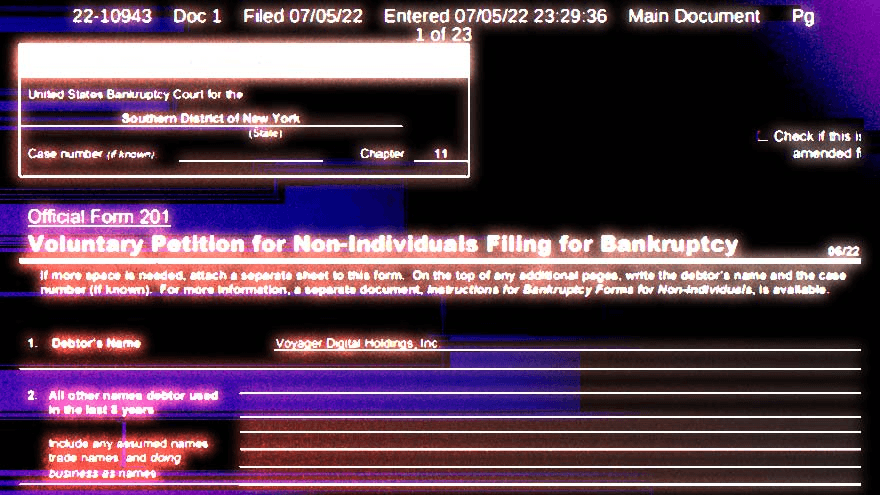

Voyager filed for bankruptcy on July 5, becoming the latest major centralized digital asset lending firm to succumb to insolvency as the systemic risk contagion from the 2022 crypto crash spread.

Voyager generated an impressive $415M in revenue for 2021, and as of late June, boasted 3.5M customers. In its filing for Chapter 11 bankruptcy, Voyager said it still holds $110M in cash, $1.3B worth of crypto assets, and $6B worth of outstanding loans.

Frustration Turned to Anger For Creditor Who Foresaw Three Arrows Collapse

Frustration Turned to Anger For Creditor Who Foresaw Three Arrows Collapse

Dutch Crypto Exchange Deribit Pleaded with 3AC Founders for Information to No Avail

But the firm loaned 15,250 BTC and $350M in USDC to Three Arrows Capital, a multi-billion crypto venture firm famed for its ‘supercycle’ thesis that went bust due to a combination of excessive leverage and overexposure to the now-collapsed Terra Classic.

On June 22, Voyager demanded that Three Arrows — whose founders’ current whereabouts are, to the frustration of the firm’s creditors and liquidators, unknown — repay $658M within five days or face default. Voyager filed for Chapter 11 bankruptcy roughly one week after its demand expired.

Uncharted Territory

Given that this is the first time crypto enterprises at this size have sought bankruptcy protection, the legal system will be treading into uncharted territory. For one thing, it may be unclear who actually owns and has title to the assets held by Voyager, said Timothy Edwards, the head of legal firm HopgoodGanim’s digital assets team.

He said recent rulings by the U.S. Supreme Court and the High Court of England and Wales found that “in some circumstances, exchanges hold digital assets on trust for users or investors.”

“This is extremely significant because, in many jurisdictions, if you hold an asset on trust for another person, title and ownership stays with that person,” Edwards said. “You are then merely the asset’s caretaker, and if you enter bankruptcy, that asset is not usually property which can be divided amongst your creditors (or sold to a ‘white knight’ of any description).”

Fearon added that many of Voyager’s customers may be “treated as unsecured creditors, with no specific consumer or similar protection.”

“In addition, there is uncertainty as to whether their investments will be viewed as currencies or commodities, and this will also affect how much if anything they can recover,” he said.

Submitted an Offer

Bankman-Fried took to social media in response to Voyager’s filing and sought to reassure Voyager’s customers. “We submitted an offer: if accepted, any customer who wanted could come and get back their share of everything that remained, as soon as possible,” he tweeted.

Many customers may be eager to take him up on the offer, even if Voyager’s management team is not.

Advertisement

Get an edge in Crypto with our free daily newsletter

Know what matters in Crypto and Web3 with The Defiant Daily newsletter, Mon to Fri

90k+ Defiers informed every day. Unsubscribe anytime.